The Candlestick: There’s absolutely no need to run this week

Via Getty

Carl Capolingua is one of Australia’s leading technical analysts and master prognosticator at ThinkMarkets, where he is admired for his unique style of price action-based trend tracking.

Capo has been honing his art over some 30 years of investing, advising, and managing funds.

Every week in The Candlestick, Carl will be plotting, for your sheer madness, a data-trove of unleavened technical analysis covering markets globally, then drilling fearlessly down into stock-specifics.

Here is his picture. Just in case you needed more, but didn’t know how to ask:

The Candlestick – Fourth iteration – Death by ribbons

In last week’s Candlestick, we discussed each of the key technical analysis-based indicators I use to determine if a rally within a bear market is just that – temporary and doomed to fail – or if it’s the beginning of a shiny new bull market.

To recap, a sustainable rally starts with demand-side candles (the ones with large white bodies and or long lower shadows), preferably corresponding with an influx of volume.

Next, the price action returns to higher peaks and higher troughs, and soon, we should reach the short-term downtrend ribbon. At this crucial zone we should observe a batch of demand-side candles (and not supply-side candles).

As the rally gathers momentum, this ribbon should swing back to up, and finally, the same process of testing and changing the long-term trend ribbon should occur. Once this process is completed, it signals the bear market is over and the new bull market has begun.

This is all great stuff of course, but none of these boxes were checked last week. Instead, the candles point to even more pain ahead for investors.

Poker face emoji.

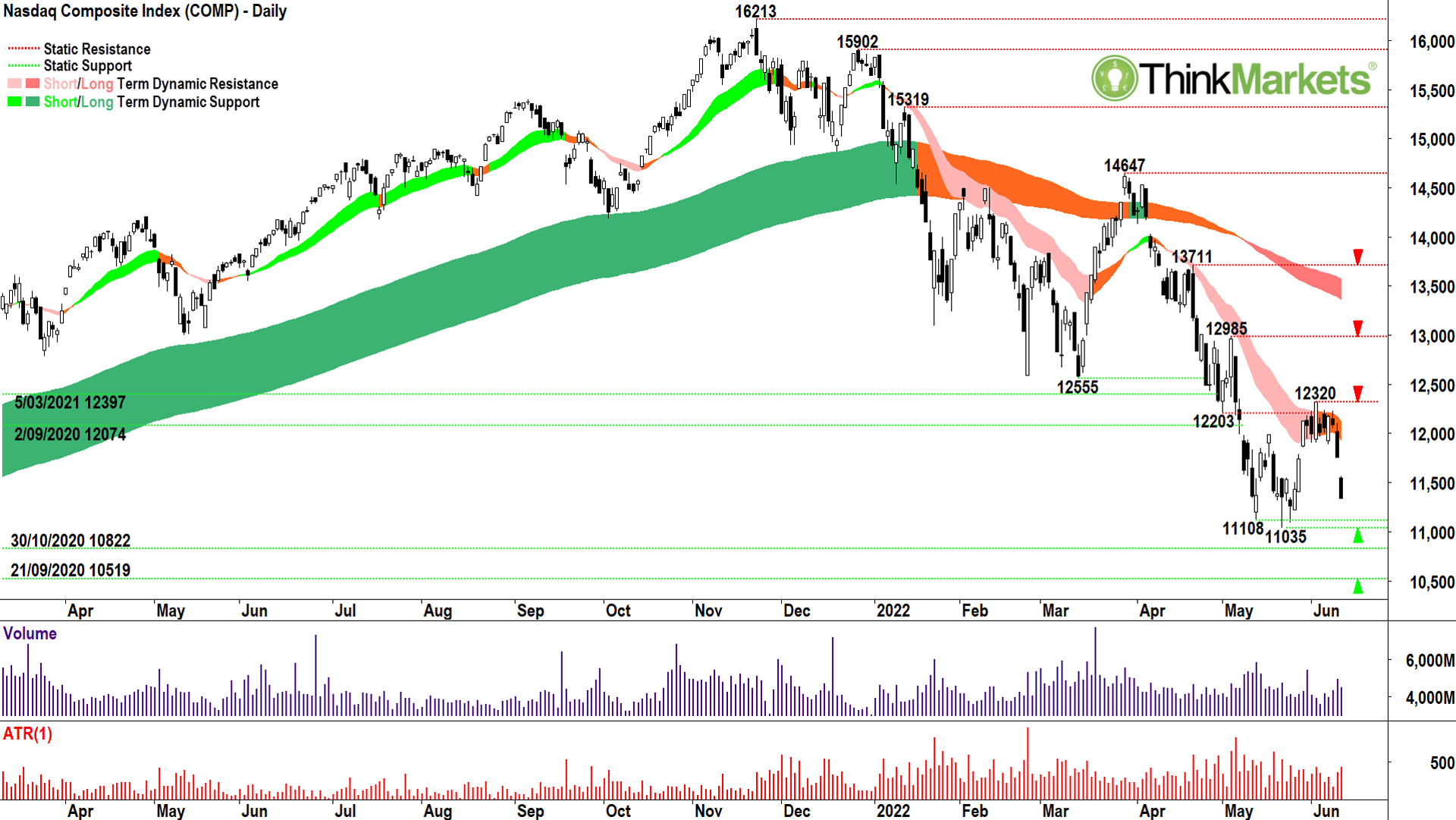

Nasdaq Composite USA (COMP) – Mind the gap, the drop is a doozy…

Let’s kick off with the Nasdaq Composite (COMP) because it is the perfect case study for spotting if the current bear market rally has legs, or if it’s just another false dawn. Remember, bull markets are all about buy the dip (BTD), whereas bear markets are all about sell the rally.

In a bear market, shareholders treat rallies with plenty of hope, but also plenty of scepticism. Any sign of weakness in the rally, or any new disappointment with respect to the news flow, triggers a quick resumption of supply as shareholders scramble to get out before the dreaded next leg down. Similarly, those sitting on cash waiting to buy realise it’s still too early to fish for bargains just yet, and they withhold their demand in anticipation of lower prices ahead. Down we go again.

This is exactly what’s occurred since our last update.

The COMP failed to capitalise on some solid demand-side candles from the 20 May low at 11,035 to the 2 Jun high at 12,320. Unfortunately for investors who were betting on a sustainable rally, it just got stuck in that deadly short-term downtrend ribbon (i.e., the light pink zone). Instead of punching through with a further batch of demand-side candles, and instead of launching back into higher peaks and troughs, by 9 Jun the COMP had resumed lower peaks and troughs and the supply-side candles were back.

It appears my short-term trend ribbon has claimed another victim – see how consistent it has been in acting as an invisible hand pushing the COMP lower since the failure at 15,319.

The 9 Jun candle with its upper shadow and close on the low, and leaking out of the short-term downtrend ribbon, was the death-knell for the fledgling rally. The subsequent 10 Jun wipeout had a sense of inevitability about it. Note also the ‘gap-down’ between the 9 Jun and 10 Jun candles. A ‘gap’ occurs when the price shifts from the close of one candle to the open of the next, and then does not trade back to the prior sessions’ low in the case of gap-down, or back to the prior session’s high in the case of a ‘gap-up’.

Gap-downs demonstrate extreme fear in a market. There has been a dislocation between demand and supply so large that the market is forced to rapidly reassess value.

Looking forward, 11,035 is now crucial.

I see three clear demand pushes from the zone between it at 11,500. Clearly, there’s been some speculative buying down there, and judging by the lack of volume, not a great deal of appetite among the supply side to sell at lower prices. So, it’s possible we see a repeat if we retrace to that zone, i.e., speculative buying and a reluctance to accept lower prices.

This thesis will likely be tested this week.

If the constituents of the COMP can’t find a solid bid in that 11,000-11,500 zone, the supply-side could panic, precipitating another sharp drop through 11,000 and down to the next potential point of demand at 10,519 (a key swing low from Sep 2020).

The final point I’ll make about the COMP is this last failure almost certainly consigns it to one of the ‘longer’ bear markets in history.

Again, just checking back with the data on COMP bear markets, ‘longer’ bear markets are those which lasted greater than six months.

This bear will now likely drag into its seventh month, and worse, it matches the other longer bear markets with its (so far) lack of volume influx occurring at any swing low so far.

View: Bearish, sell rallies until a close above 12,320.

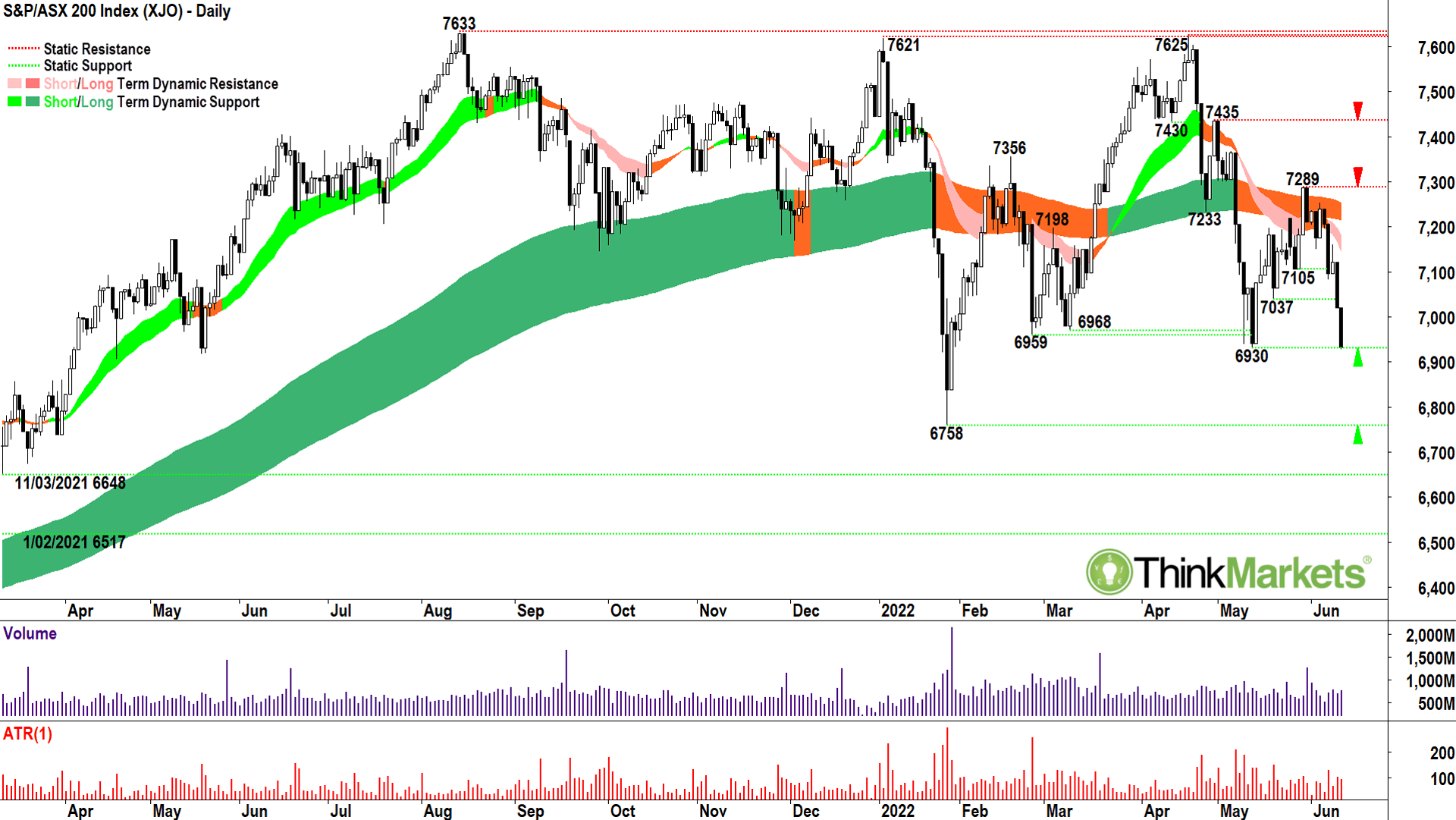

S&P ASX200 XJO about to get Hans Grubered?

Aussie investors got a reprieve on Monday from the selling, but no doubt it’s only a stay of execution.

Still, the local bourse has so far been resilient in the face of the concerted risk-off behaviour which has gripped so many other major stock indices.

My fear, however, is that the charts indicate we’re due for a Nakatomi Plaza-style catch up. Alas, it’s The Hans Gruber chart.

If the ASX had a face, that’s kinda how I feel it would look right now…

Based upon ASX SPI 200 Futures, the local benchmark S&P ASX200 is expected to open around 110 points or 1.6% lower when trading resumes Tuesday.

Asian markets are down between 1-3% as I write this Monday. Plenty hangs on how on US stocks fare in trading tonight. That doesn’t look good either, as Nasdaq futures are pricing in another 1.8% fall.

On the way up, the trend ribbons are light green (short-term) and dark green (long-term). I say they provide ‘dynamic support’; that is, they act like an invisible hand pushing prices back up. This is clearly evident on a number of occasions in the XJO chart between Apr 2021 and Aug 2021 for the short-term ribbon, and until Jan 2022 for the long-term ribbon.

As the long-term trend flattened out, the long-term trend ribbon acted as somewhat of a balance point as we swung either side of it – but inevitably, were drawn back towards it. I fear the most recent failure to decisively reclaim the coalescing short- and long-term trend ribbons at 7,289 is the final straw which breaks the current bull market’s back. A close below 6,930 would confirm the new bear market if I put my pessimist’s hat on, but a bear market is certain should we close below 6,758.

I hope I am wrong and we regain 7,289 quickly, but this increasingly feels like a miracle scenario when considering the gathering momentum to the downside evidenced by the growing number of supply-side candles (the ones with large black bodies and or long upper shadows), and the downward curvature of the trend ribbons.

Downside targets? As in, how bad could it get? Well, we’re down around 9% from our all-time high compared to the S&500’s 19% and the COMP’s 30% declines (shudders).

But I do see some potential demand points at the 2021 low of 6,517 and another well-defined area of support set just after the COVID low around 6,250. View: Bearish, until a close above 7,289.

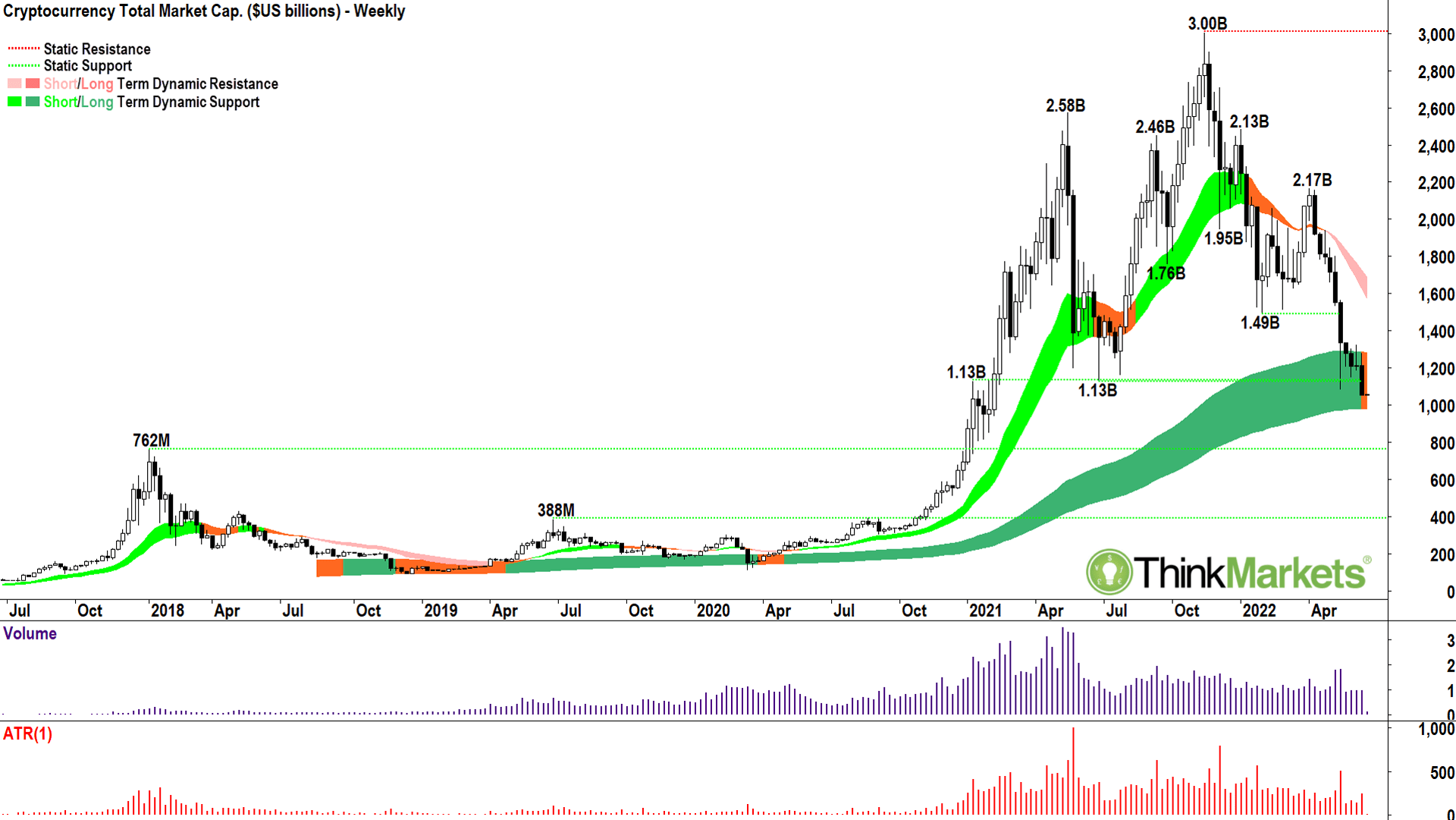

Crypto is losing the confidence game

Crypto investors have reacted poorly to the moves in other financial markets. As liquidity is sucked from the system via higher rates, quantitative tightening, and ultimately for many smaller investors who were dabbling in crypto, lower disposable income, cryptocurrencies are facing a demand vacuum. There’s plenty of selling around as investors cut their losses, or are forced out of leveraged positions, and there are very few buyers with the confidence to step in.

On Monday, Bitcoin touched its lowest level in 18 months – dipping briefly below the psychological $25k support level. It has now wiped out all of its gains since 2021.

The total value of all cryptocurrencies is threating to break below US$1 billion in market capitalisation, down from its peak in November last year of just over $3 billion. That’s when the Fed flipped from dove to hawk and started talking tough on inflation. As the world shifted from ‘inflation is transitory’ to ‘inflation needs to be fought’, risk assets like crypto and non-profit making tech stocks have suffered immensely.

The risk now, is even if the Fed can rein in inflation, there may be too much damage done to asset prices, the wealth effect, and disposable income to avoid a recession. The latter is particularly damaging for crypto. As I have said many times, crypto is a confidence game, not just in terms of what’s happening in the sector, but in terms of how much lazy money is burning a hole in risk-takers’ pockets. There’s at least $2 billion less in those pockets directly due to crypto losses, and likely multiples of this amount due to the collapse in meme and tech stocks. This equals a lack of potential demand if conditions to improve. It could take prices a very long time to recover as investors build back lazy cash balances – if they ever do to the magnitude spurred by the helicopter money poured on an entire generation of punters.

Adding salt to the wounds, with LUNA’s spectacular US$60 billion collapse still fresh in crypto investors’ minds, Monday also saw crypto lending platform Celsius announce it was suspending withdrawals and transfers, citing extreme market conditions. It’s been reported Celsius was holding $12 billion in clients’ funds over as many as 1.7 million accounts. Liquidity is a big issue for crypto, as prices fall, more and more accounts are forced to sell to cover losses, and more cash leaves the ecosystem never to return. Confidence is down, trust is broken. The lack of liquidity feeds on itself, and factor in the fact the ‘buy the dip’ crowd is gone because they’ve been burnt too many times – you get the sharp falls in prices we’ve seen over the past week.

Yes, prices are down, but so too is hope of a rally sufficient to recover the accumulated losses. Many newer investors have come into this asset class over the last 18 months, and along with stocks prices, they just assume if they hold on long enough, crypto prices will also go back up. Unfortunately, they’re now realising, it might take longer than they can bear, or worse, prices may never go back up…the harsh reality is some cryptos and some companies are never coming back.

Bitcoin, you broke my heart

It’s been a heartbreaking few months for the crypto faithful.

Since the start of the year, I’ve seen the social media chatter transition steadily from FOMO, lambos, rocket ship emojis and planned trips to the moon, to #HODL forever and buy the dip, to the current despair and resignation among millions of millennials’ that their dreams of retiring by age 25 is no longer viable. Whilst I’m a little past the used-by date in terms of retiring by age 25, I do HOLD some Bitcoin. I must admit it’s the one thing I break my trend-following rules on. I’m not sure why, there’s just something wonderful about the possibility Bitcoin represents… its sheer genius… its purity and infallibility… its cry of get stuffed with two fingers up to the incumbent financial system. There I go again, getting all Michael Saylor on you. Anyways, this week: Bitcoin, you broke my heart!

I was banking on the 25,365 and accompanying volume spike marking a significant swing low. A major shift in sentiment as a wave of forced selling from the LUNA-inspired 9-12 May drive lower hit substantial demand (12-15 May demand side candles). I know a bunch of selling came out (high volume) and I know it was soaked up at the lows by strong hands (demand-side candles). The candles on 30 May and 6-7 Jun were particularly strong. Promising, promising, promising.

Where I let my heart and my hopes eclipse my head and my better judgment, was betting against the short-term downtrend ribbon (yes, that bloody light pink zone again!). Much like with the COMP, it was once again Nostradamus-like in predicting where Bitcoin’s bear market rallies were doomed to fail. Since 48,228 it’s decisively killed at least four attempts to break the short-term downtrend.

Worse, the candles now look terrible on Bitcoin: Six consecutive supply-side candles in a row. Even worse, potential demand points at 27,877 and 25,365 were dispensed with barely a fight from the bulls – where is the demand? I explained that above…it’s potentially never coming back, or if it does, potentially a long time coming. At the time of writing, the low of the current candle is 24,891. A close below 25,365, but even more decisively, 25,000, would imply further losses are ahead. There’s a minor static support point at 24,298, but then very little holding Bitcoin up until the $20,000 handle.

Short- and long-term trends are firmly established to the downside – I couldn’t even contemplate dipping a toe in the water until I see a cluster of demand side candles on a volume influx at least as substantial as that witnessed at the 25,365 low, or alternatively, on a break back above the short-term downtrend ribbon, and even above 32,992 to be safe.

View: Bearish, sell rallies until a close above 32,992 (as much as I will continue to grimly HODL onto my own stash of Bitcoin to the bitter end).

Until next week,

Candle-out.

The views, information, or opinions expressed in the interviews in this article are solely those of the interviewees and do not represent the views of Stockhead. Stockhead does not provide, endorse or otherwise assume responsibility for any financial product advice contained in this article.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.