JBWere’s Sally Auld: The policy of least regret means central bankers will not be taking their foot off our throats anytime soon

Via Getty

It might’ve been a quiet session overnight with the UK on holiday and a fair bit of attention on a funeral service in London (a pretty good time to be in funerals, actually). But behind the scenes investors were pricing in the US Federal Reserve’s turn on Thursday morning – our time – to roll the dice on a third straight 75 basis point rate increase and probably another of said scale when it gets back together again in November.

According to those calculations the market pricing for now in Fed funds futures suggests America’s terminal rate – that is, the moment where the FOMC slams the brakes on the rate hikes – will be 4.39% by April 2023.

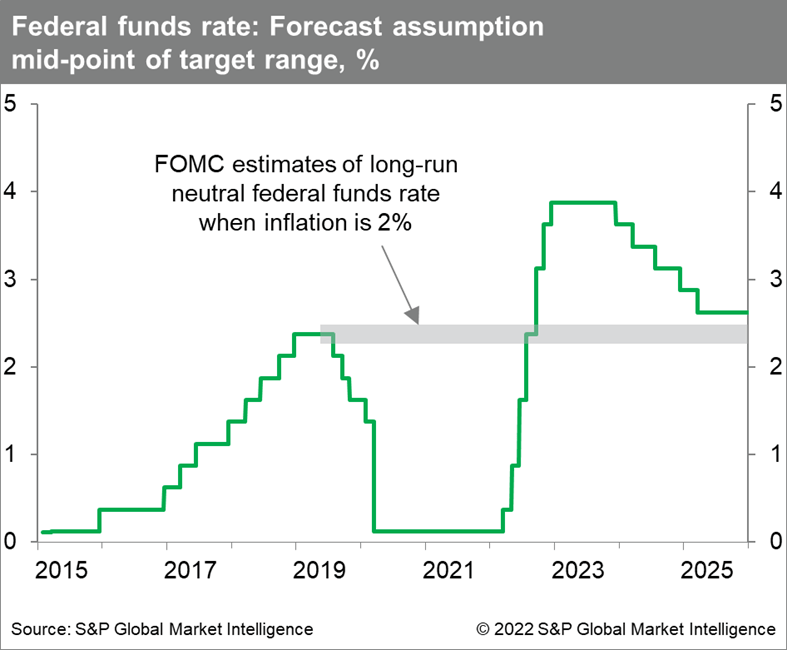

In a note this morning, S&P Global Market Intelligence is telling everyone that the FOMC is just about certain to announce another very large hike in interest rates on September 21st.

Ken Matheny, executive director, US Economics, S&P Global Market Intelligence anticipates the US Fed will raise the target for the federal funds rate by 75 basis points to a range of 3% to 3.25%.

He says the argument for a very large rate hike is based on the “still very worrisome” data on actual inflation.

Well, “worrisome” for some…

https://twitter.com/WatcherGuru/status/1571728713808486401

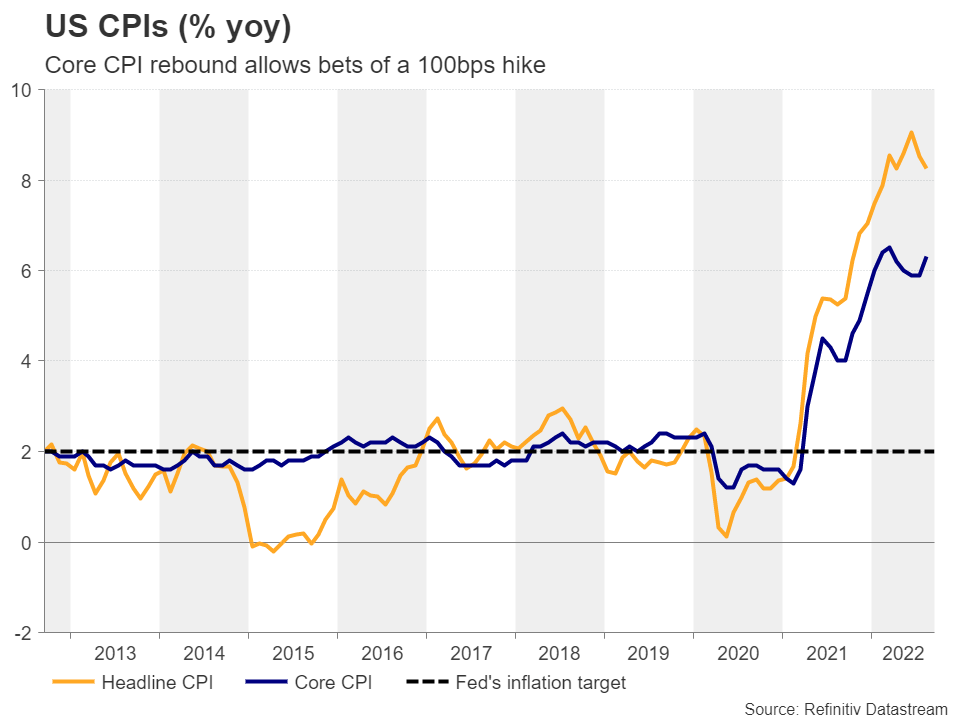

Stateside, headline inflation, including food and energy prices, is still 8.3% higher year on year, while core inflation — taking out the cost of food and gasoline etc — has still risen 6.3%, with the 0.6% monthly gain in August tearing a real hole in expectations.

Most observers now tend to agree that any hit to GDP growth and hints of moderation in the pace of employment gains will not deter the FOMC from pulling the trigger on a substantial rate hike.

“Until inflation is lowered much closer to 2% on a sustained basis, the Federal Reserve will act as if it’s almost single-mindedly focused on inflation. It sees slaying inflation as the defining challenge of this episode. It will tolerate, even expect, a period of economic softness and higher unemployment as the price to pay to bring inflation down,” Matheny said

Indeed, there’s some speculation The Fed is fixing to lift by an unprecedented 100 basis points this month in an attempt to signal – in the most forceful manner – its determination to see inflation brought down quickly.

“We would not rule out such a move, but with no signalling from policymakers that it might be considered, we see an increase of 75 basis points as more likely this week,” he added.

Adding to the sense of doom: bond yields continued to push higher overnight

And it’s never a good sign when bond yields go rogue. They certainly remained firm overnight with the rate-sensitive 2-years testing 4%. That is a scary repeat of 15-year highs. Meantime, the 10-years traded above 3.5% for the first time since 2011.

Pete McGuire from XM says the icing on the cake was last week’s hotter-than-expected CPI data, which disappointed those expecting inflationary pressures to ease in the months to come and allowed others to place bets over a full percentage point rate increase at this gathering.

“According to the Fed funds futures, market participants are now assigning a 20% chance for such an action, with the remaining 80% pointing to a 75bps increase. This may have increased the risk of disappointment and thereby the chances for a setback in the dollar, even in the still very hawkish case of a third 75bps hike.”

Auld news: Fed not getting wrong-footed again

JBWere’s Sally Auld told the NAB Morning Call poddy that markets have already priced in rate rises this week of 80bps in both the UK and US, meaning there’s some decent chance the hike will be more than 75.

“I suspect given the nervousness and hawkish rhetoric in the context of upside surprises for inflation is probably why front end bond yields are lifting,” Auld said.

“We’re not at the beginning of of the tightening cycle – some banks have raised 300 bps in a very short frame of time and to be contemplating that the Fed could still go as high as 100bp in this stage of the tightening cycle really underscores how central banks have been wrong-footed by the inflation trajectory but also how worried they are.

“The important distinction is what we are seeing in the inflation numbers is headline inflation starting to moderate a little bit as the decline in commodity prices comes through in official numbers but what’s not going to script is what’s going on in core inflation which continues to lift and this is the thing that will worry central banks because its the core which really reflects the persistence or otherwise of inflation.”

Auld says the fact that that series is yet to turn around underscores why banks are going to continue to be aggressive.

“All this tells us is that inflationary pressures are pretty dominant and this is why central banks are some way from taking their foot off the throat.”

Back to the hole

At Jackson Hole, Fed Chair J Powell was a little more explicit and a little more transparent, Auld added, with Powell et al reiterating the FOMC was “very mindful” of not making the mistake of easing too early.

At the annual economic symposium, Powell appeared top to toe in feathers, saying the bank will raise as high as needed and keep them there “for some time”.

While he acknowledged that this could hurt economic growth as well as labor market conditions, he added that these are the “unfortunate costs of reducing inflation,” and since then he’s even got Cleveland Fed President Loretta Mester saying interest rates should rise to slightly above 4%.

“That tells you they are more prepared to make the mistake of taking rates too high for too long and we don’t have to stretch too far to see where that mistake will take us,” Auld said.

Central banks often talk about “the policy of least regret” – if we’re going to make a mistake.. which one would we prefer to make?

“The choice for central banks in this case is pretty stark: we can take the economy into a recession or… not tighten enough and risk inflation expectations getting unanchored,” she added.

“And I think faced with that choice… the mistake they’d prefer to make is the recession.”

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.