The Ethical Investor: Most ASX companies not doing enough on disclosures – with Perspektiv’s Katie Williams

Ethical Investor: ASX companies not doing enough on disclosures. Picture Getty Image

A move by the ASX to make listed companies more accountable for information they provide to investors has yielded mixed results – with only a minority achieving high levels of compliance with new guidelines.

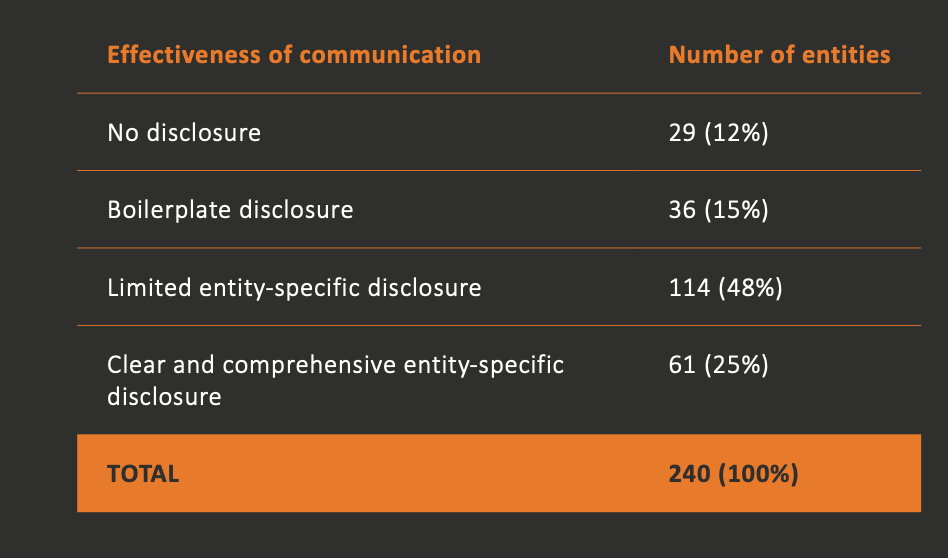

According to a research paper prepared by Deakin University, more than a quarter of a sample group of 240 largest ASX-listed companies made no effective disclosure in relation to the ASX Recommendation 4.3.

And most of them provided only vague or limited details of how they had ensured the integrity of unaudited reports to investors.

Recommendation 4.3 took effect for most ASX listed entities in 2021.

Essentially, the Recommendation states that:

“A listed entity should disclose its process to verify the integrity of any periodic corporate report it releases to the market that is not audited or reviewed by an external auditor.”

Periodic corporate reports are defined by the ASX as:

“An entity’s annual directors’ report, annual and half yearly financial statements, quarterly activity report, quarterly cash flow report, integrated report, sustainability report, or similar periodic report prepared for the benefit of investors”.

Which companies are making efforts?

Deakin’s analysis revealed that the majority of ASX 300 companies have actually made efforts to disclose the processes they use to enhance the integrity of their unaudited periodic corporate reports.

However, the results also revealed significant disparities between companies in terms of the level and quality of their responses to Recommendation 4.3.

For example, 48% of sampled companies made entity-specific disclosures, but with only limited details of how their integrity enhancing processes operated in practice.

15% of companies did not provide entity-specific disclosures, but rather used ‘boilerplate disclosures’, or general statements that could apply to any entity.

Just 61 companies (25%) out of the 240 in the sample were rated as providing clear and comprehensive descriptions of the processes they used to ensure the integrity of their unaudited periodic corporate reports.

A more detailed comparison across the ASX 300 suggests that larger entities (79% of the ASX 100, and 78% of ASX 101-200) were more likely to communicate entity-specific integrity enhancement processes compared to smaller entities (61% of the ASX 201-300).

Deakins has singled out two companies that have done particularly well in their response to Recommendation 4.3.

According to its research, SCA Property Group (ASX:SCA) has a clear and comprehensive integrity enhancing process when it comes to its non-audited periodic corporate reports.

The verification protocols undertaken by SCA’s management include an internal annual review of the disclosures by the relevant internal team – for example finance, legal.

SCA directors are then provided with the opportunity to provide input on the relevant announcement and finally once verified, all announcements are reviewed by the CEO, CFO and General Counsel of the company.

29 Metals (ASX:29M) is also another company that scored highly according to Deakin.

The company follows similar protocols to SCA where it conducts verification by “ticking-and-tying” back to source documentation derived from the company’s information management systems.

Why ‘G’ in ESG shouldn’t be ignored

So how important is the G in ESG?

According to Katie Williams, Principal Sustainability Consultant at Perspektiv, the G is often the least conspicuous when it comes to ESG.

Because Governance – what it does and what it adds – can be hard to define.

Governance seems to capture our attention far less than environmental and social factors, but its role is vital, according to Williams.

Governance is the internal mechanisms and structures that enable the company to formulate and implement its sustainability strategy.

It provides the framework to set the right goals and create the conditions for achieving them.

Williams says that at its core, sustainability governance is a mindset.

It requires everyone in the business – starting with the board – to shift from thinking about short-term financial outcomes, to long-term thinking about multi-generational outcomes.

To accept that risks to the planet and society are risks to the business. To move away from shareholder primacy and towards the interests of all stakeholders.

Interview with Katie Williams of Perspektiv

Perspektiv works with the private sector and government to enable better outcomes for people and planet.

The company uses the UN Sustainable Development Goals as its guiding force and advises clients from a range of different sectors.

Williams’ background is in legal practice, and at Perspektiv, her role is mainly advising clients on the human rights aspects.

She works with companies to help them understand the ways in which their operations can impact on people, which might be their own employees, as well as the communities in which they operate.

How should we investors and companies look at G in ESG?

“Just to take a step back, the concept of sustainability often gets conflated with with ESG, but they’re not really exactly the same, they come from different origins,” Williams told Stockhead.

“ESG comes from financial markets, and sustainability comes from a multi stakeholder, sustainable development context.

“Therefore you can look at Governance from the perspective of how businesses are impacted by social and environmental risks.

“Initially this was the ESG approach and basically the question was, can the investor be satisfied that the governance structures are appropriate to identify risks that could affect the financial condition of the company?

“But there’s also another way of looking at Governance, which goes more to the concept of sustainable development rather than ESG.

“And that’s when you look at it from the perspective of how the world is impacted by the business, or the risk to society and environment that arise from the company’s activities.

“In other words you look at it from the other end of the telescope.

“And there’s a really nice convergence on both of these ways, because if you think about it, the impact on people and planet can also result in impact on the company’s own financial performance.”

But how do you measure Governance?

“There are various ways you can measure it, as there is an alphabet soup of different reporting frameworks, which are mainly voluntary,” Williams said.

“TCFD, or the Task Force on Climate related Financial Disclosures is a big one, and that’s all about the way in which a company reports and discloses its exposure to risks relating to climate change.

“TCFD is absolutely the standard bearer, albeit it relates specifically to the issue of climate change.

“The ASX, ASIC and APRA all have very clearly stated their expectations that listed companies should be adopting the framework of the TCFD.

“ESG ratings are another way governance is being measured, but the problem with ESG rating is there’s absolutely no uniformity in their approach at the moment.”

What are your thoughts on the Deakin’s research?

“That’s a really interesting piece of research, and it’s so relevant to the issues that we have at the moment around greenwashing,” Williams said.

“Good governance means that the company is disclosing and reporting on issues that might materially affect the value of the company, or materially affect the company’s financial position.

“And there’s a regulatory basis for that.

“Corporations are required to provide reports in a way that’s not going to to mislead. Australian Consumer Law is relevant here.”

What ESG reports should be subject to the ASX Recommendation 4.3?

“Listed companies that are fully compliant with the ASX listing rules and the Corporate Governance Principles recommendation should be providing a list of disclosures covered by this recommendation,” Williams explained.

“This should include the Sustainability Report for example, if it hasn’t been subjected to third party verification audit.

“The Modern Slavery Statement is also another clear example.”

What should be the consequences for failing to adhere to the Recommendation?

“The fallout from that is potentially legal action for greenwashing,” said Williams.

“Because if you’re making disclosures about your approach to sustainability, your climate change policy and net zero commitments are the ones that are at the highest risk of greenwashing and litigation.

“So if you’re making these disclosures publicly, then good governance will be requiring you to also make clear the basis in which you’ve put together those statements.

“You might want to have a look at the Santos litigation, which is a real life example of that happening at the moment.”

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.