CHRIS OF DEATH: Is Kogan just a Bogan stock (and if so, where is its bottom?)

Pic: d3sign / Moment via Getty Images

Every now and then, Stockhead’s enfant terrible dep ed Christian Edwards gets all het up about a stock’s poor performance. After getting tired of his sleeve-tugging – and making him promise to consult a proper expert – we allow him to plant his Chris of Death on the unlucky target. And ooh, does it leaves a mark…

Just when you think shares in spirited Aussie online retailer Kogan (ASX:KGN) can’t possibly tank anymore, they find a little more in the tank and just keep on tanking.

Down 3.5% on a touch Wednesday, 30% in a month and 60% year-to-date. If you’d given someone you love KGN stock for Christmas, then you’re probably a bastard.

Back in August, Kogan shares changed hands for a mighty $13 a pop, on Wednesday they’re trading at around $3.50 – of course, back in October of COVID-2020 shares in KGN were practically leaping out the door for $24.75.

And with the supply-and-demand challenges adding to the compound annual groan rate of tech stock pressure on valuations from rising interest rates, well, if there is a bottom to this, its vast radius is taking some time to traverse.

Luckily, we have time.

Where to begin?

Let’s go by the numbers to kick off.

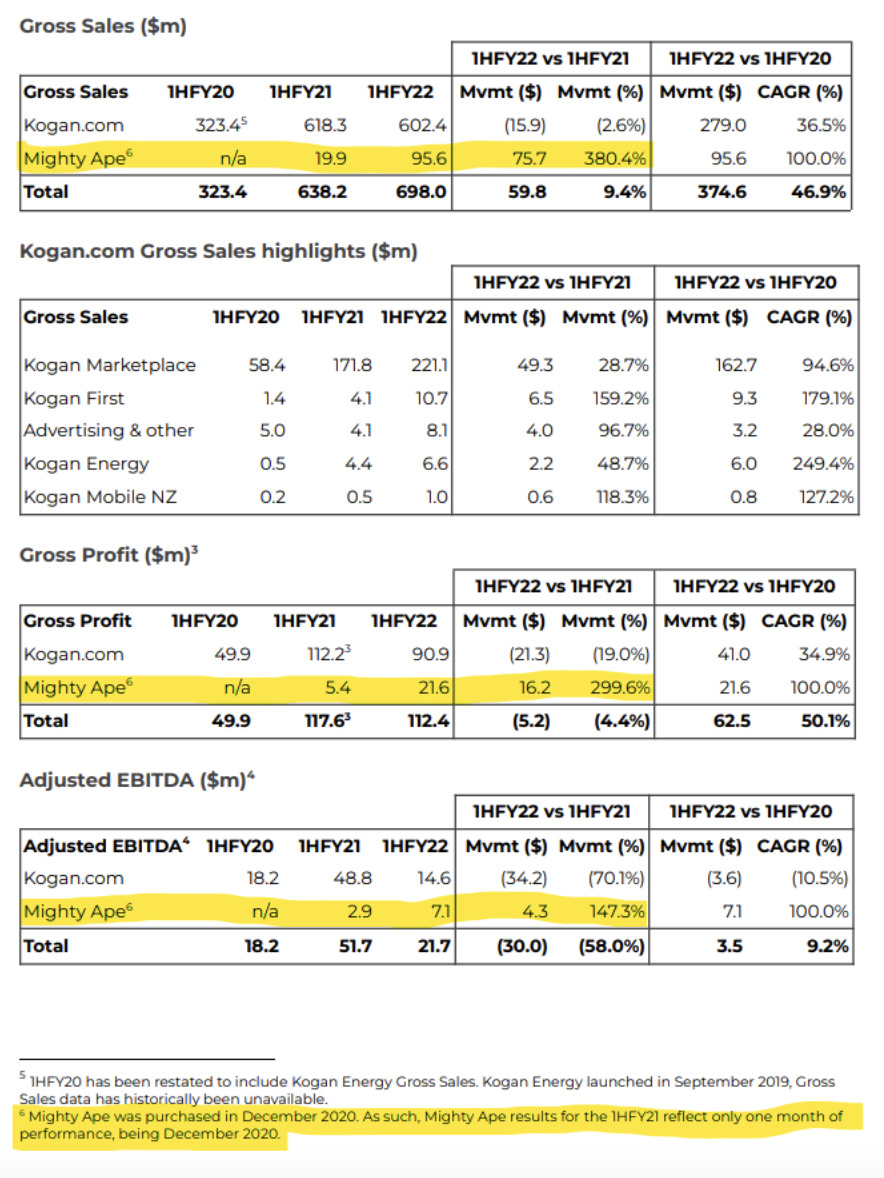

In its first half, to December 31, both gross sales and Kogan’s number of active customers jumped by 9.4% to $698 million and well over more than four million, respectively. Omicron was abroad, we was still buying stuff with gay abandon and then Zooming our peeps about it.

In total gross profit terms, the company reported a total 4.4% decline to AU$112 million, after Kogan.com recorded gross profit sliding 19% to AU$91 million during the period. This was offset, however, by a 300% uplift to AU$21.6 million in gross profit by Kogan’s UnZed retailer, Mighty Ape.

“Gross profit was impacted by continuing supply chain interruptions as a result of the current COVID situation and associated fluctuations in demand,” the company said.

Adjusted EBITDA also came in 58% lower year-on-year for the half at AU$21.7 million.

KGN is not enjoying 2022

But the March quarter was a dismal three months, sales reversed, the business swung to a loss as demand evaporated and unsold inventory, clogged warehouses and backed-up already front-loaded supply chains.

In a sobering late-April third quarter update, Kogan said gross sales fell 3.8% in the first three months of 2022, stalling at just above $262 million.

Weak sales, higher inventory and operating costs delivered a humiliating $800,000 loss for the quarter, a 110% fall on the same quarter in 2021.

The rot first appeared in February when KGN banged into a trading halt and then fessed up to its December period $12 million loss – a period featuring such online retail hits as Christmas, Singles Day, Black Friday and s..t-tonne of Covid-19. That’s the annual online spendfest and one which KGN had never before been in the red since listing on the ASX in mid-2016.

Kogan’s March forecast of achieving a compound annual growth rate (CAGR) of at least 20% is looking a little disingenuous.

OK perhaps for JB Hi-Fi, which year to date is up 6.56%, Harvey Norman shares are also up year to date, while Myer has also seen strong online growth to be up 5.4% over the same period.

So what’s a good price for KGN?

Earlier this month frazzled-sounding Credit Suisse brokers told investors they were downgrading Kogan’s shares to “Underperform”, perhaps only because analysts can’t assign a ‘Put It Out Of Its Misery rating’.

At the same time Credit Suisse lopped a full third off its KGN forecast, whittling it down from $5.53 per Ruslan to just $3.75, saying sales fell “well short of forecasts and market averages, gross sales falling -7.2% year-on-year and Third-Party and Exclusive Brands falling -21.8% and -18.8% respectively.”

The broker says gross profit will struggle in the short-term due to high direct sourcing costs and cautions the company’s cost/profit problem could become a cash problem. Costs eased QoQ, but remained 16% above 2021, the broker added, while margins (EBITDA) also tumbled.

Credit Suisse: KGN target price is $3.75; Current Price is $3.50

On the same day – 2nd of April – UBS brokers also put out a note, but holding the KGN rating at Neutral.

Following the “significant downturn” from January, third quarter gross sales came in -13% below the UBS forecast due to “general weakness in e-commerce and a more cautious consumer over February and March.”

The broker says gross margins will be impacted by KGN’s elevated inventory levels (again), and “more material operating leverage is now not expected until at least 2H23.”

But, while Kogan’s forward earnings multiple remains elevated, UBS retains the Neutral rating.

UBS: Target price is $4.30; Current Price is $3.50

The pandemic poster child for the challenges of supply chain management

Considering the inventory bloat, coupled with slow sales, the question is, how long can Kogan go? Has we got a handle on the warehouse bloat that led to its 2021 profits falling by close to 87 per cent? Company shares are now down a massive 60.6 per cent for the year-to-date.

It was a marked turnaround from January trading which was up 12% yoy – again now sitting on elevated inventory levels – Kogan is a poster child for highlighting the challenges of supply chain management in the face of extended lead times on new stock and volatile consumer demand. You can expect higher warehousing costs in the near term too, which’ll be pushing out more material operating leverage.

We put the Koganundrum to Merewether’s Luke Winchester

Luke says that during the Covid boom, the market was willing to overlook a number of red flags that has always existed with Kogan but with the Covid sugar hit now waning those issues are rearing their head.

“First up, Kogan has always cherry-picked its reporting metrics and focuses very heavily on adjusted numbers rather than audited financials,” Winchester told Stockhead.

As an example, Luke cites the January 2021 update, where Kogan claimed 380% growth in their Mighty Ape acquisition, but in the notes clarified that they were only comparing one month of results in the prior period:

Busted.

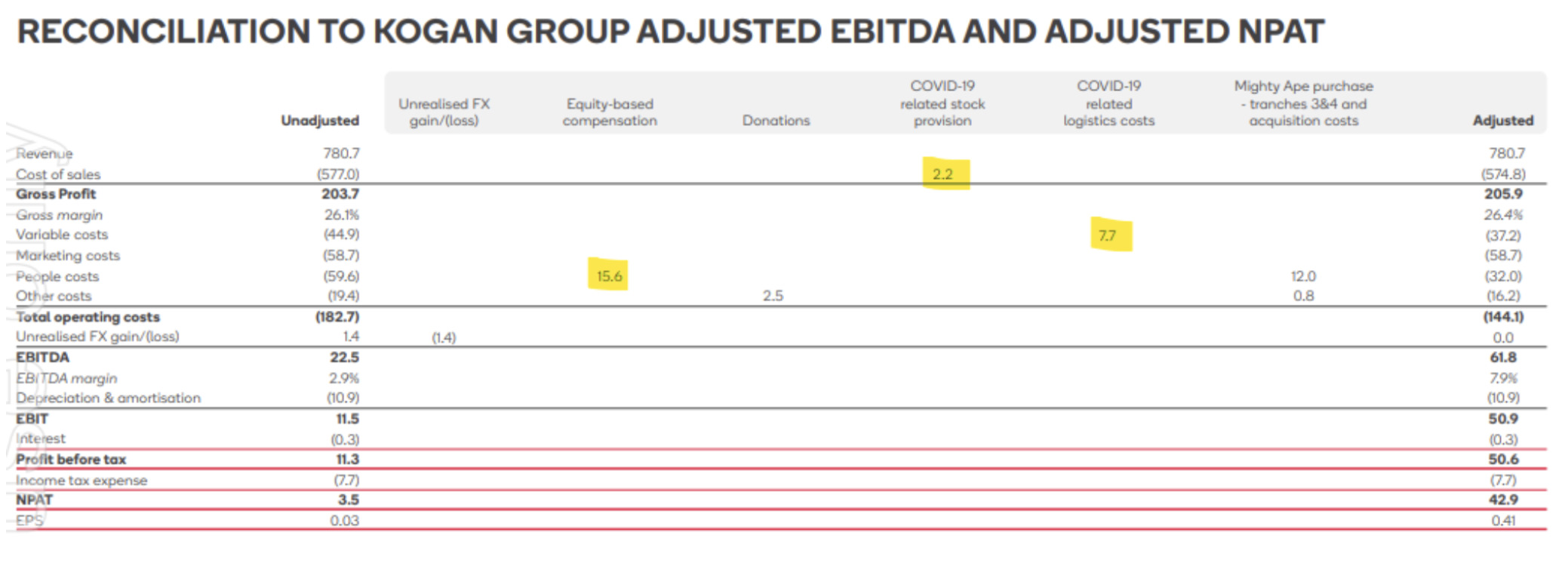

And Luke adds, while most of Kogan’s adjustments are similar to other businesses, they have been known to include costs that are costs of running a business:

From their FY21 results, Kogan excluded the costs of $7.7m required to purchase additional warehousing space required because they overstocked. Despite management trying to claim it was a one-off, inventory issues continue to plague the company and are a cost of doing business for a retailer, particularly during a time like Covid.

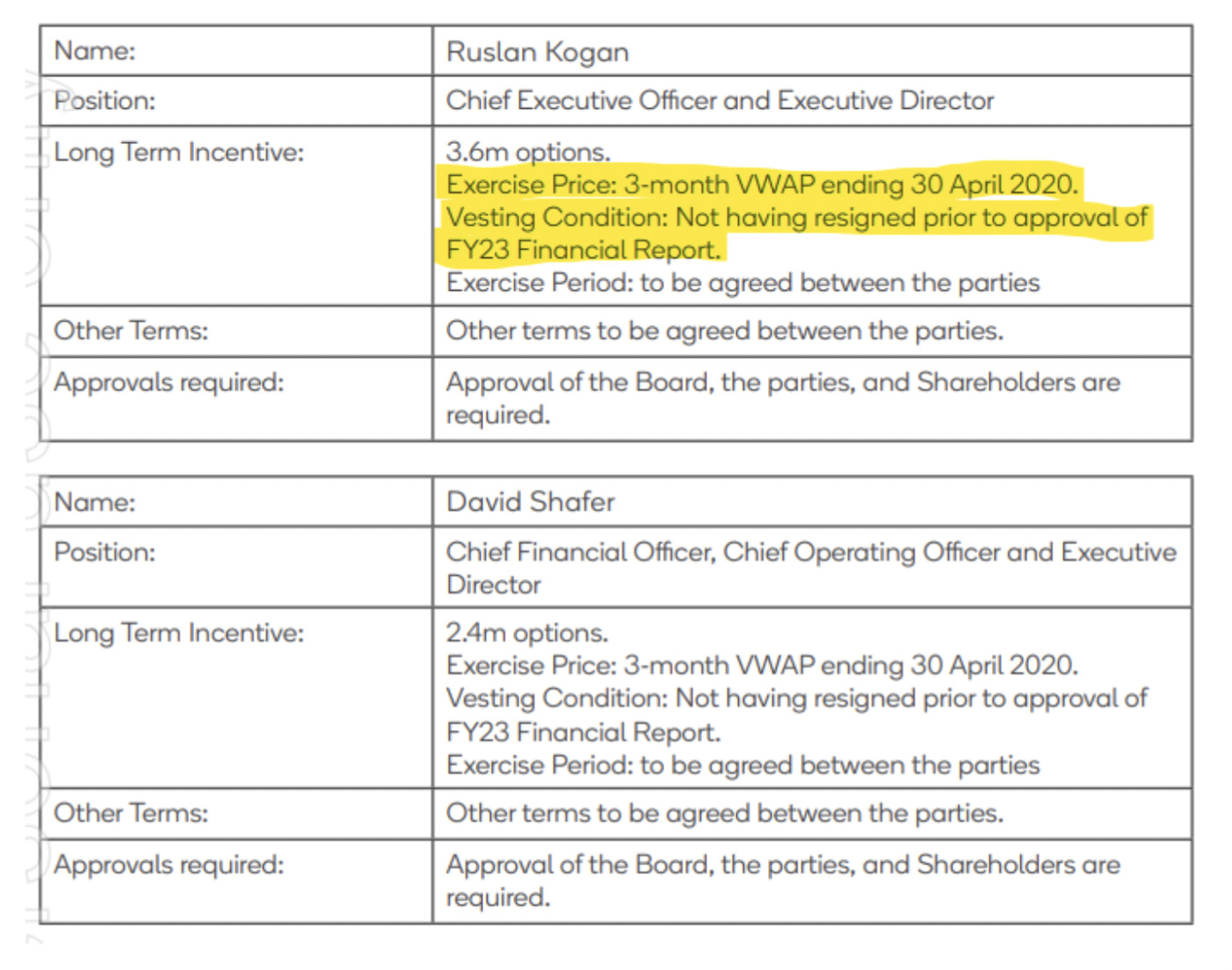

“The market also took umbrage with the fact that Ruslan Kogan and David Shafer (COO) were awarded 6m in options in May 2020 with the only hurdle being they didn’t resign before the company’s FY23 result,” Winchester said (before a longer discussion over how best to present the detail below. As you can see we went for yellow texta and screenshot-from-printout of ASX announcement).

What really pissed off the market (and proxy advisors who pressured the Board not to proceed at the AGM where it required approval) was the strike price was based off the average share price in the three months leading up to the announcement rather than at the time of vesting.

“Throwing fuel on the fire was Ruslan and David sold 7.3m shares in August, pocketing millions knowing they would be able to repurchase those shares in a few years time (although perhaps karma playing a role, with the share price currently below the exercise price!),” Winchester said.

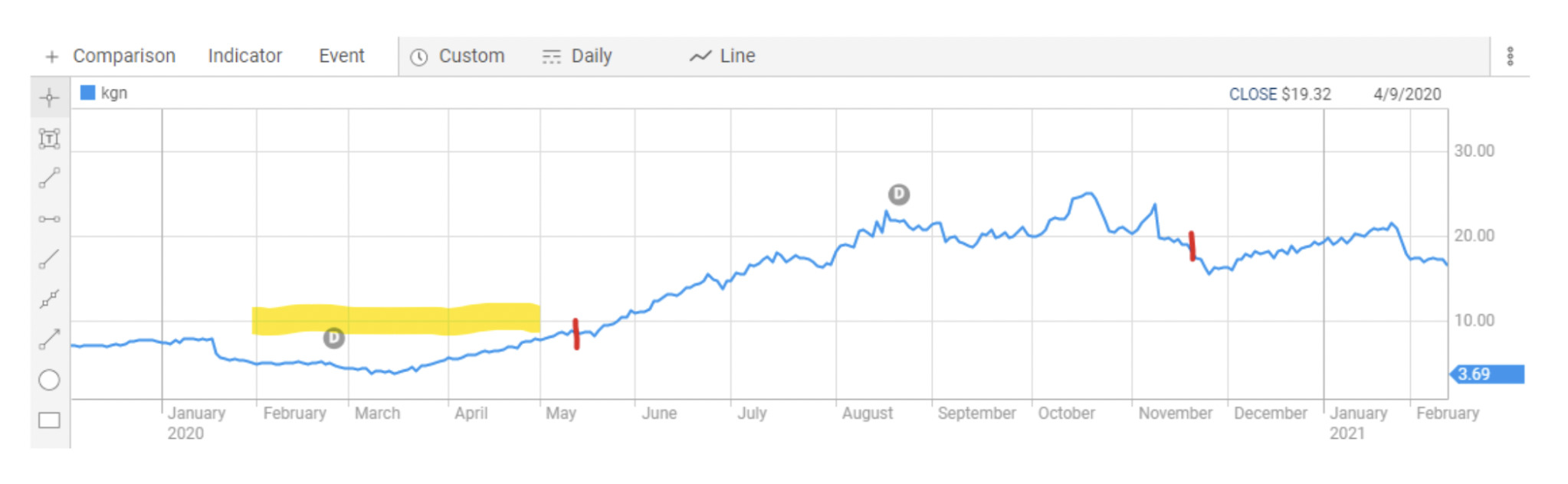

Again, Merewether Capital and Stockhead have joined forces to give you yellow texta (below) to highlight the period to help calculate the options price.

“So, 12 May was when that was announced – so options were already well in the money, thank you – and by the time they were approved 20 November, Ruslan and David were sitting well on a nine-figure fortune between them, that doesn’t always delight the Mums and Dads.”

Finally, it’s also likely that suffering Kogan shareholders are starting to wonder whether the business is spreading itself too thin. Luke cut this and sent it to us from their strategy update from last year’s AGM:

“When you have an underperforming core retail segment, should management really be focused on 12 other segments?”

“I know they often just partner with other providers using their brand, but nonetheless it isn’t a good look,” Luke says.

And when a genius like Kogan runs a business called Kogan, well, we’d expect less Kogan and more revenue.

The views, information, or opinions expressed in the interviews in this article are solely those of the interviewees and do not represent the views of Stockhead. Stockhead does not provide, endorse or otherwise assume responsibility for any financial product advice contained in this article.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.