The Reserve Bank of Australia (RBA) will announce its next rate decision at 2.30pm Sydenham time, today.

All the expert punters agree it’s going to be a very close call.

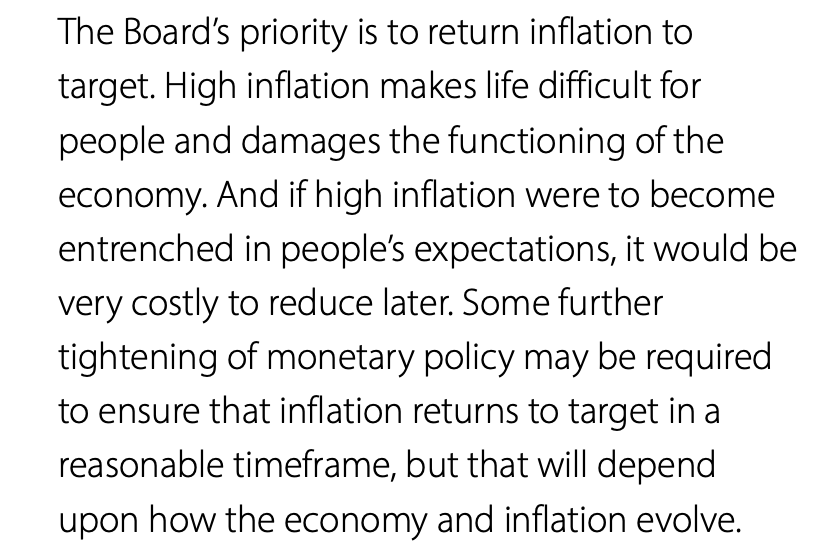

For me, and I’m no expert – although I make a point of reading the bank’s monthly Statement on Monetary Policy (SOMP) – I find the final few pars of the last SOMP always provide a bit of a tell on the next decision. Here’s what the SOMP left us with at the end of last episode (May).

Doing what’s necessary…

Via RBA SOMP May

…and then ending on this:

Via RBA SOMP May

To catch you up

Last month, the RBA board (pictured below, minus the people, but with a nice summary) surprised the market and raised the cash rate by 25bp to 3.85%.

Screenshot: Via RBA

It was the bank’s 11th rate hike in a cycle that began last May and has so far added a chunky 375bp to the cost of money in this lucky country.

Following the surprise 25bp cash rate increase in May, money markets are pricing in a 45% probability for another rate increase, after last week’s quirky ABS April CPI read which suggests, kind of, that inflation has been coming in a bit hotter than anticipated.

New research from the RFI Group suggests the biggest driver of the decline in consumer sentiment is our rapidly deflating take on Australia’s short term economic outlook,

“12 months ago, prior to the first of the RBA’s ten consecutive cash rate increases (and now 11 in 12 months), 39% of Australians anticipated Australia’s economic situation would worsen in the following 12 months,” RFI says.

Now, despite being 12 months into rate rises, it seems Australians are expecting things to get worse before they get better, with that number having grown to 59% (one of the highest levels on record).

Hotter inflation, slower growth

It’ll be a tough call for Governor Dr P. Lowe and his central bank accolytes on Tuesday. There’s pretty decent arguments on both sides of the table – to raise or to pause.

After several months of declines, inflation fired up again in April and is currently on track to overshoot the Reserve Bank’s forecasts for this quarter. Similarly, the latest quarterly data on wages showed an acceleration, fanning concerns of a wage-price spiral that keeps inflation burning for some time.

Such concerns were reinforced this week after the Fair Work Commission decided to raise the minimum wage by 5.75%, providing another boost to wage growth that could lead the RBA to adopt a more aggressive stance.

However, XM CEO Peter McGuire says there’s other elements suggest the RBA should take a cautious approach.

The labor market weakened in April, with the unemployment rate rising noticeably.

Retail sales stagnated as consumers turned more defensive.

The slowdown in China’s manufacturing sector continues to intensify, (which spells bad news for an Australian economy that relies on Chinese demand to absorb its commodity exports)

Combined, Pete says, these suggest economic growth has started to lose momentum.

“(But) if the RBA raises rates, the Australian dollar could benefit, although it’s questionable whether the currency can sustain a rally with the Chinese economy losing steam,” Pete adds.

This decision will be a close call

Hence, the question heading into Tuesday’s rate decision is whether the RBA will prioritise fighting inflation or supporting economic growth.

“So far, policymakers have been laser-focused on bringing inflation down, and with inflationary forces regaining strength, it will be hard for the RBA to do nothing,” McGuire says.

Markets are pricing in a 45% probability for a quarter-point rate increase, which seems relatively low considering the inflation dynamics.

The path of least regret

Tony Sycamore at IG Markets says the RBA in its last decision noted that while inflation had likely peaked, it was still too high, and a further increase was needed to return inflation to target.

“Given the importance of returning inflation to target within a reasonable timeframe, the board judged that a further increase in interest rates was warranted today.”

“The Board will continue to pay close attention to developments in the global economy, trends in household spending and the outlook for inflation and the labour market.”

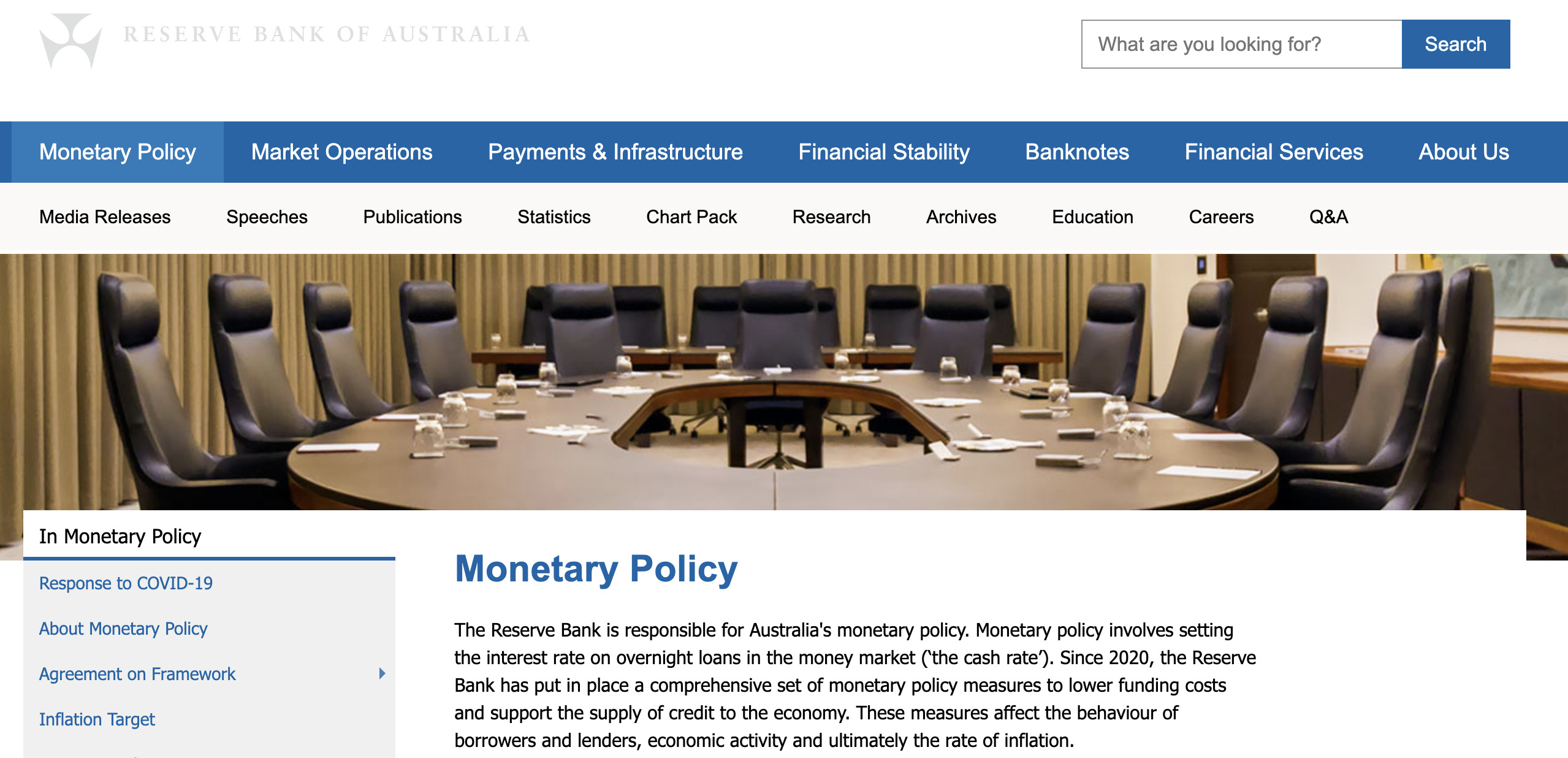

Via RBA

The RBA Cash Rate

Via IG

RFI: Sentiment – No one’s happy about it

While much attention remains on the cost-of-living crisis faced by lower-income Australians and the negative state of sentiment this brings, RFI research shows the past 12 months shows that no one is immune to current conditions.

“While Australians with lower personal income have consistently reported lower levels of consumer sentiment, those with higher income – managers & professionals, other white-collar employees, and not surprisingly those with a mortgage – are in fact reporting the biggest falls in sentiment over this period.

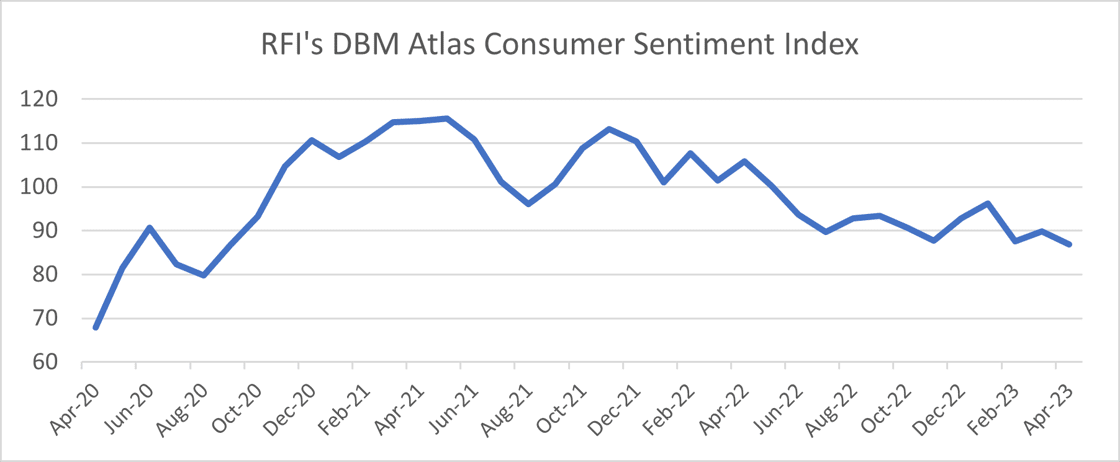

RFI’s DBM Atlas Consumer Sentiment Index fell to 87 in April (the lowest point since the pandemic) revealing continued pessimism consumers towards their personal finances and the Australian economy overall.

Via RFI Global

RFI says consumer sentiment is now at the lowest point since September 2020 – when Australians reacted to the Delta wave of the COVID19 pandemic – with data from RFI telling a worrying tale for Australian consumers and the organisations managing their finances.

RFI Global says it’s tracked the “continued stress of mortgage borrowers around the country,” throughout May.

“As well as extreme renter stress, depletion of savings buffers and increasing challenges facing those trying to enter the property market, which combined have amplified the dire state of consumer sentiment across the nation.”

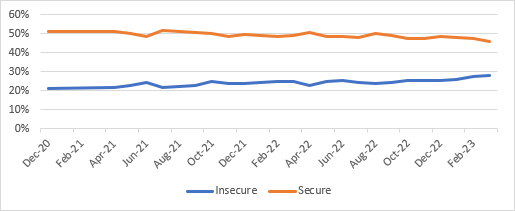

Financial (in)security blooms

Dig deeper and the RFI data uncovers pessimistic consumers feeling increasingly angst-ridden about their own financial security; with ‘the proportion of consumers who report feeling financially secure having fallen to 46% in April, after showing a consistent decline since the start of the year.’

Likewise, the proportion of Aussies who feel financially insecure has increased to 27% in April:

Via RFI Global

Sentiment lags as loan repayments grow

In addition to the steady decline in consumer sentiment, RFI is seeing changes in customer behaviour highlighting how macro-economic factors are impacting Australians.

Overall, Australians are increasingly saying they expect to struggle making their credit repayments.

Via RFI Global

RFI Global data shows the proportion of mortgage holders “who anticipate struggling to meet mortgage repayments in the next 12 months increased to a record high of 29% in March prior to the cash rate pause”.

The proportion of personal loan holders who expect to struggle to meet their loan repayments also increased to 14% in March 2023 (up from 9% at the end of 2022); and the proportion of credit cardholders who are paying interest on their credit card (RFi calls them ‘Revolvers’) increased to a record high of 38% in March 2023, from 24% in March 2022.

“As savings buffers are further eroded, it is likely that these metrics will continue to increase, and more customers will turn to credit to help them manage their budget.”

Sad enough for the RBA, says CBA

“We believe the domestic economy is now showing sufficient signs of slowing and we expect the RBA Board will judge that leaving the cash rate on hold is the appropriate policy move in June,” CBA wrote last week.

Current forward guidance from the RBA May Board Minutes is that, “members also agreed that further increases in interest rates may still be required, but that this would depend on how the economy and inflation evolve”.

“As we noted at the time, our take on this forward guidance is that the Board is willing to raise the cash rate again in this cycle,” CBA’s top economist Gareth Aird said on Friday.

“But another rate increase would require the economic data, particularly around inflation, GDP, the unemployment rate and wages/unit labour costs, to come in stronger than the RBA’s updated forecasts.

“Put another way, we do not think the RBA will lift the cash rate again if the economic data prints in line or weaker than their forecasts from the May Statement on Monetary Policy,” Aird reckons.

The 2023 May Commonwealth Budget has also been handed down since the May Board meeting, Gareth added.

“The RBA Governor agreed with our assessment that it does not add to inflationary pressures in the economy.

“Overall we expect the RBA to leave the cash rate on hold at the June Board meeting.

“But we expect the RBA to retain their forward guidance that – ‘further increases in interest rates may still be required, but that this would depend on how the economy and inflation evolve’.”

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our

Privacy Policy.

Get the latest Stockhead news

delivered free to your inbox

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our

Privacy Policy.