TECH HEAVY: Time to call in $10 trillion of Mega Tech earnings in the next 72 hours

Hi Zuck, you ranga? Via Getty

The Week on Wall St

Well. US sharemarkets just continue to casually edge further into record highs.

If US tech stocks were expected to underperform this year – having splurged without remorse from their late 2022 lows – well, there have been no signs of an impending comeuppance just yet.

But it’s a big week on Wall Street and these coming few days will be a major test of whether the Magnificent 7 can justify their Mega Tech titles.

Already this week, a laconic S&P500 clocked a fresh record high, as did the Best of Tech index, the Nasdaq 100 both indices boosted late by the US Treasury’s move to cut quarterly borrowing by a lazy US$55 billion to $760 billion in the first quarter.

Optimism of the slightly cautious kind pervades US markets which are looking out for a string of really big signals this week in the form of Wednesday’s headline US Fed’s interest rate call and the various big tech earnings calls which could do all sorts of funny things to Wall Street’s record‑breaking rallies.

Aside from Non-Farm Payrolls and the FOMC meet, US Q4 earnings is about to explode into life.

Enter Messrs Pfizer, Alphabet, Starbucks, AMD, Microsoft, Mastercard, Boeing, Qualcomm, Meta, Apple, Amazon as well as Exxon and Chevron Corp, among many others.

Artificial Optimism?

Wall Street just enjoyed a third week of gains and although the major indices ended Friday mixed, the overriding mood is still positive amid the recent AI-driven optimism.

Out front again was new king on the block, Microsoft, which reclaimed the title of Wall Street’s most valuable company as its share price rose to all-time highs and its market cap exceeded $3 trillion.

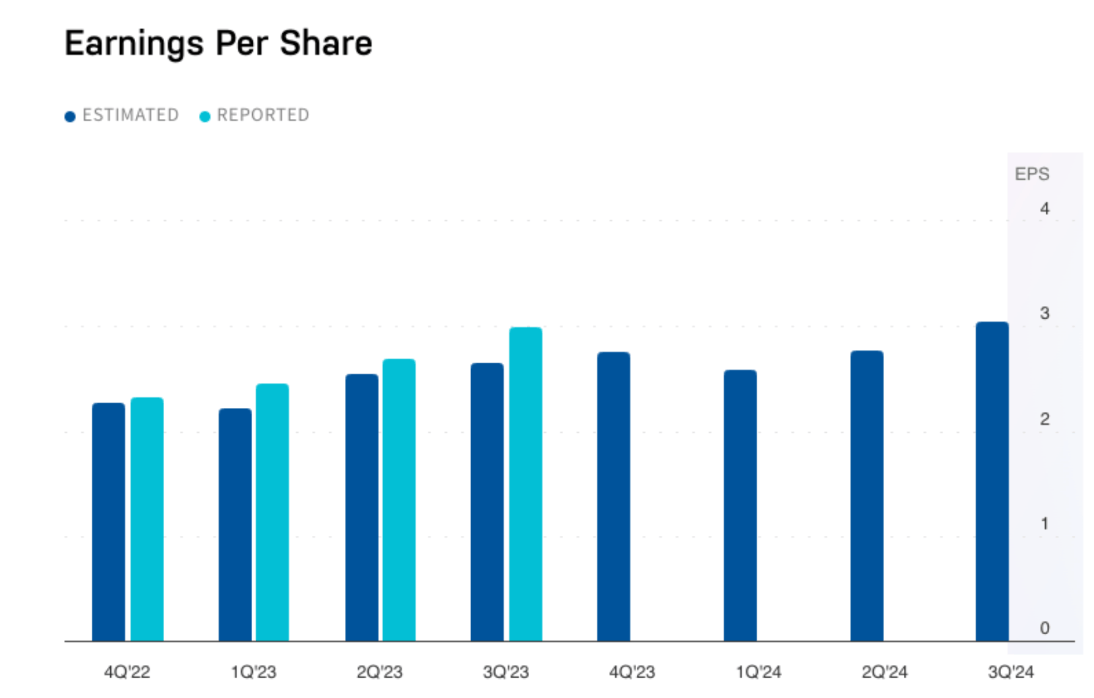

Microsoft Projected (EPS)

Kyle Rodda at Capital.com says the milestone comes as investors back the company as the market’s leader in artificial intelligence, courtesy (in large part) due to its acquisition of a significant share of OpenAI.

“Investors will watch Microsoft’s Q2 results for signs that it is executing its AI strategy and monetising the hype surrounding the burgeoning technology. Analysts forecast a nearly 20% rise in EPS from a year earlier to $2.77 per share on a lift in revenues to US$61.12 billion.”

But with four other equally monstrous tech names unwrapping some US$10 trn in earnings between Tuesday and Thursday, XM CEO Australia Peter McGuire says those bullish bets will be put to the test.

Microsoft and Alphabet set to report their results tonight, followed by Apple, Meta and Amazon on Thursday.

“A cautiously risk-on tone ahead of a very busy week for the markets that’s expected to get heated up mid-week by the Fed’s policy decision, culminating with the latest payrolls report on Friday.

“After a week of yet more upbeat economic indicators out of the United States, the soft landing narrative remained intact as the inflation data went in the opposite direction.”

The bigger-than-expected drop in core PCE on Friday underscores the view that US price pressures are cooling, McGuire told Stockhead.

“Paving the way for a rate cut sometime in the spring.”

“But investors remain split as to the likelihood of the Fed chopping 25 basis points off the Fed funds rate as early as March, so the focus for the January meeting is entirely on what clues the FOMC statement and Powell’s commentary will offer on the timing.”

So far, the data has been moving in policymakers’ direction.

“The Fed has to tread carefully as the labour market is still churning out jobs at a solid pace. Chair Powell risks getting investors’ hopes up by not reining in expectations, only for them to be dashed if Friday’s jobs report surprises to the upside again.”

On the corporate front, Netflix shares surged almost 20% last week after the streamer smashed forecasts by adding new revenue to its flood of businesses with live streaming and ad-revenue gaining traction as it delivered its best quarter of growth since the pandemic.

Meanwhile, Air BnB (ABNB) stock surged 6% on Friday after the company announced it’ll increase guest service fees for cross-currency bookings.

Starting April 1, guest service fees for bookings paid in a currency different from the listing will increase by as much as 2%, with total guest service fees increasing from less than 14.2% to up to 16.5%.

JPMorgan believe that the new cross-currency fee could lift 2024 & 2025 revenue by ~2% & EBITDA by ~4%-6%, which the punters have taken note of.

Finally, the former US President Donald Trump smoked the former South Carolina Gov. Nikki Haley in Tuesday’s New Hampshire primary, moving the great orange fiend an infamy closer to a general election reshowdowndeathmatch with former young person, the incucumbent President Joe Biden.

The ex-president secured 47.3% of the vote, according to exit polls via Real Clear Polling.

Elon Watch

I don’t see why this needs Elsplaining:

Inner demons can be helpful pic.twitter.com/EcOlXdGbRU

— Elon Musk (@elonmusk) January 28, 2024

This however, probably needs more Elsplaining than I can possibly unearth:

The first human received an implant from @Neuralink yesterday and is recovering well.

Initial results show promising neuron spike detection.

— Elon Musk (@elonmusk) January 29, 2024

Elon’s Tesla (TSLA) meanwhile, is likely to generate plenty of noise once again this week as investors and analysts weigh the premium valuation in light of the lowered unit volume expectations.

US Earnings

Tuesday January 30 – Friday February 2

Five Mega Tech stocks boasting a combined market cap of more than US$10 trillion will report earnings this week. All eyes are on Microsoft, Alphabet, Meta Platforms, Amazon and Apple which are on deck between Tuesday and Thursday.

Tuesday

General Motors (NYSE:GM), United Parcel Service (UPS), Sysco (SYY), Pfizer (PFE), Alphabet (GOOG), Microsoft (MSFT), Starbucks (SBUX), Mondelez International (MDLZ), and Advanced Micro Devices (AMD).

Wednesday

Phillips 66 (PSX), Boeing (BA), Mastercard (MA), MetLife (MET), Qualcomm (QCOM), and Boeing (BA).

Thursday

Merck (MRK), Honeywell (HON), Altria (MO), Amazon (AMZN), Apple (AAPL), Meta Platforms (META), Royal Caribbean Cruises (RCL), and Post Holdings (POST).

Friday

Exxon Mobil (XOM), Chevron (CVX), AbbVie (ABBV), and Charter Communications (CHTR).

5 ways this all might go sideways

deVere Group CEO Nigel Green says investors this week will be looking for the best buy cues for artificial intelligence (AI) technologies.

“The S&P 500 index is pushing further into record territory, and this is mostly down to the tech titans,” Green says. “These megacaps were also the drivers of most of the index’s 24% gain in 2023.”

“This reporting season for these five major tech companies holds immense significance for investors as their performance not only influences sector-specific trends but also serves as a bellwether for broader market and economic sentiment.”

Here’s 5 reasons why Green reckons this week is when earnings go “critical” for Big Tech.

1. Market barometers

“The combined market value of these five tech behemoths is a staggering reflection of their influence on the broader market. Investors often view these companies as barometers for the health of the technology sector and, by extension, the overall economy. A strong earnings performance from these giants can provide a positive sentiment boost to the entire market, while any signs of weakness may lead to increased market volatility.”

2. Leadership in the S&P 500

“The rally in the stock market last year was notably fuelled by megacap tech stocks. As investors continue to place significant emphasis on the potential of AI services offered by these tech giants, their earnings reports will be scrutinised for insights into the sustainability of this leadership and its impact on wider market trends.”

3. Tech’s role in economic growth

“The tech sector is now a linchpin in driving economic growth. The reliance on digital services, cloud computing, and e-commerce has surged, and these companies are at the forefront of these trends. A strong earnings season from tech leaders would signal a continuation of the sector’s pivotal role in supporting economic growth, influencing investor confidence,” noted the deVere CEO.

4. AI and innovation

Green explains: “Investors are excited by the promises and possibilities of artificial intelligence (AI) services. Companies like Microsoft, Alphabet, and Nvidia have been leading the charge in AI innovation, and their earnings reports will be closely monitored for updates on advancements, partnerships, and commercialization of AI technologies. Positive signals in this regard will drive enthusiasm among investors looking for exposure to cutting-edge technologies.”

5. Consumer behaviour and e-commerce

“Amazon and Apple, in particular, are closely tied to consumer behaviour and spending patterns. Amazon’s performance is a key indicator of the strength of e-commerce, while Apple’s earnings shed light on consumer demand for tech products. As these companies navigate global challenges and evolving consumer preferences, their earnings reports provide valuable insights into economic trends and potential shifts in consumer behaviour.”

The Economic Calendar

Monday January 29 – Friday February 2

Non-farm Payrolls drop on Friday night, which could see the US make a small shift either way on the date for a first Fed rate cut – currently fully priced in for May.

TUESDAY

Japan Unemployment Rate (Dec)

Eurozone GDP (Q4, flash)

Eurozone Economic Sentiment (Jan)

Mexico GDP (Q4, prelim)

United States S&P/Case-Shiller Home Prices (Nov)

United States JOLTs Job Opening (Dec)

United States CB Consumer Confidence (Jan)

WEDNESDAY

Japan BoJ Summary of Opinions (Jan)

China (Mainland) NBS PMI (Jan)

Japan Consumer Confidence (Jan)

Germany Retail Sales (Dec)

Germany GDP (Q4, flash)

United States ADP Employment Change (Jan)

United States Fed FOMC Interest Rate Decision

Brazil BCB Interest Rate Decision

THURSDAY

Worldwide Manufacturing PMIs, incl. global PMI (Jan)

South Korea Trade (Jan)

Eurozone Unemployment Rate (Dec)

United Kingdom BoE Interest Rate Decision

United States ISM Manufacturing PMI (Jan)

FRIDAY

South Korea Inflation (Jan)

France Industrial Production (Dec)

United States Non-farm Payrolls, Average Hourly Earnings,

US Unemployment Rate (Jan)

United States UoM Sentiment (Jan, final)

United States Factory Orders (Dec)

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.