RBA boss Michele ‘Blunt Tool’ Bullock shows she’s a hawk of a different feather in terrifying Sydney inflation speech

Nobody move an inch... Via Getty

Last night the mask dropped – if not the dollar – after new-ish Reserve Bank governor Michele Bullock warned a stunned Australian Business Economists dinner that inflation here has quietly mutated into an awful, “homegrown” monster which will probably take circa two more years to tackle.

Homeowners spat out their soup and called their brokers to brace for more pain, when Bullock said she intends to wield the “blunt tool” of rate hikes “to serve the welfare of Australians, collectively”.

The problem – aside from goods and services costing heaps – is that the demands of getting your hair cut, going out for a feed or just opting to get your teeth cleaned are marching ahead “strongly” as simple daily services is running ahead of supply in this country.

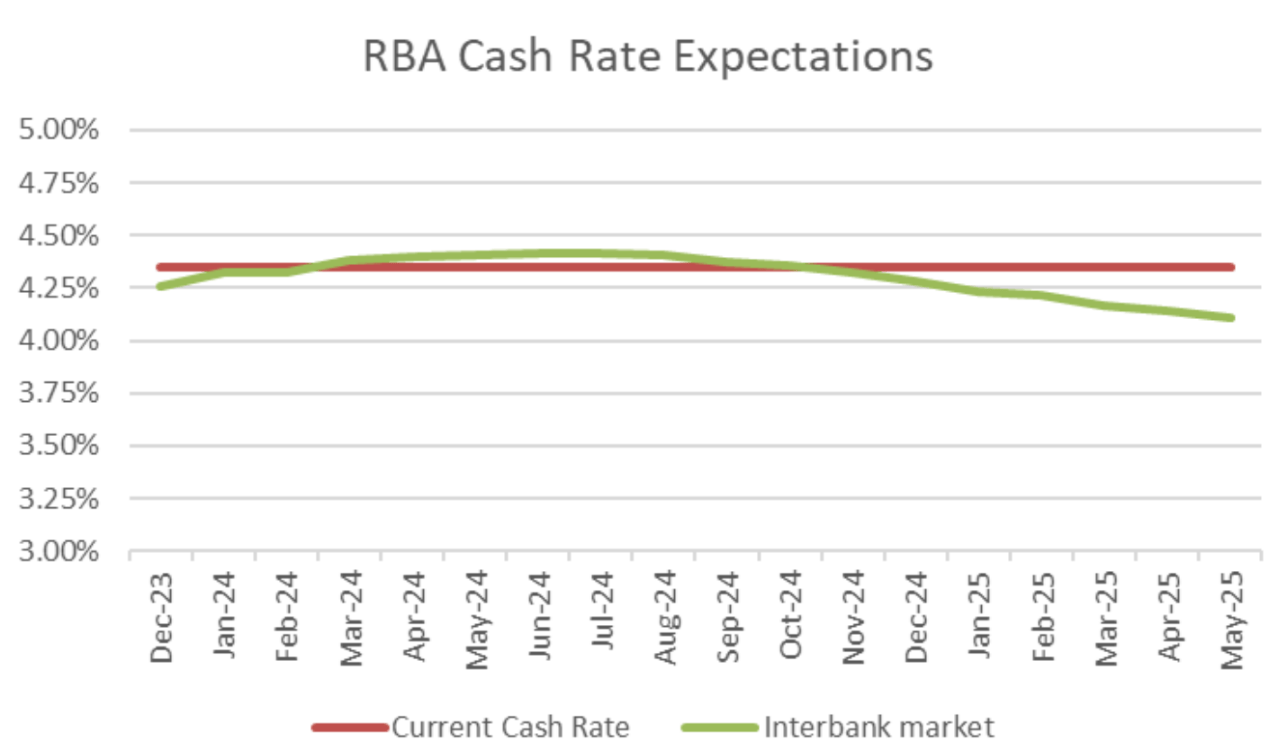

Here, I’ll turn to the other bankers at UBS who yesterday suggested that despite 13 rate increases and a 425bps increase in the cash rate, the Aussie economy’s resilience is both impressive, but also a bit of a double-edged sword.

In terms of the equity market UBS says we’ve now pretty much been priced in for the peak in the cash rate, which they say will likely top out around this 4.35% level.

Two more years

But that observation comes with the rider that, by about May next year, the market has just one rate cut priced in – “a genuine higher-for-longer environment” but a prediction which seems utterly dovish in comparison to what the guv’nah was saying last night.

Bullock expects – against this soft-supply environment – that herding the cats of inflation back to the RBA’s 2-3% target range was a circa two-year project.

“We expect it to take another two years … because much of the remaining task of bringing inflation back to target will require bringing aggregate demand and aggregate supply into closer alignment.”

Which suggests this model, recently released by the RBA, is now defunct:

The solution, she says, isn’t to lift supply, but to smash demand.

“That is what the board is aiming to do with monetary policy – to slow the growth of demand enough to bring inflation back to target while keeping employment growing.”

IG’s market analyst Tony Sycamore is, to put it mildly, sceptical.

“Next week’s retail sales and monthly inflation data will need to be red hot for the RBA to raise rates at the December RBA board meeting, although a rate rise in February is a risk.”

Twin Peaks

UBS reckon the problem is the “twin peaks” of record high migration and big spending Boomers. Not haircuts and dentists.

Migration to Australia is tracking at 600,000 a year right now, this would see Australia’s population surge by a never before seen 2.5% this year.

At the same time senior Australians have emerged as a spending force, with $29bn of superannuation benefits paid in Q3-2023, which is equal to an astounding 10% share of total household disposable income.

The jolt to the economy from these ‘twin peaks’ has (and should continue to) prevent a collapse in consumption, even as the middle demographic gets squeezed by cost of living and rates.

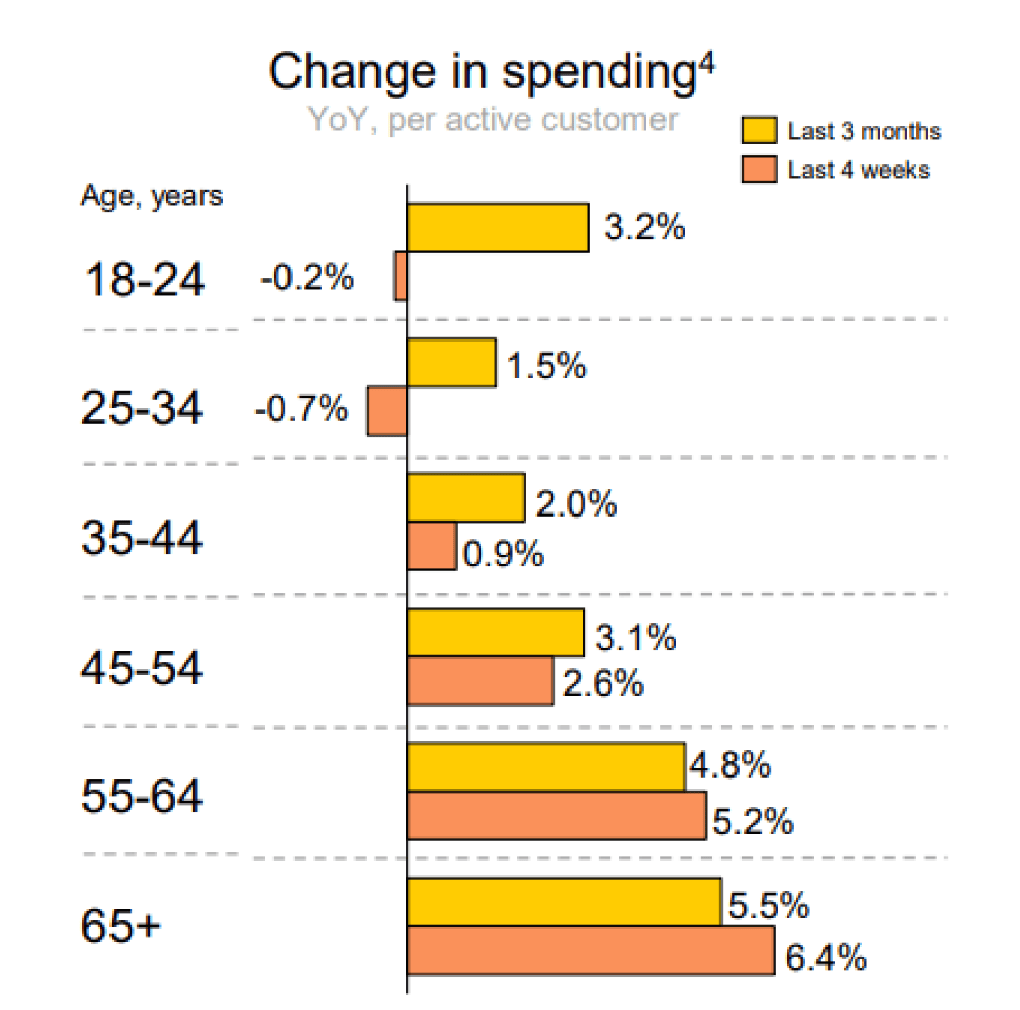

We would highlight this fact with data from CBA’s latest earnings report, which shows all them Aussies aged 55 and over are not only spending more in absolute terms than a year ago – but are actually accelerating their spending.

A the other end of the stick – youngsters under 34yrs are in outright retrenchment, and can’t apparently afford a Paddle Pop.

But check out how hard the youngsters spend is being cut off, according to CBA…

The RBA’s been hoisting the cash rate under previous guv’nah P Lowe since May last year. It’s just hiked the cash rate again by 25 basis points in November, after keeping rate steady for a full quarter.

A new beast

But Bullock says the inflation animal has changed from one created by surly supply chain issues to a simpler, scarier demand v supply beast – compounded by labour shortages.

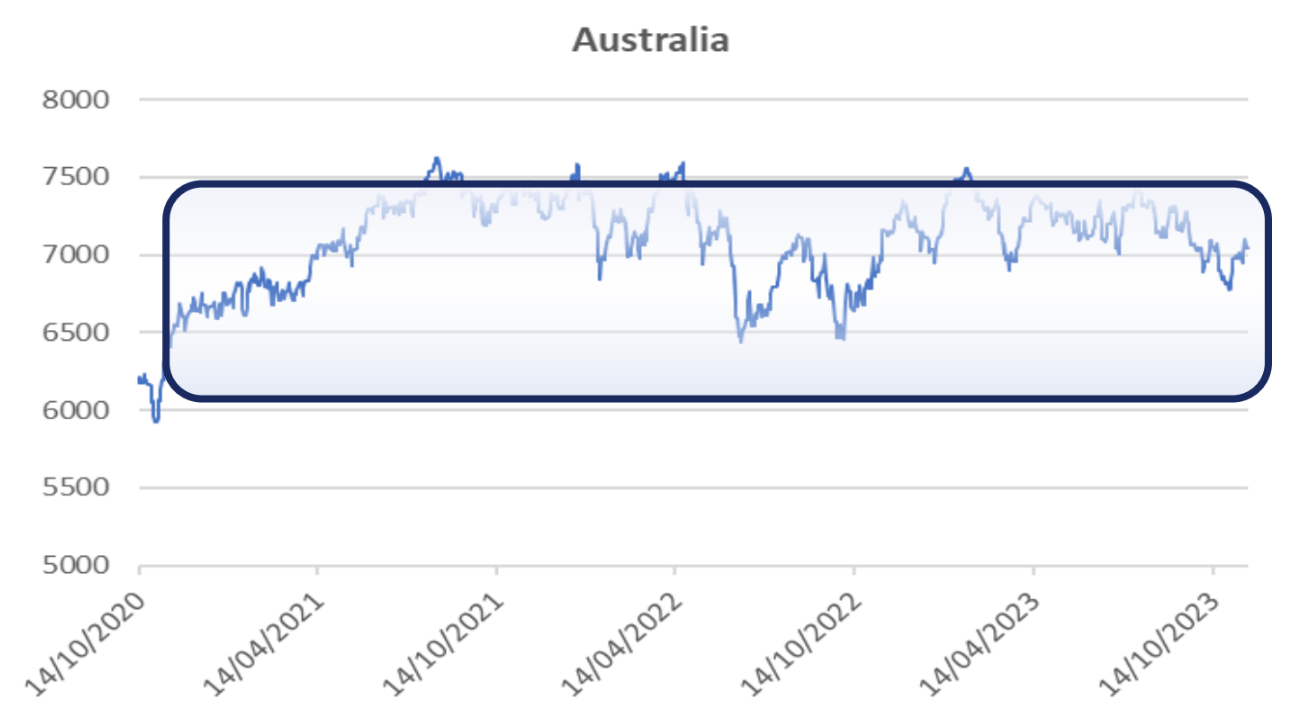

UBS says although the rate rise-led suppression of the economic and profits cycle is “smoothing” Australia’s economic landscape, “it is also creating a sideways and rangebound equity market.”

The ASX200 has been rangebound between ~6,400 and 7,600 for three years now (~ +/-10%).

The sticky local inflation compared to most other advanced economies has weighed on the $AUD over the last two years but UBS says this could now swing over to a strengthening bias.

“Historically, the most direct sector view for a rising AUD has been long Mining over Healthcare.”

Without any ‘imminent turning point’ in the economic cycle evident, the bank says playing EPS momentum trends is the handiest way to eke out some shorter term gains.

As we’ve highlighted, UBS likes construction related stocks as the best illustration of this dark matter momentum in the real Aussie economy, with upward revisions for messrs: Boral (ASX:BLD) , James Hardie (ASX:JHX), CSR (ASX:CSR), Worley (ASX:WOR),Seven Group Holdings (ASX:SVW) and Reece (ASX:REH).

For the good of the nation

I think we should always be scared when officials start pinning their ears back and say, however much they don’t want to do x, y and z – the truth is it will all be for the greater good of the country.

Bullock, after a few months, is firmly in this category of disassociated power brokers, on the basis of last night’s comments that it’s tough love, but that the country will take the medicine it’s given – knowing what the impact of the RBA’s decisions have on low income Aussies.

The boss says she gets letters all the time from citizens under the pump to make ends meet.

“Everyone is seeing prices for goods and services rise strongly… This emphasises the need to get inflation back down.”

She said she was also aware that interest rate rises are squeezing the finances of households with a mortgage.

“But while the board recognises there is a wide diversity of experience, the bank’s statutory objectives are economy-wide outcomes, and our key tool – the interest rate – is a blunt one.

“The board must therefore set its policy to serve the welfare of Australians collectively.”

Cool. Scary. Blunt.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.