Tech-Heavy: Nvidia reckons ‘every $1 spent on a GPU returns $5’ – and experts agree

Via Getty

ON Wall Street last week, US Q1 earnings season got its fairy tale finish after Nvidia (NVDA) produced another super steely set of results, with revenue of US$26bn ahead of estimates at circa $24.5bn.

Nvidia’s stock will now trade under US$200 for the first time in 16 months in just over a week, after the chipmaking darling splits its stock 10-to-1.

This means its shares will go from trading at about US$1,064 to US$106. The stock has simply gotten too big, too fast, too strong – it’s risen more than 600% since the start of 2023, rallied once again following the result, helping push the Nasdaq 100 to a record close on Friday.

Nvidia’s shares have rallied over 20% on average to a new high following its prior splits.

The 10-for-1 forward stock split will go into effect after the market closes on June 7, the company said.

Stock splits don’t alter your basic share price fundamentals in any way, but merely have the effect of making the underlying stock more affordable, which can have a positive psychological impact on retail investors.

Stock splits are a fairly common strategy, with companies including Alphabet, Amazon and Tesla all orchestrating similar stock splits in 2022. When the change goes into effect on June 7, all Nvidia common stockholders will receive an additional nine shares.

It’s happened quickly – the price of Nvidia’s stock has gained more than 25 times in the last five years.

Nvidia CEO Jensen Huan, who as of Friday last was the world’s 17th-richest person, according to Forbes, now has an estimated US$91 billion to his name.

That’s more than double what he was worth last Christmas, Bloomberg notes.

On Friday when the chipmaker dropped its quarterlies, Huang likewise dropped a bomb of hints that Nvidia was only getting started. He expects sales to increase with the launch of its upcoming new graphics processing unit, called Blackwell, later this year.

“The next Industrial Revolution has begun. Companies and countries are partnering with Nvidia to shift to the trillion-dollar installed base of traditional data centres to accelerated computing and build a new type of data centre, Ai factories to produce a new commodity, artificial intelligence.”

The transformation, Huang says, enables productivity gains to almost every industry from cost and energy efficiency savings while expanding revenue opportunities.

That’d put quarter-on-quarter growth of 18% vs 11% expectations. EPS (earnings per share) of $6.12 slightly beat estimates for $6.09, q-o-q, but a staggering 461% jump in EPS on the first fiscal quarter of last year.

Likewise, Q1 revenue is up 262% y-o-y, and the only rider is that the chip-making behemoth will be challenged to keep up with demand for its AI graphic processors.

The cracking numbers smacked the already ionospheric expectations of Wall Street, but more importantly for investors and the stock’s 90% YTD gains, NVDA iced it by offering glittering Q2 guidance, well above analysts’ similarly glittering consensus.

Sky-high valuations?

During the quarter, Nvidia bought back $7.7 billion worth of its shares and paid out $98 million in shareholder dividends.

Going forward, the company intends to increase its cash dividend from four cents per share to 10 cents on a pre-split basis, so when the split comes into effect, the new dividend will amount to a penny per share.

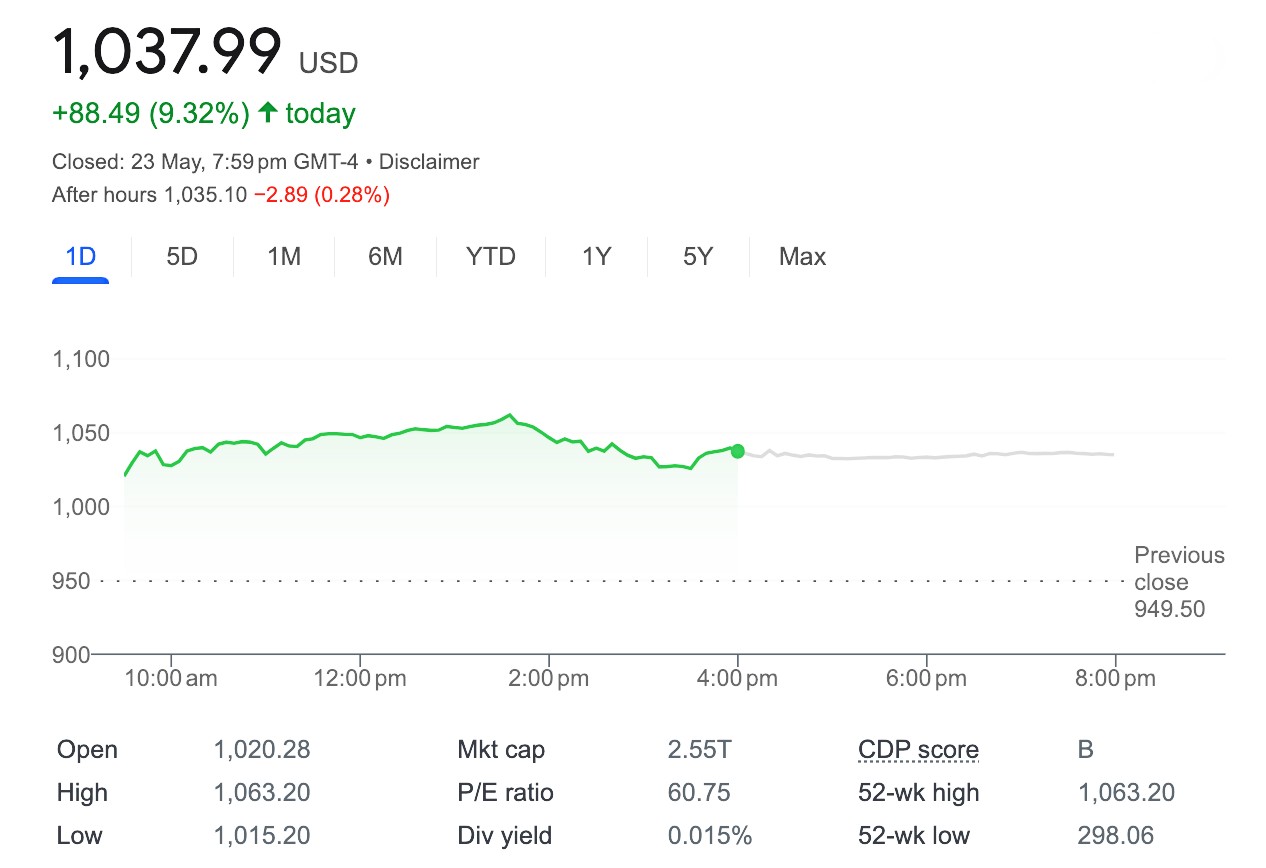

The stock price is up more than 9% in after-hours trading, surpassing $1,000 and increasing its lead over the other Magnificent 7 stocks.

NYU’s Aswath Damodaran told US media last week that Nvidia has taken up the torch, where other momentum trades flickered out like Meta, Google, Apple and Tesla.

“It is testimonial to the power of momentum, everything they touch turns to gold,” Damodaran said on CNBC.

Yet, according to XM Australia CEO Peter McGuire, from a valuation perspective Nvidia is far from being the most overvalued among the mega caps and is comparable to Amazon and Microsoft when looking at their forward 12-month price/earnings ratios.

“This underlines the ongoing attractiveness of the Big Tech despite the stratospheric rise in their share price, as most of them have been able to deliver on the earnings front.

“The few such as Tesla that haven’t, have been brutally punished by the markets,” Peter told Stockhead.

Dan Ives, Wedbush Securities managing director, has been beating the Jensen Huang Fan Club drum and to his credit, the Godfather of AI – as described by Ives – has delivered again with the 1Q25 earnings.

Ives described the results as “a Masterpiece quarter”.

Michael Frazis from Frazis Capital Partners pointed to Huang’s commentary on the financial multiplier effects for Nvidia customers.

Huang set the phones buzzing during the conference call, saying every US$1 of spend on a GPU returns US$5 in earnings to the hyperscalers over a four-year period, equating to a one-year payback. Every US$1 spend on the H100 (Hopped) servers equates to US$7 in revenue over a four-year period.

Frazis says his math adds up to those kinds of numbers too.

Huang also said there’s more to look forward to, with the imminent launch of Nvidia’s next-generation Blackwell GPUs set to drive even more growth later this year.

“We will see a lot of Blackwell revenue this year,” he said, adding that he expects it to arrive in data centres by the fourth quarter.

Wait there’s more.

The company said it was seeing strong demand for its networking components, which are quickly becoming just as important as its GPUs.

That’s because data centre operators are looking to build clusters of tens of thousands of chips that must be interconnected with one another, to power more advanced AI workloads. Networking-related sales came to US$3.2 billion during the quarter, up threefold from a year earlier, primarily thanks to sales of InfiniBand products.

NVDA Q2 guidance of $28bn revenue

NVDA Q2 guidance of $28bn revenue

Forward guidance was so far ahead of expectations (of $24.5bn), it was beautiful to the point of anxiety inducing.

Morgan Stanley called it the quarter of “shock and awe” when US$10bn revenue in revenue against the US$28bn guided this time around for 2Q25.

What we’ve just seen may’ve been the last gimme of a quarter for NVDA. With the big guns now throwing everything they can at the AI space, NVDA’s bag of tricks is no longer bulging like Santa’s stocking.

Superlative growth rates and the ability to beat-and-raise from here are going to become more difficult.

Morningstar’s NVDA analyst and equity strategist Brian Colello disagrees.

“Nvidia once again reported stellar quarterly results and provided investors with even rosier expectations for the upcoming quarter, as the company remains the clear winner in the race to build out generative artificial intelligence capabilities. We’re encouraged by management’s commentary that demand for its upcoming Blackwell products.”

“We raise our fair value estimate to $1,050 from $910 as we model stronger data center revenue growth over the next several quarters while maintaining our longer-term growth rates from a higher installed base of AI equipment,” Brian says.

“Shares were up about 6% on the earnings report, and we think the reaction is justified and view shares as fairly valued.”

Barely four minutes into their conference call, management made some comments that were greeted very positively by investors – that for every $1 spent on NVIDIA AI infrastructure, Cloud Service Providers (CSPs) have an opportunity to generate $5 in GPU monetisation over four years.

In an environment where speed matters, NVIDIA’s rich software stack and ecosystem, and tight integration with cloud providers, makes it easy for end-customers to get up and running on NVIDIA GPU in a public cloud.

In turn, this is allowing management to extend their optimism further, suggesting that demand may exceed supply “well into next year”.

Whilst customers will no doubt want viable competitors, in the near-term, the risk of “experimenting” with another GPU is too great and this is being evidenced by customers still taking delivery of the Hopper GPUs, despite the more powerful Blackwell GPU to be shipped later this year (i.e., customers are not delaying purchases of the old GPU so they can receive shipments of the new GPU, like we traditionally see when new models/versions of a product are to be released).

Additionally, and more unexpectedly, the customer base is finally starting to broaden with enterprise ticking up and revenue from sovereign-driven projects ramping much faster than expected (see more below).

Divisionally, it was no surprise that the Data Centre business is now the main focus:

Segments and numbers

Gaming revenues fell 8% quarter-on-quarter, much worse than expected and now accounts for just 10% of sales. Automotive sales rose a very strong 17%, 2x expectations, following continued growth of NVDA’s cockpit solutions and self-driving platforms (Level 3 autonomy vehicles have “environment detection” and can make informed decisions for themselves, such as accelerating past a slow-moving vehicle… they also require very advanced algorithms and much larger learning models.

NVDA delivered another quarter of record Free Cash Flow generation at ~$15bn (~58% FCF margin) taking its cash balance to ~$31bn. Given the very strong FCF generation, share repurchases jumped to ~$7.8bn and analysts model this growing to over $10bn through 2025 (>$40bn p.a.)

NVDA also followed in the steps of other mega tech names by announcing a 10-for-1 stock split, which no doubt will further enhance retail participation.

The average Price Target for NVDA increased from US$1,025 to US$1,164 (almost 15%), on the back of 7%-12% EPS upgrades for 1 / 2-year forward EPS.

US$400bn in market cap was added post the March quarter result, which might have been boosted by the announced 10-for-1 stock split. The split has no bearing on the financial outlook, rather a tilt of the goodwill hat to retail investors to increase share purchase availability.

With a US$2.6trn market cap at US$1065 per share, Nvidia could reach US$3trn (15% upside) according to Ives in 2025, thereby superseding Apple at its current valuation and making it the second largest listed US company, after Microsoft.

When it comes to price targets post earnings, analysts implemented an across-the-board upgrade cycle.

Morgan Stanley sits at the more conservative end at US$1160 with Goldmans Sachs and UBS at US$1200, stretching to Jeffries at US$1350 a

LGT Crestone has NVDA up top of its Best-in-Sector List /at US$1,026.39 (+8.2%).

The Consensus Recommendation for NVDA is a Buy and the Price Target is US$1,164.15.

The AI effect

A solid quarter for earnings

All three of the major US indices managed to more than recover from the April pullback to notch up fresh record highs on the back of the stellar earnings season.

From the 93% of S&P 500 companies that had reported as of May 17, 60% posted better-than-expected revenue, while earnings on average grew by 5.7% in Q1, making it the best quarter since Q2 2022 according to FactSet.

Nvidia is worth $2.6 trillion — larger than two Metas, three Berkshire Hathaways, or five ExxonMobils. Goldman Sachs called it “the most important stock on planet Earth” for its centrality in the booming AI industry, and his company will likely be worth more than Apple in a few months.

Last week on Wall Street, the S&P500 managed to close slightly higher, clinching a sliver-then fifth straight week of gains, the US benchmark’s longest winning run since just after ‘Straya Day.

That was mainly thanks to Nvidia’s +7% after hours surge on Wednesday, where the chipmaker busted through the $1,000 level for the first time on the back of stunning quarterly results and even better guidance.

Yet, truth be told, after clocking its latest fresh record high on Tuesday in New York, US stocks have largely sat back on their haunches sucking in the big ones as that growing cloud of interest cut mystery continues to gather round Mount Federal Reserve.

T’were those FOMC minutes, the hawky-talky coupled with the unwelcome good economic data, which dented US sentiment last week.

Of course, the Nasdaq Comp got a revivifying shot in the arm when NVDA smashed them haughty Wall Street expectations.

The US Week Ahead

Monday May 27 – Friday May 31

Monday:

US Memorial Day holiday

Germany Ifo business climate (May).

Tuesday:

US Case-Shiller Home Price Index (March)

US consumer confidence (May).

Wednesday:

Germany consumer confidence (June).

Earnings: HP, Salesforce, UiPath.

Thursday:

Switzerland economic growth (Q1).

Earnings: Costco, MongoDB, Zscaler.

Friday:

US PCE inflation (April)

Eurozone flash inflation (May)

Canada economic growth (Q1),

India economic growth (Q1).

The Economic Calendar

Monday May 27 – Friday May 31

MONDAY

BOJ Gov Ueda Speech

CN Industrial Profits (YTD)

JP BOJ Uchida Speech

JP Coincident Index Final MAR

JP Leading Economic Index Final MAR

DE Ifo Business Conditions MAY

EU 20-Year, 3-Year Bond Auction

ECB Lane Speech

TUESDAY

AU Retail Sales MoM Prel APR

ECB Schnabel Speech

US Fed Mester Speech

Germany Wholesale Prices YoY

Germany 10-Year Bund/g Auction

WEDNESDAY

US Money Supply APR

US Fed Cook Speech

12:00 PM

AU Westpac Leading Index

AU Construction Work Done

AU Monthly CPI Indicator APR

JP BOJ Adachi Speech

JP Consumer Confidence MAY

Ger GfK Consumer Confidence JUN

Inflation Rate YoY Prel MAY

FR Consumer Confidence MAY

FR Retail Sales MoM APR -0.5% 1.0%

EU Loans APR

EU M3 Money Supply YoY APR

US MBA 30-Year Mortgage Rate MAY

US Mortgage Market Index MAY

IN M3 Money Supply YoY MAY/17 11.1% 10.9%

US Redbook YoY MAY

THURSDAY

US Richmond Fed Manufacturing Index MAY

US Dallas Fed Services Index MAY

US 2-Year FRN Auction

RU Industrial Production YoY APR

US Fed Williams Speech

US Fed Beige Book

US API Crude Oil Stock Change MAY

AU RBA Hunter Speech

US Fed Bostic Speech

GB Car Production

JP Foreign Bond/ Stock Investment by Foreigners MAY

AU Building Permits MoM Prel APR

AU Building Capital Expenditure

AU Plant Machinery Capital Expenditure

AU Private Capital Expenditure

AU Private House Approvals MoM Prel APR

JP 2-Year JGB Auction

Unemployment Rate APR 7.2% 7.3% 7.3%

08:00 PM

EU Economic Sentiment MAY

Unemployment Rate APR

Consumer Confidence Final MAY

Consumer Inflation Expectations MAY

Industrial Sentiment MAYSelling Price Expectations MAY

Mex Unemployment Rate APR

US GDP Growth Rate

US Corporate Profit

US Goods Trade Balance Adv APR $-91.83B $-91.8B $-93.0B

11:30 PM

US Initial Jobless Claims MAY

US Retail Inventories Ex Autos

US Wholesale Inventories MoM

US Continuing Jobless Claims MAY

US Core PCE Prices

US GDP Sales

FRIDAY

US Pending Home Sales

US EIA Crude Oil Stocks Change

US Fed Williams Speech

US Fed Logan Speech

KOR Industrial Production

KOR Retail Sales MoM APR

JP Unemployment Rate

JP Tokyo Core CPI

AU Housing Credit

AU Private Sector Credit

CN NBS Manufacturing PMI MAY

CN NBS Non Manufacturing PMI MAY

CN NBS General PMI MAY

JP Housing Starts YoY APR

JP Construction Orders

FR Non Farm Payrolls

AU Commodity Prices YoY MAY

FR Inflation Rate YoY Prel MA

FR GDP Growth Rate QoQ Final

FR PPI MoM APR

GB BoE Consumer Credit

EU Inflation Rate

US Core PCE Price Index

US Core PCE Price Index YoY APR 2.8% 2.7%

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.