Wall Street’s Friday session ended lower, but not enough, however, to prevent the S&P500 from recovering 1.7% and the tech-heavy Nasdaq from soaring by 3.5%.

Like relapsing internet addicts, the US Tech Heavy index returns in fits and waves to utterly dominate the hearts, minds and dopamine centres of global market participants.

For circa 20 years investors with a spare dollar and a sense of wonder for the impact of global digitisation haven’t even needed to think of what their options are. The bubble’s gone and burst every now and again over that time, but in the great, cunning scheme of things, there’s only one narrative for all of this and its trajectory is distinctly assurgent.

Bank of America’s ‘baby bubble’

Every so often a macro-economic reality might skewer a few companies with non-existent business models during the frequent periods of free money markets, but even for these, the consolidation is often short-lived and more so for the genuine mega tech names.

Especially since these companies seem to have found fresh buoyancy in the content-generating tools based on artificial intelligence – a still virgin playground, but all too synonymous with potential windfall. It’s a game for the cash rich and once again the American megacaps stand to benefit.

Bank of America calls them The Magnificent Seven – a nod to the 1960 film starring Yul Brynner, Steve McQueen and Charles Bronson. (And not the remake with Ethan Hawke, Denzel Washington and Starlord.)

BoA, in a note on Friday, pinned the latest unlikely tech bull market – rallying amid the ugly macro-environs of 2023 YTD – on the breathless hoopla around artificial intelligence (AI) with a particular nod to the potential of generative AI tools, most potently described in what the kids are doing with OpenAI’s ChatGPT right now.

BoA’s gunslingers, in order of appearance are Apple, Microsoft, Google, Amazon, Nvidia, Meta and Tesla. Tech-leaning, AI-dripping businesses trading on 30x price earnings (P/E) ratio vs 17x P/E for the rest of the S&P 500.

At a basic level, your (P/E) ratio is a handy measurement to double check just how expensive (or cheap) your company’s shares are.

The math is doable – by dividing the share price, (market value), of your company by its annual earnings (per share), you end up with a figure which fundies et al appear content with as a representation of the amount of money you’re paying for each dollar of its earnings.

And so, in mega cap Magnificent 7 land, that’s to say stockholders are paying around 30 times the results against 17 times on average for the rest of the rating in the United States.

For example, according to Tesla’s latest financial reports and current stock price, Elon’s current price-to-earnings ratio for the last (trailing) 12 months (TTM) is 47.0869.

Not the outrage it appears, considering that at the end of 2021 Tesla’s P/E ratio was 190.

On Friday, the boss of BofA’s investment strategy team thought it a good time to retrace the steps which led to the original and best bubble which emerged during 1999 as an investment vortex lifted the Nasdaq into the ionosphere around 5,000 points.

The cost of money, under Fed Chair Alan Greenspan, had been liquid and delicious for so long no one knew better. But the F/E ratio (Ferraris in the carpark, divided by average employee) suggested perhaps that the speculation in internet stocks might require the teeniest of monetary tightening.

The dot-com bubble, now so enormous it was sucking up sleeping children from their own beds, exploded in shocking glory a few months thereafter.

Michael Hartnett, chief investment strategist at Bank of America Global Research, is the chap late last week who said AI is the new engine behind the current “baby bubble.”

Hartnett recalled, with some small degree of pleasure I felt, that from March 2000 the Nasdaq through a combination of intermittent fasting and outright purging lost circa 80% of its 5000 in about 20 months.

It’d need another 15 years of incredible technological development to retrace its way back to the 5,000 mark.

And right now, he says, the din around AI is drowning out much of what else is roiling markets.

OpenAI’s ChatGPT has fired the imagination around what money might be made with the celeverest of open-language, chatbot and generative AI.

Making out real good right now is Nvidia. So is Meta. Those companies have seen their stock easily more than double year to date.

AI, the big betters posit, could rebuild the dead duck of advertising at Facebook. Nvidia’s apparently the best placed chipmaker to make hay out of generative AI.

And once again, the headline names with cash to burn are leaving a trail of breadcrumbs for the rest to follow. ARK Invest’s Cathie Wood says Tesla stock will be worth 22 million gold bars by Christmas. Bill Ackman’s turned heads by pouring a cool billion into Google daddy Alphabet, on exactly the same thesis that’s reinvigorating Facebook’s mama.

“Bubbles in right things (e.g. Internet) & wrong things (e.g. housing) always started by easy money, always ended by rate hikes” (and) “AI = internet,” Hartnett says.

So the implication broadly enough is that on Wall Street, there’s simply no indexation without these companies which have almost single-handedly provided the momentum that’s pumped the rise of the S&P500 and the Nasdaq since New Year.

It’s even easier to see how that might be possible by isolating one name from the rest.

Apple.

Last month I read this which I leave to you verbatim from a chap on CNBC (so apologies for US spelling).

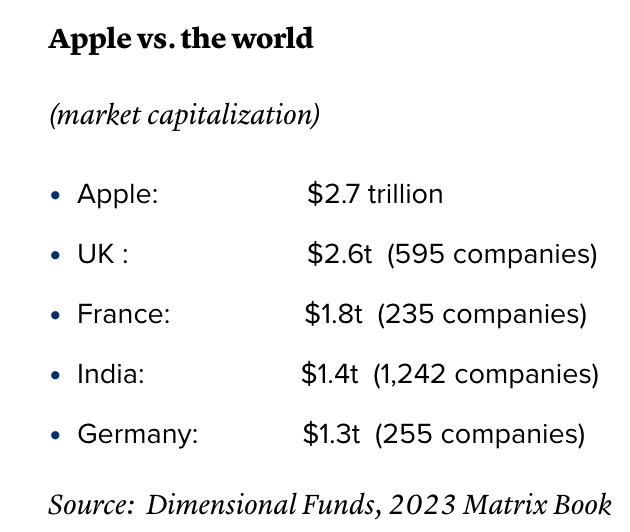

Dimensional’s Matrix Book is an annual review of global returns that highlight the power of compound investing. It’s a fascinating document: you can look up the compounded growth rate of the S&P 500 for every year going back to 1926.

Buried on page 74 is a chapter on “World Equity Market Capitalization,” listing the market capitalization of most of the world, country by country. No surprise, the U.S. is the global leader in stock market value. The $40 trillion in stock market wealth in the U.S. is almost 60% of the value of all the equities in the world.

Here’s where it gets fun.

My friend Ben Carlson pointed out that Apple’s current market capitalization of about US$2.7 trillion this week exceeds the entire market capitalization of the United Kingdom, the third biggest stock market in the world.

Not only is Apple bigger than all 595 companies that list in the United Kingdom, it’s bigger than all the companies in France (235 companies), and India (1,242 companies).

Apple is twice the size of Germany’s entire stock market, with 255 companies.

Via CNBC

Apple is bigger than the entire LXE.

Apple is twice the size of not only the Frankfurter Wertpapierbörse (FWB or the Frankfurt Stock Exchange), but also Germany’s six other exchanges combined.)

So this is just how powerful the investment predilection for US tech and growth stocks is.

I would think it’s worth adding that the Bank of America also cited their European counterparts, but in luxury, with LVMH , L’Oréal , Hermès , Christian Dior , Compagnie Financière Richemont , Kering and Ferrari, all worth taking note of for their stupendous 2023.

“Les Sept Magnifique” average PER clocks at about 36 times, compared to 12 times at STOXX Europe 600.

Which gives us x2 categories of Magnificent Seven, one powered by AI and the other by the vagaries of fashion, the bored rich, and the strengthening of the upper middle-class in Asia and beyond.

Elsewhere

There was a lot of geopolitics on the menu over the weekend:

The Japanese G7 gave hideous birth press releases which upset China, particularly concerning the the China Sea and Russia.

The timing was pretty good for China to then exercise some economic reciprocity upon the US, publishing a rare decision to banish forthwith the American chipmaker MicronTechnology from its infrastructure, saying something to the tune of the chips not being sufficiently reliable in terms of cybersecurity.

The Cyberspace Administration of China on Sunday announced that the company’s products presented “serious network security risks.”

The decision to ban local firms from using the chips was as the emperor has foreseen what with ever-escalating tensions between the two global superpowers who alternate with tedious regularity between sulky and outraged.

It is however, China’s first retaliatory sanction following America’s almost complete ban on any semiconductor flirting with China.

On the plus side, Korea’s burgeoning semiconductor suppliers are on the rise already this week, looking good as an alternative semiconducting option.

On the negative side, and in his defence, he was a bit distracted by the debt ceiling stuff, US president Joe Biden, and probably picked the wrong moment to come out of the G& in Hiroshima to declare with an octogenarian’s innocent smile, that US ties with China are probably past the worst and would be tempered very soon.

In Ukraine, Russia’s Wagner group said it’s finally taken the pile of blood and rubble that is Bakhmout, which I believe is Russian for Deathtrap. (At about midday in Paris, there’s reports Ukraine was counter-attacking, although Moscow is also claiming the capture of the city.)

Like the fog of war, Kiev has responded by indicating its troops are seeking to encircle the area (it’s a trap!).

It’s hella difficult to sort out information from propaganda. But after turning up at the G7, it looks like the United States authorised the use of F-16 fighters by Ukraine. Uncle Joe Biden says he’s received assurances that the jets would not be used on Russian territory. Just for pizza delivery, as F-16’s were originally purposed.

Elon Watch

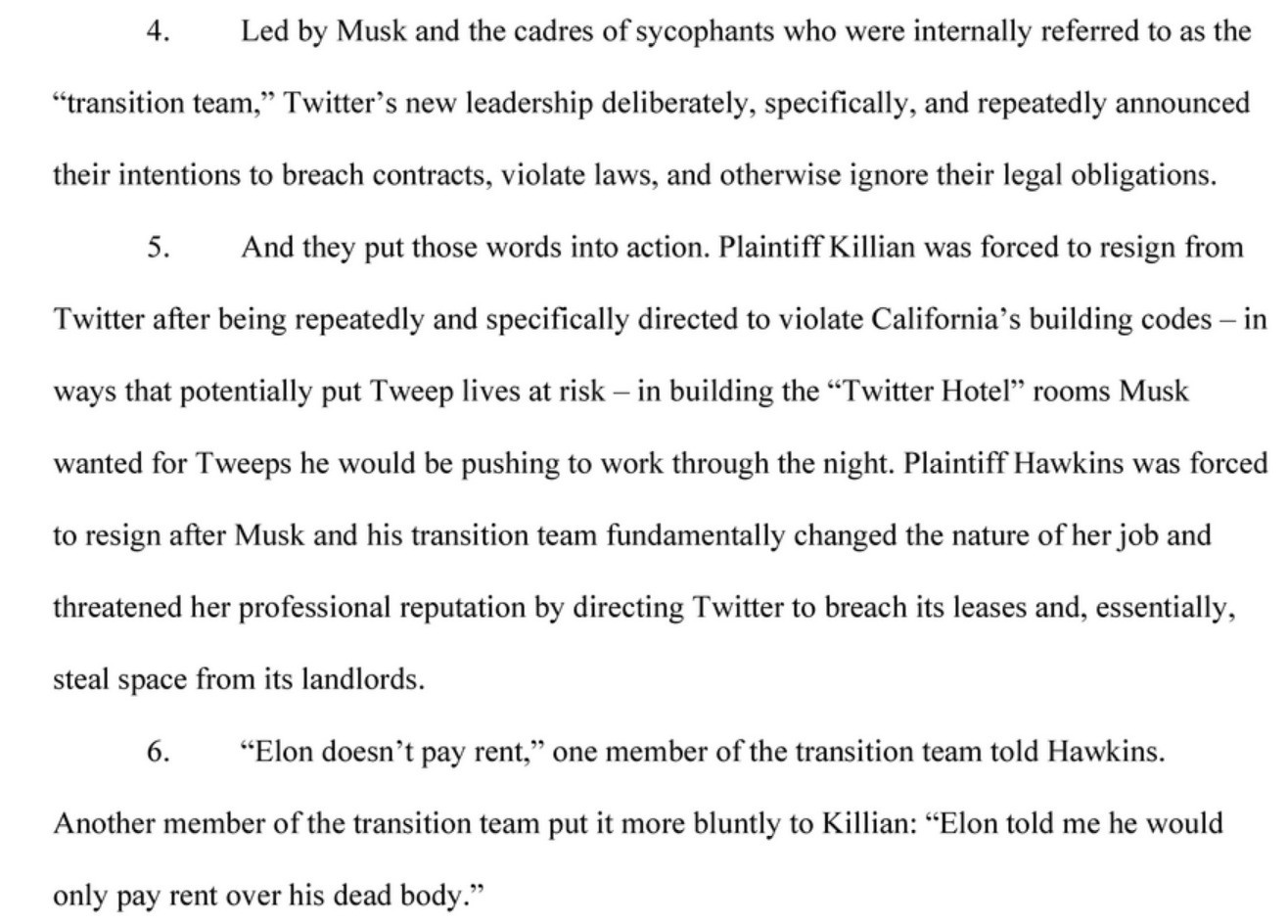

In a complaint, six former Twitter employees have denounced Elon’s reasonable idea to transform offices at Twitter HQ into bedrooms.

The terrifying San Francisco authorities who watch this kind of stuff have reportedly opened an investigation to verify whatever Elon’s being accused of.

The complaint, filed on May 16, accused Musk and Twitter of counts including fraud, and breaches of contract and labor-rights laws, and failure to pay severance. Everyone seems pretty embittered.

The complaint filed in Delaware is a pretty good read.

Wednesday, May 24 – Kohl’s (KSS), Analog Devices (ADI), Nvidia (NVDA), Snowflake (SNOW), and American Eagle Outfitters (AEO).

Thursday, May 25 – Royal Bank of Canada (RY), Best Buy (BBY), Dollar Tree (DLTR), Ralph Lauren (RL) and Costco (COST).

Friday, May 26 – Big Lots (BIG).

Nvidia (NVDA) – Reports after the close, Wednesday NY time

Nvidia reports its Q1 earnings in which investors will be hoping for more good news.

Wall Street expects Nvidia to earn 92 cents per share on revenue of US$6.52 billion, that vs to the year-ago quarter when earnings came to US$1.36 per share on revenue of US$8.29 billion.

eToro’s Josh Gilbert told Stockhead that shares of Nvidia have taken an impressive year so far and made an even more impressive show of it over the last four or five weeks.

They’re up and still upping – rising close to 15%, compared with the 1% rise in the S&P 500 index.

“But question marks now lie over its valuation with its rally this year.”

“The conversation of AI in the investment world has been rife so far in 2023, and earnings season in the US was no different, with thousands of mentions of AI on earnings calls from US tech. The investor excitement for this developing technology has sent Nvidia’s shares soaring this year, and so far, the tech giant wears the crown for the S&P500’s best-performing stock of 2023,” Josh says.

On a year-to-date basis the performance looks even better. The graphics chip giant has gained over 116%, while the S&P 500 index has risen 9.34%.

Essentially, since bottoming in mid-October last year NVDA has become the pin up for AI and its potential.

But with the forward P/E now closed to 65, is it time to take profits, Josh asks?

“Nvidia is by far the market leader in developing graphics chips, and this is exactly what is needed to handle the complex calculations required to power AI applications, meaning investors believe Nvidia will reap the rewards from growing demand.

“However, outside of AI, the PC market is seeing considerable weakness affecting AMD and Intel this quarter. So the focus for investors will be if AI demand can offset other areas of weakness and if Nvidia can provide strong guidance for the rest of the year.”

Nvidia said in Q4 it expects to generate some US$6.5 billion in revenue – a big number, but has ambition gotten the better of Nvidia CEO Jensen Huang who’s declared that generative AI represents an “iPhone moment”?

Nvidia’s tied itself nicely to the entire narrative and scored the deals to back it.

Its star began to rise not only when the market awoke to the generative AI alarm bell, but its GPU data centre accelerators will likely form the spine of client Microsoft’s (MSFT) insanely large investments in its own AI infrastructure.

Meanwhile the Bank of America analyst Vivek Arya has been gushing for the business all year, calling Nvidia’s accelerated silicon, systems, software and developers the “full stack” which puts it in a position to “lead the nascent generative AI arms race among global cloud and enterprise customers.”

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our

Privacy Policy.

Get the latest Stockhead news

delivered free to your inbox

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our

Privacy Policy.