Think Big: Should investors fear the inflation spike, or will it be temporary?

Pic: metamorworks / iStock / Getty Images Plus via Getty Images

The US inflation spike on Wednesday night caught markets off guard, but CBA thinks it will prove transitory.

Still, the May inflation print will be of particular interest after April CPI growth came in hot at 0.9pc.

Annual growth leapt by 4.2pc — the highest level since 2008.

Markets were ready for some large annual jumps because of the low base effects from last year.

An important part of CPI interpretations as based around the result, relative to expectations.

On that front, the consensus forecast was for April CPI growth of only 0.2pc, so the 0.9pc jump was a huge beat.

The link between inflation, interest rates and high-growth tech stocks has been well-documented and the US Nasdaq index fell sharply.

But CBA senior currency strategist Elias Haddad reckons investors should “fade the inflation risk”. Here’s why:

Fade the trade

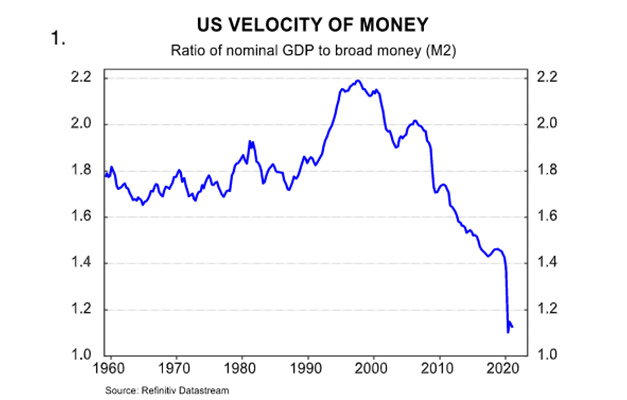

Firstly, Haddad discussed the velocity of money in the US economy.

The term is used to describe the pace at which money is changing hands in the economy. Since the pandemic began, the overall money supply has increased materially.

But as Haddad aptly put it, the speed at which that money is changing hands (velocity) is still “bombed out”:

“This means easy money is not creating a credit boom,” Haddad said.

He also highlighted the U6 unemployment rate, which adds workers who are part-time because business conditions in their sector aren’t operating at full capacity.

Benchmark unemployment (the U3) has fallen from post-pandemic highs of almost 15pc to around 6pc.

But the expanded U6 rate is still “historically elevated” at above 10 per cent, Haddad said.

At those levels, the U6 is an indicator of ongoing labour market slack which in turn is viewed as a negative catalyst for wage growth — a key input to the inflation outlook.

Thirdly, Haddad said core PCE inflation — the preferred measure of the US Fed — is being driven by unusual post-COVID factors rather than cyclical inflation growth.

A good example is the global shortage in semi-conductors, which has hamstrung major global supply chains such as new-car manufacturing.

“This means temporary industry-specific factors are pushing inflation higher,” Haddad said.

But the key thing is they are temporary, and policy makers have made it clear they will “look through” temporary uplifts.

The US Fed wants to get PCE inflation above 2pc, but just as importantly, it wants it to stay there — a situation which hasn’t occurred for more than 25 years.

“As a result, the risk the Fed prematurely reduces policy support is low,” Haddad said.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.