It’s fake or break time for an unstimulated China

Via Getty

It’s an awfully critical week in the life of China and its gigantic/feeble economy, especially now the wrong card has turned up again in Taipei.

But no time to dwell, this week is all crucial data.

The Q4 GDP read, a check up on maudlin retail sales, and industrial production, the ballpark unemployment numbers, and then finally the house price index all drop under the shadow of a property crisis.

The property sector remains a significant risk, says XM CEO Peter McGuire, but there are signs that the market is stabilising.

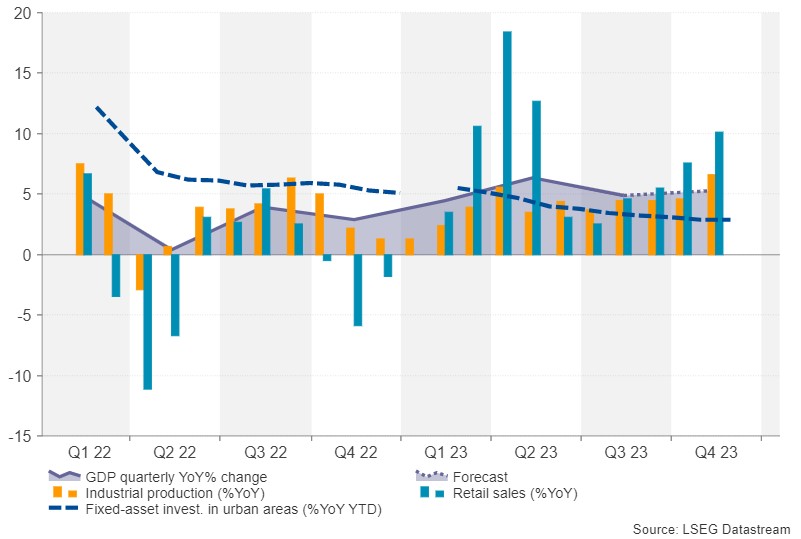

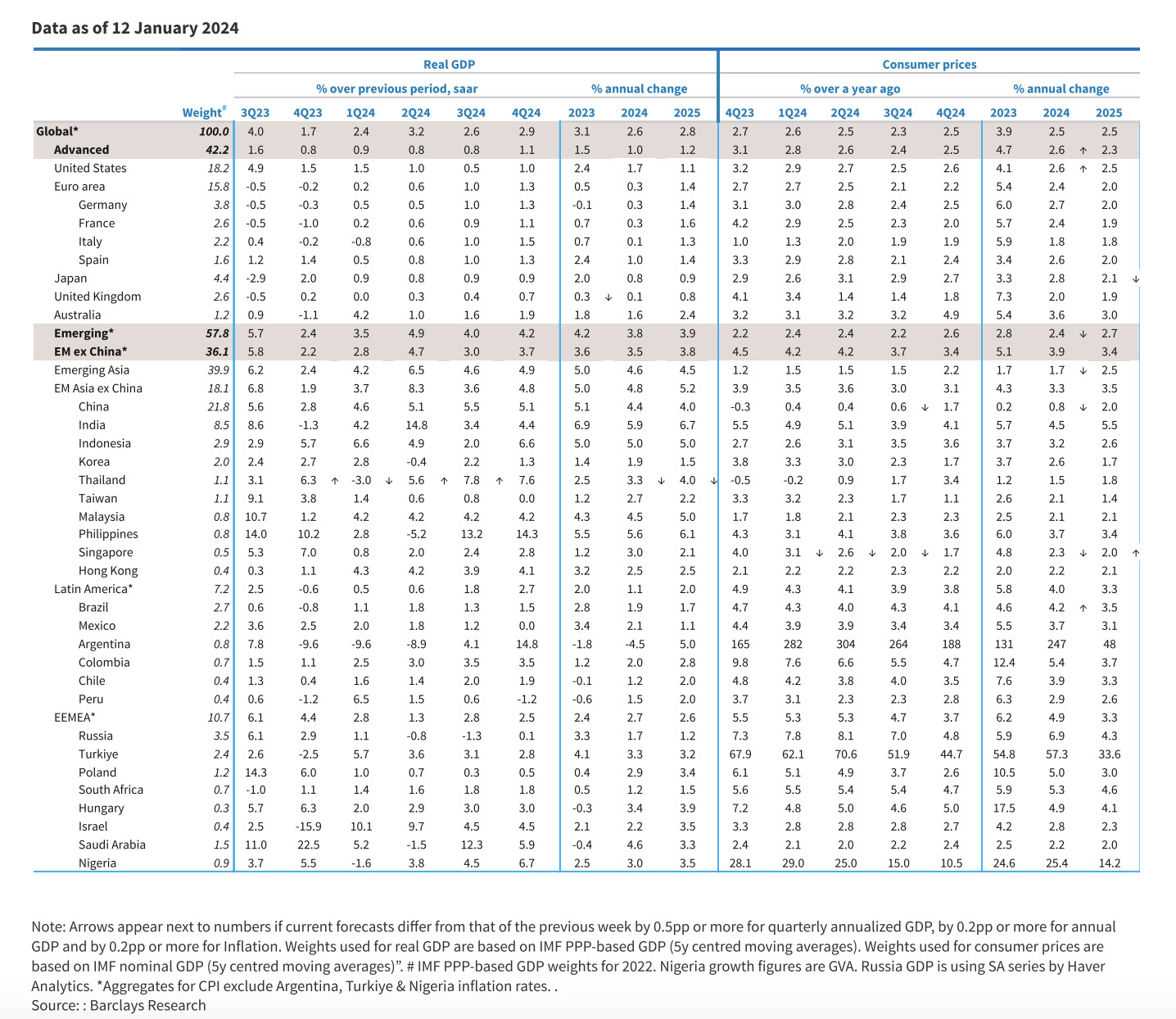

XM, CBA and Barclays all agree that GDP growth likely quickened in the final quarter of 2023 to 5.3% y/y after slowing to 4.9% y/y over Q3.

“Markets held their breath for a major stimulus announcement, but with one eye on deleveraging, authorities’ response only went as far as offering targeted drip-feed measures, leaving investors flabbergasted and disappointed,” McGuire told Stockhead on Sunday night.

“However, the government’s efforts may not have been totally in vain as Chinese consumers have been spending more since the summer and industrial production has also been rebounding.”

China drops Q4 GDP on Wednesday; Is it recovery time?

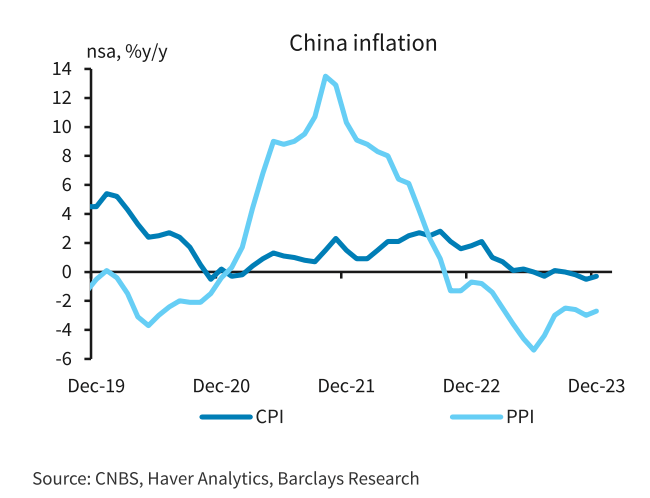

China’s figures for December showed that the world’s second-largest economy remained trapped in deflation for a third month running. China’s producer prices index (PPI) also extended falls for the 15th month in a row.

“On the bright side, the nation’s exports rose by more than expected, fuelling optimism that global manufacturing demand is finally picking up steam,” McGuire said.

A Q4 reading of slightly above 5.0% y/y would ensure that the government meets its growth target of around 5.0% for the full year.

The says XM Australia CEO says global equities, as well as the Australian dollar – broadly accepted as a decent liquid proxy for China risks – could gain on the back of stronger-than-expected growth in the world’s second largest economy.

The Chinese economy suffered several wobbles in 2023, as the property crisis went from bad to worse and this week, we’ll get a look at just how far the world’s No. 2 economy has come.

Chinese equities have been hammered

In Hong Kong, the Hang Seng index fell again, this time by almost 2% for the week, the second straight in ’24, as hopes for interest-rate cuts from the Fed in March waned following the hotter-than-expected inflation in the US.

It didn’t help that the nosy World Bank slashed its China GDP growth forecast for 2024 to 4.5%, the slowest expansion in over three decades outside of the pandemic years of 2020 to 2022.

Capping the fall were bets that the PBoC may ramp up liquidity injections and cut the key interest rate when it rolls over maturing medium-term policy loans this week.

It comes down to this – no one wishes ill upon China’s deflationary environment and faltering economic recovery, but a few genuinely bad data drops would surely leave Beijing with no cards to play other than get the PBoC to seriously slash their key lending rates and cut the reduce the RRR (reserve requirement ratio) again this year.

Unstimulated

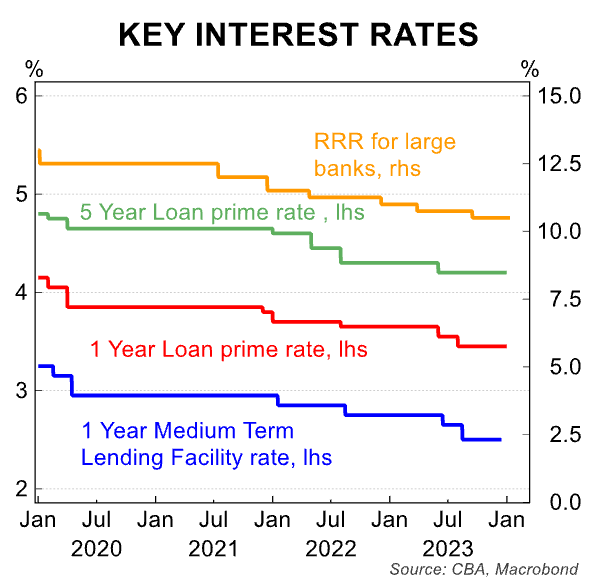

Certainly, following a report from China’s outstanding state news agency, Xinhua, investor expectations of a cut to the RRR fell into focus when Zou Lan, monetary policy department head of PBOC, highlighted the ratio as a monetary policy option to support credit growth.

Zou told Xinhua the PBoC will in fact use a variety of tools to provide “strong support” for a reasonable growth in credit, highlighting the Medium-term Lending Facility (MLF) and the banks’ RRR.

CBA forecast a 10bp cut to the key policy interest rates and a 25bp cut to the RRR (reserve requirement ratio) in Q4 2023, which didn’t materialise.

Instead, according to CBA economist Carol Kong, the PBoC opted to inject a bit of liquidity into the banking system via the one year MLF and open market operations in late 2023.

“We consider China’s economy is still in need of further monetary support,” Kong says.

Now the signals from the PBoC further suggest more easing is on its way as China’s uneven economic recovery leaves a trail of conflicting data drops – there was a decent lift in exports for December, but weak credit growth.

From the outside the feeling is that China’s persistent deflationary pressures are begging for more genuine stimulus measures.

This from Barclays Bank over the weekend:

“We think sustained CPI and PPI deflation highlight weakened domestic demand (consumption and housing drag).

“The visibly entrenched debt-deflation spiral, across-the-board pessimistic sentiment and PBoC officials’ hints suggest imminent monetary easing,” the bank’s economics team says.

They were wrong.

CBA now forecast the PBoC will cut the one-year MLF rate by 10bp in Q1 and Q2 2024 to 2.30%.

They were wrong again.

On cue, China’s central bank left the medium-term policy rate unchanged on Monday, defying those expectations for a cut on the back of a weaker RMB which limited the scope of monetary easing in the near-term to boost the economy.

“We also expect a25bp cut to the RRR in Q1 and Q3 2024. This expected scale of PBoC easing will be the same as 2023. The risks to our call are skewed to more aggressive easing.”

Where does the growth come from?

Kong says ahead of Wednesday’s drop that China’s economy looks to be on track to finish 2023 above the government’s GDP target of “around 5%”.

The consensus of China economists forecast a 5.2% lift in GDP for 2023.

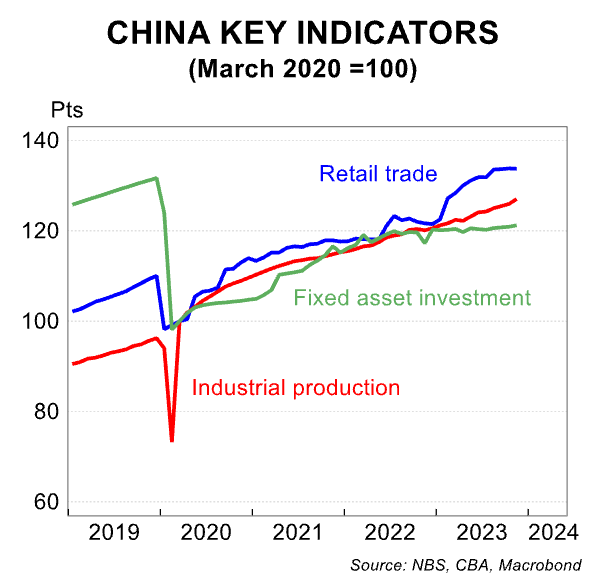

Kong says that at first glance, domestic consumption looked to be a stronger driver of 2023 growth (blue bars above).

But while the bulk of consumption growth welled up in H1 2023 – thanks to pent-up post-zero-COVID demand in December 2022 – Chinese consumer spend barely budged in H2 2023 (blue line above).

Fixed asset investment also performed poorly, flat-lining through 2023 (green line above).

Falling property investment was the main culprit, according to CBA.

“The government’s various support measures have failed to move the needle on the property sector.

“For example, medium to long term loans to households, a proxy for mortgages, remained weak despite lower mortgage interest rates and more favourable home-buying rules,” Kong says.

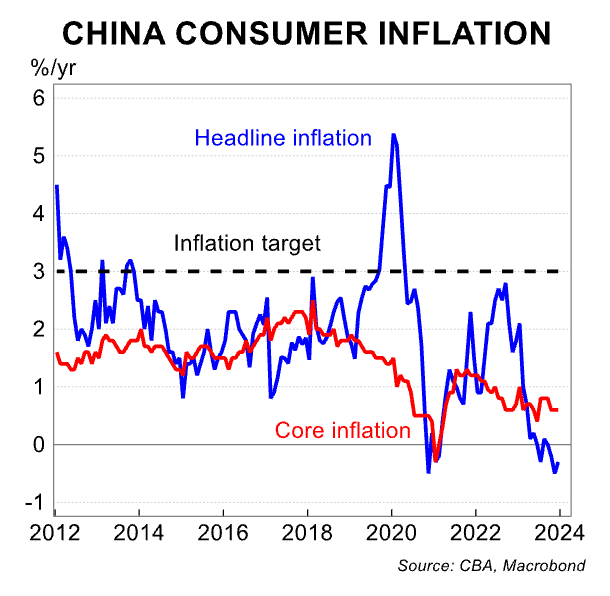

And the ongoing uncertain, even tepid domestic demand has kept Chinese consumer price inflation soft.

The Headline CPI printed at or below 0.0% for half of 2023, while Core CPI inflation remained well below the government’s 3%/yr target.

“The external sector fared better than we had expected. China’s export growth grew for the first time in seven months in November. Nevertheless, the improvement in exports largely reflected exporters slashing prices which may not persist for long,” Kong says.

Easing policy constraints

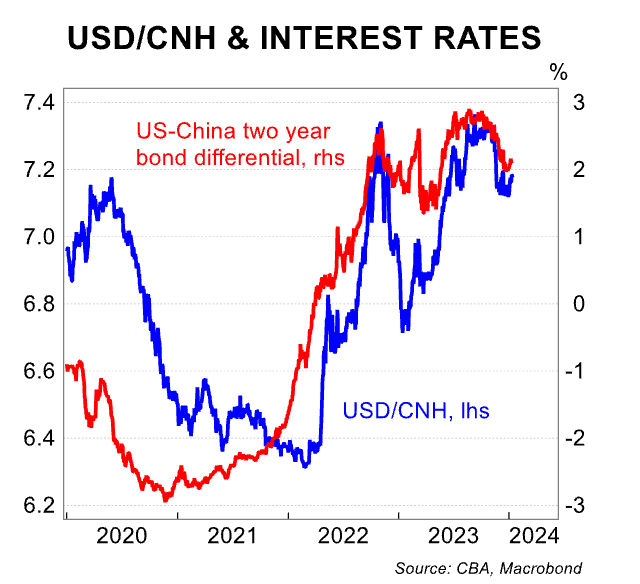

CBA has noted previously that China’s weak currency may have prevented the PBoC from undertaking a more aggressive easing cycle.

However, the yuan (CNH) has strengthened against the USD by about 2.5% since September 2023. Expectations for FOMC rate cuts have weighed on US interest rates and in turn on the USD/CNH.

Judging by the PBoC’s continued intervention at the daily CNY fix, the currency is likely still too weak for the government’s liking.

That said, CBA believes environment may become more favourable for the PBoC to ease monetary policy this year while the FOMC is expected to cut the Fed Funds rate.

In addition, China’s state-owned banks have again cut their deposit rates in late December 2023. Deposit rates were previously cut in June and September 2023.

That’s significant because lower deposit rates can reduce banks’ funding costs, giving them more leeway to cut lending rates to support spending.

CBA: it’s not enough

Weak domestic demand, as well as less pressure from the currency and banks’ funding costs, suggest further PBoC easing is likely in coming months.

“One could argue monetary policy may only have a limited impact on boosting demand,” according to Kong.

“Indeed, economic momentum remains weak despite the PBoC cutting the one year MLF rate and the RRR two times in 2023.

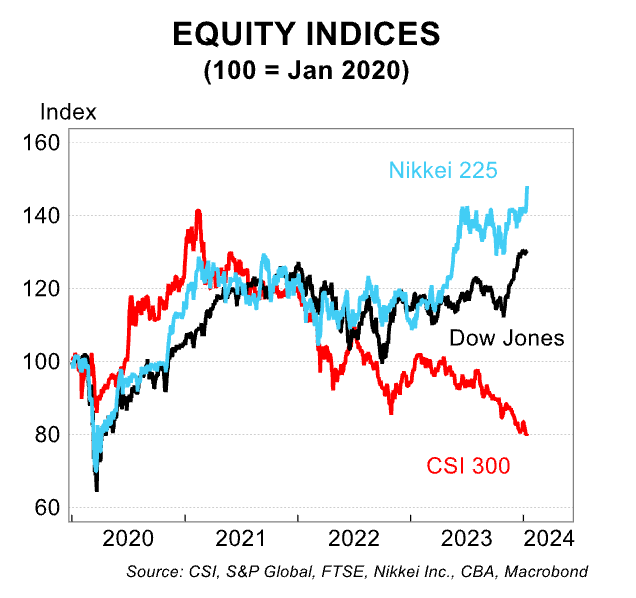

“China’s asset prices also performed poorly. For example, China’s benchmark CSI 300 index declined by more than 15% in 2023. In contrast, the Japanese and US equity markets posted very strong gains.”

But the clamour for additional policy support from the PBoC is getting louder and more China watchers now regard official intervention as necessary.

First up for CBA: the PBoC will likely want to prevent the real policy rate from rising given CPI deflation.

“Second, monetary easing can signal the government is committed to supporting the economy which may improve confidence at the margin,” Kong says. “Fiscal policy maybe more effective in monetary policy in restoring confidence in the economy.”

The question OFC, is whether Beijing is willing to go down this route.

“The central government’s refusal to introduce strong stimulus measures in 2023 showed it may be prioritising other objectives, such as national security and competition with the US, over economic growth.”

The annual National People’s Congress (NPC) meets in March where key economic targets will be announced.

That’s when Beijing will likely set the GDP growth target for 2024 – probs “around 5%” the same as last year and which was deemed conservative at the time.

Kong says such a target may be “a bit too ambitious” for the economy in ’24, given the poorly domestic demand and a higher base of comparison without further fiscal support.

“At this stage, we consider the risks to our 2024 GDP growth forecast of 4.9% as skewed to the downside.”

Putting China GDP in Context

And finally…

Last week state media were let run with shiny new report from an arm of the official Chinese Academy of Sciences (the shadowy-sounding Centre for Forecasting Science), declaring that China’s economy “will maintain steady growth this year with an estimated GDP growth rate of around 5.3%”.

So that’s where my 2 cents is.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.