Closing Bell: Day 5 in the ASX wilderness despite a jobs read bad enough to bury rising interest rates

Via Getty

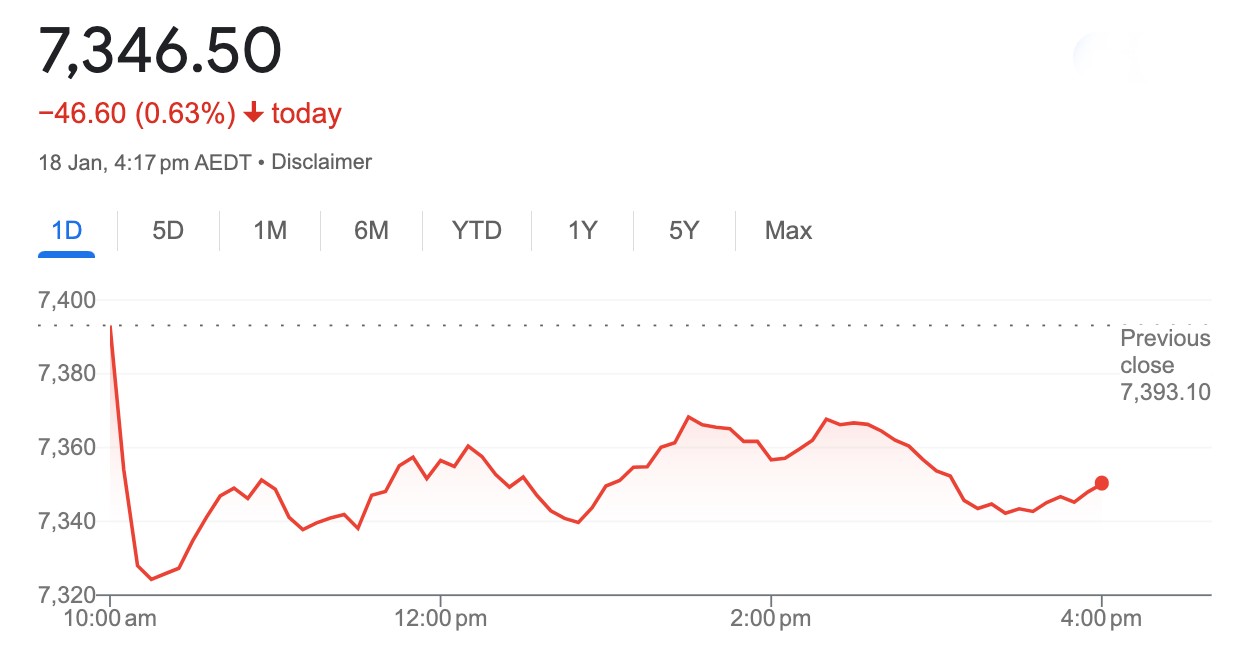

- ASX200 ends 0.63pc lower, a fifth consecutive decline

- Sector losses led by Real Estate

- Small cap winners led by Osmond Resources

It’s Day 5 of straight losses for the ASX benchmark. Wall Street fell, and so did we.

At 4.15pm on Thursday, the S&P/ASX200 closed down 47 points or 0.63% to 7,346.5:

To be fair, on Thursday the ASX200 inherited some shopping numbers out of both Britain and the US disconcerting enough to force yet another recalibration of the bets made on the imminent end of interest rate cycles. In the UK, consumer prices were toppy, while US retail sales were typically extravagent.

That sent shivers down the spine of local growth sectors with Property particularly hammered, down more than 2%.

Next in the dog house was a third strike for the Energy sector, which has lost ground again on tepid crude oil movements.

Strike Energy (ASX:STX) has lost more than 3%.

Viva Energy (ASX:VEA) and Santos (ASX:STO) fell about half that.

It was a mixed day for the big miners as the price of iron slipped again overnight towards $125 per tonne.

Tech stocks wobbled (Block down 1.1%) and fell (Novonix, 4.3%, Appen lost 3%).

EML Payments killed it after killing its disaster of an Irish subsidiary.

On the slightly positive side of the market, the major banks rose to the tune of likely RBA rate cuts, the National Australia Bank (ASX:NAB) out front with about 0.7%.

Australia’s seasonally adjusted unemployment rate was at 3.9% in December 2023, holding steady for the second straight month and remaining at its highest level since May 2022.

That said, the jobless rate totally plunged, while the participation eased off its November’s record high of 67.3%.

All the big 4 banks, Gregor, Robert Badman, my cat and our neighbours – as well as most economists – now reckon the RBA is done lifting interest rates and will look to lower the cash rate in the back half of 2024.

“Make no mistake, the labour market is cooling, and following a recent run of softer inflation data, RBA rate cuts are coming,” IG market analyst Tony Sycamore says.

“Q4 inflation data, scheduled for release on January 31st, will determine whether expectations of two 25bp RBA rate cuts become three in 2024. The more cuts, the merrier as far as the ASX200 is concerned.”

ASX SECTORS at 4pm on THURSDAY

Around the ‘hood…

Best to start in Shanghai, where the Composite has already lost about 1.3% and the Shenzhen Component 1%.

These losses are starting to accumulate.

Both the mainland benchmarks at lunchtime on Thursday are at or around their lowest ebb in almost four years.

The comatose Chinese economic recovery has drifted with tetonic inevitability all the way back to pre-COVID levels.

Despite the upbeat talk out of Davos, China’s economic outlook and the total absence of aggressive policy support measures out of Beijing remains one of about 20 problems weighing heavily on investor sentiment.

On Wednesday, data showed that China’s economy grew 5.2% year-on-year in the fourth quarter, missing forecasts for a 5.3% expansion, but it’s the official absence of concern which might be giving traders extra angst.

We’re watching gold…

Which is looking more settled at around US$2,010 an ounce on Thursday following a small pullback in the Greenback and USTreasury yields.

The safe haven is still down around a five week low as traders equivocate over stronger-than-expected US retail sales data vs the likelihood of more higher/longer thinking from the US Federal Reserve.

This week, Fed officials like the tough talking Fed Governor Christopher Waller pushed back hard against Wall Street’s aggressive bet placements on an easing monetary cycle.

In the States…

US markets struggled again overnight, all three majors in the red as investors weighed cautious statements from central bankers over the pace of any upcoming interest rate decreases as US economic data remains resilient.

The Dow fell 94 points to 37266, the S&P 500 and the Nasdaq lost 0.6%.

US Markets are now pricing in a 53.8% chance of a Fed rat cut in March, down from 63.1% in the previous session, according to CME’s FedWatch Tool.

Investors continue to eye developments in the Middle East following reports of fresh US strikes on Houthi targets in Yemen.

ASX SMALL CAP LEADERS

Today’s best performing small cap stocks:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % | Volume | Market Cap |

|---|---|---|---|---|---|

| MRD | Mount Ridley Mines | 0.002 | 100% | 8,487,888 | $7,784,883 |

| FTC | Fintech Chain Ltd | 0.009 | 50% | 7,769 | $3,904,618 |

| JAV | Javelin Minerals Ltd | 0.0015 | 50% | 9,676,290 | $1,633,729 |

| KEY | KEY Petroleum | 0.0015 | 50% | 3,563,007 | $2,262,928 |

| MCT | Metalicity Limited | 0.003 | 50% | 364,999 | $8,970,108 |

| PIM | Pinnacle Minerals | 0.17 | 42% | 2,150,661 | $4,159,574 |

| SPQ | Superior Resources | 0.015 | 25% | 3,976,081 | $24,014,645 |

| ESR | Estrella Res Ltd | 0.005 | 25% | 1,751,658 | $7,037,487 |

| NRX | Noronex Limited | 0.011 | 22% | 1,564,069 | $3,404,716 |

| ASN | Anson Resources Ltd | 0.12 | 21% | 4,346,714 | $127,288,178 |

| BFC | Beston Global Ltd | 0.012 | 20% | 814,725 | $19,970,469 |

| HOR | Horseshoe Metals Ltd | 0.006 | 20% | 216,670 | $3,232,393 |

| IEC | Intra Energy Corp | 0.003 | 20% | 9,179,921 | $4,151,954 |

| RIL | Redivium Limited | 0.006 | 20% | 2,295,429 | $13,654,274 |

| TML | Timah Resources Ltd | 0.031 | 19% | 5,715 | $2,307,754 |

| FIN | FIN Resources Ltd | 0.019 | 19% | 1,369,161 | $10,388,299 |

| MAN | Mandrake Res Ltd | 0.045 | 18% | 4,705,858 | $23,398,877 |

| KOB | Koba Resources | 0.099 | 18% | 370,234 | $8,855,000 |

| NIM | Nimy Resources | 0.1 | 18% | 390,739 | $11,850,440 |

| DVL | Dorsavi Ltd | 0.014 | 17% | 26,475 | $7,159,939 |

| LIS | Lisenergy Ltd | 0.1575 | 17% | 408,640 | $86,427,031 |

| MOM | Moab Minerals Ltd | 0.007 | 17% | 2,011,300 | $4,271,781 |

| PRX | Prodigy Gold NL | 0.007 | 17% | 12,561 | $10,506,647 |

| TMK | TMK Energy Limited | 0.007 | 17% | 12,813,133 | $36,735,476 |

| R3D | R3D Resources Ltd | 0.044 | 16% | 111,033 | $5,790,120 |

Osmond Resources (ASX:OSM) has joined the growing list of mining minnows to come screaming out of the woodwork with news about a uranium find, after the company undertook “a review of historical exploration results” for its South Australian Fowler project, which has identified “the potential for large-scale uranium (U3O8) mineralisation.

Osmond had, at the time of writing, piled on a 29% gain on the strength of that release which – just so we’re clear – basically says that the company has cracked open the spreadsheets from long-finished exploration, and now there’s “potential” for uranium in there somewhere.

Meanwhile, Helix Resources (ASX:HLX) is leading the ladder for the day so far, up around 50% despite having no fresh news to titillate investors with today – the last we heard from Helix was on 15 January, when the company announced that it has hit decent, very shallow copper mineralisation at its Bijoux prospect in the Cobar-Nyngan area of central NSW.

Melodiol Global Health (ASX:ME1) has also lurched round 50% today, again on no fresh info since the company dropped news of a 51% spike in revenue YoY, and that it had raised a handy $215,000 following a placement at $0.001285 per share.

And a bumpy day for Woomera Mining (ASX:WML) yesterday appears to have been re-routed into something of a happy ending, with the company up 50% as well.

Wednesday was not an ideal day for Woomera, after it got shoved into a trading pause, which then blossomed into a full-blown trading halt a couple of hours later – which wasn’t lifted until quite late in the day, once Woomera revealed that it did, in fact, have news.

The news was that Woomera had completed a 26-hole / 2813m RC drill program at its Ravensthorpe projects located in SE Western Australia, and spotted peggies from eight of those holes to boot.

And Sabre Resources (ASX:SBR) has swung into the uranium news business, with an announcement that the company has launched a new exploration program at the Dingo Uranium Project within the Company’s 1,100km2 Ngalia Basin tenement package in the Northern Territory.

Sabre says the new program is set to build on the discoveries it’s already made at the site, inclding high-grade sandstone hosted uranium targets boasting numbers up to 5,194ppm eU3O8.

ASX SMALL CAP LAGGARDS

Today’s worst performing small cap stocks:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % | Volume | Market Cap |

|---|---|---|---|---|---|

| AN1 | Anagenics Limited | 0.012 | -40% | 1,493,797 | $7,575,557 |

| APM | APM Human Services | 0.795 | -40% | 20,027,206 | $1,215,266,078 |

| NRZ | Neurizer Ltd | 0.008 | -36% | 19,366,637 | $17,224,321 |

| EDE | Eden Inv Ltd | 0.002 | -33% | 46,665,247 | $11,034,813 |

| GES | Genesis Resources | 0.004 | -33% | 1,211,147 | $4,697,048 |

| LNU | Linius Tech Limited | 0.002 | -33% | 1,250,000 | $14,817,722 |

| YPB | YPB Group Ltd | 0.002 | -33% | 9,958,773 | $2,371,384 |

| DCX | Discovex Res Ltd | 0.0015 | -25% | 1,127,503 | $6,605,136 |

| MHK | Metalhawk. | 0.09 | -25% | 929,111 | $11,929,734 |

| PIM | Pinnacleminerals | 0.155 | -23% | 2,983,388 | $6,932,623 |

| C7A | Clara Resources | 0.012 | -20% | 256,585 | $2,835,586 |

| 1MC | Morella Corporation | 0.004 | -20% | 2,457,447 | $30,893,997 |

| 88E | 88 Energy Ltd | 0.004 | -20% | 114,970,845 | $123,627,103 |

| PNX | PNX Metals Limited | 0.004 | -20% | 3,190,000 | $26,903,124 |

| FTZ | Fertoz Ltd | 0.044 | -20% | 331,040 | $14,180,915 |

| IND | Industrialminerals | 0.425 | -19% | 898,561 | $36,099,000 |

| OD6 | Od6Metalsltd | 0.1 | -17% | 106,846 | $6,601,860 |

| MTB | Mount Burgess Mining | 0.0025 | -17% | 11,300,000 | $3,134,440 |

| TMR | Tempus Resources Ltd | 0.005 | -17% | 1 | $4,141,740 |

| TMX | Terrain Minerals | 0.005 | -17% | 200,000 | $8,120,567 |

| NMR | Native Mineral Res | 0.016 | -16% | 84,486 | $3,985,260 |

| KAU | Kaiser Reef | 0.1275 | -15% | 135,456 | $25,656,584 |

| TTT | Titomic Limited | 0.041 | -15% | 4,077,107 | $43,811,602 |

| SLB | Stelarmetalslimited | 0.18 | -14% | 121,362 | $11,005,664 |

| ASR | Asra Minerals Ltd | 0.006 | -14% | 1,115,631 | $11,455,470 |

TRADING HALTS

FBR (ASX:FBR) – pending an announcement in relation to the results of a proposed capital raising.

Toro Energy (ASX:TOE) – pending the release of an announcement regarding a proposed capital raising.

Mayur Resources (ASX:MRL) – pending an announcement in relation to a funding and development partner, and the securing of development funding for Mayur’s Orokolo Bay Industrial Sands Project.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.