Brokers on Monday: Clinuvel finds friends; ANZ’s unimpressive outlook

Breaking the ASX. Via Getty

We check in with some of the week’s notable broker moves. This week we focus on Clinuvel Pharmaceuticals and the ANZ Bank…

Clinuvel Pharmaceuticals (ASX:CUV): Brokers begin to sit up

Consensus recommendation – Hold

Consensus Price Target – $21.33

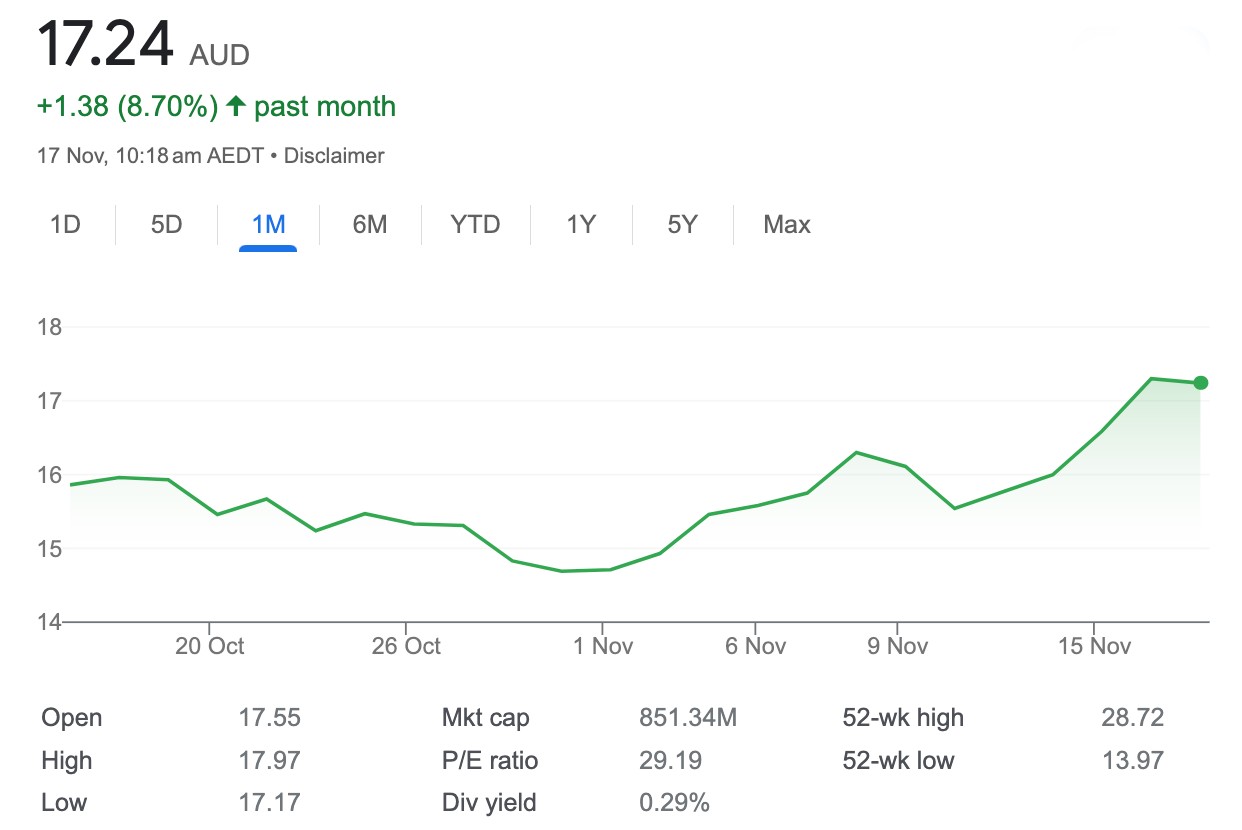

Current share price – $17.24, upside of circa 26% (ex-div)

Both Morningstar and Ord Minnett initiated coverage of CUV

CUV is a ‘global specialty pharmaceutical group focused on developing and commercialising treatments for patients with genetic, metabolic, systemic, and life-threatening, acute disorders, as well as healthcare solutions for the general population.’

Morningstar starts by clocking Clinuvel with a fair value estimate of $18.00 – and says the stock currently looks undervalued, trading at an 11% discount.

“We suspect the market is likely too pessimistic on the speed and extent of Clinuvel’s commercial rollout of Scenesse for its existing indication which contributes 83% to our fair value estimate.”

The company’s key product, Scenesse, is the only approved treatment for phototoxic reactions specifically associated with erythropoietic protoporphyria (EPP), a rare genetic disease, the broker says.

Morningstar’s forecast an Earnings Per Share (EPS) Compound annual growth rate (CAGR) of 16% for the next five years when Scenesse will remain fairly protected from competition.

The broker suspects the market is ‘also underestimating potential new earnings streams’ – broader indications including vitiligo might still be in clinical trials, M’star says ‘early efficacy and safety data is positive’ and would OFC greatly expand Clinuvel’s addressable market if successful.

Regardless, due to low capital requirements and high-profit margins, Clinuvel enjoys high returns on invested capital.

The Morningstar Uncertainty Rating for Clinuvel is High, and it assigns a Standard Capital Allocation Rating.

Over at Ord Minnett the initial coverage rating for CUV is Hold.

Ord Minnett has also initiated coverage of Clinuvel Pharmaceuticals with an $18 fair value estimate, as well as a Hold rating.

The broker is also relatively upbeat for CUV saying the market is on the whole, overly pessimistic about the biotech’s outlook.

Clinuvel’s current strategy revolves around expanding its direct distribution and increasing reimbursement support for Scenesse and exploring various ways to diversify its earnings beyond the niche adult EPP market.

According to FNArena, CUV’s current forecasts are for a five-year group CAGR of 13% compared with 19% revenue growth in FY23.

CUV: Past month

CUV: Year-to-date

Australia and New Zealand Banking Group (ASX:ANZ): Outlook – not that bankable

Consensus recommendation – Hold

Consensus Price Target – $26.02

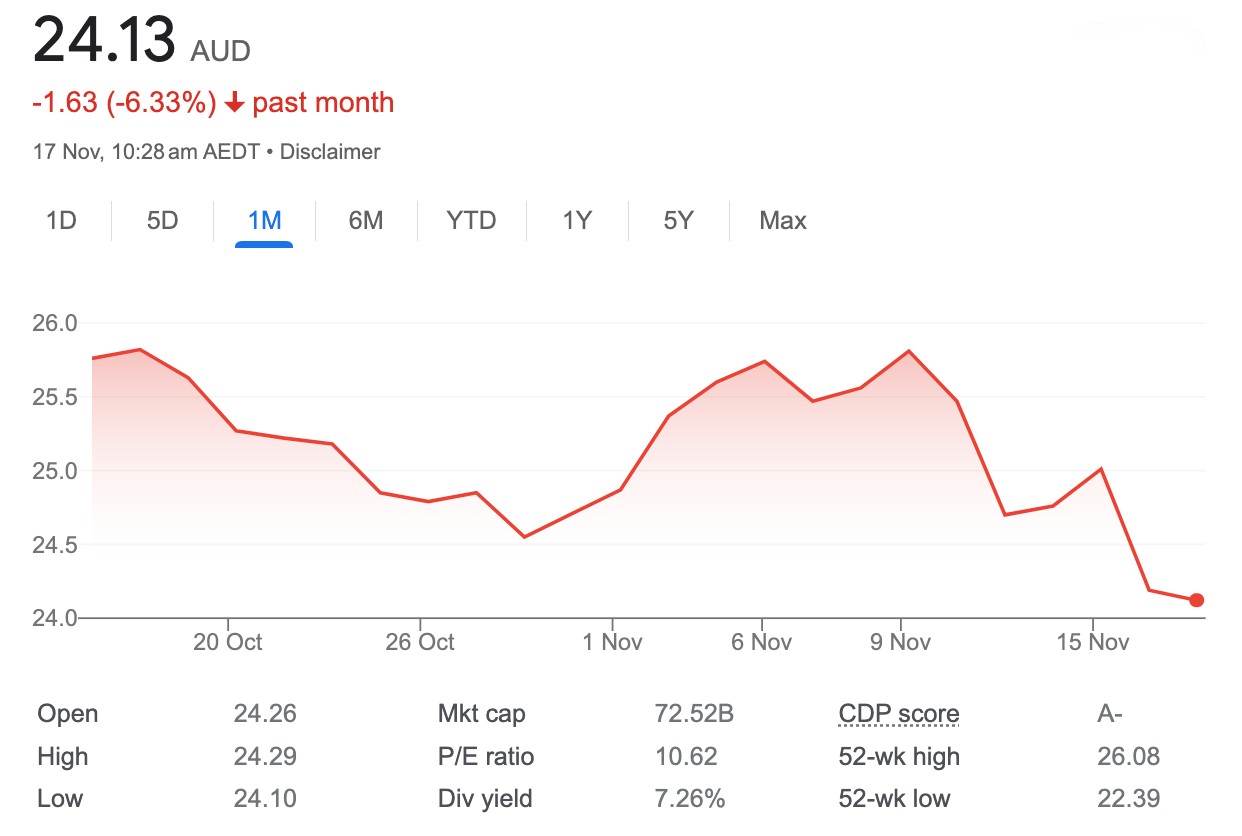

Current Share Price $24.13 (-3.2%, ex-div)

UBS Downgrades ANZ to Sell ($25 Price Target from $26).

Both JPMorgan and Citi lower PT ($25.40 from $26.50) and ($26 from $27) respectively. Both brokers Downgrade ANZ to Neutral

After dropping FY23 numbers this week, the feeling is that overall, it was a softer result than the headline implied, with beats in other operating income and asset quality, which are unlikely to be capitalised by investors.

ANZ Bank has delivered a slight miss to UBS’s expectations with its full year results, but the broker attributes the result to the cost of the bank growing above market during a period of heightened competition and some irrational mortgage pricing.

Cash net profits declined -6% year-on-year to $3.6bn, with net interest income down -5% to $8,078m, but some net interest income pressure offset by stronger than expected non-net interest income.

Citi analysts believe ANZ’s cash earnings are a significant miss on forecasts around -4% and -2% respectively.

The bank’s weighting to institutional business, formerly a boon, came home to roost as institutional offshore deposits fell, leaving the bank to fall back on more expensive domestic retail TD deposits to support their above-system mortgage growth, which hit retail profits, says the broker.

Going back six months, ANZ’s deposit franchise was a strong point of positive differentiation vs peers, courtesy of their weighting and execution in Institutional Banking.

However, over the second half, the momentum in the diversification story slowed as offshore deposits in institutional declined sharply. This led to ANZ’s aggressive mortgage market share push needing to be funded by expensive domestic retail Term Deposits, hitting retail banking profitability.

ANZ’s second half Cash NPAT of ~$3.6bn was a slight miss versus consensus expectations.

Net Interest Income fell 5% half-on-half, whilst Net Interest Margins contracted 10bps to 1.65% – in the core banking division, the underlying contraction was 7bps, ~3bps worse than expected (albeit this was broadly in line with peers).

Costs rose +3% to $5.1bn, 3% ahead of consensus, with the Cost-to-Income ratio slightly worse than expected at 49.6%.

ANZ: Past month

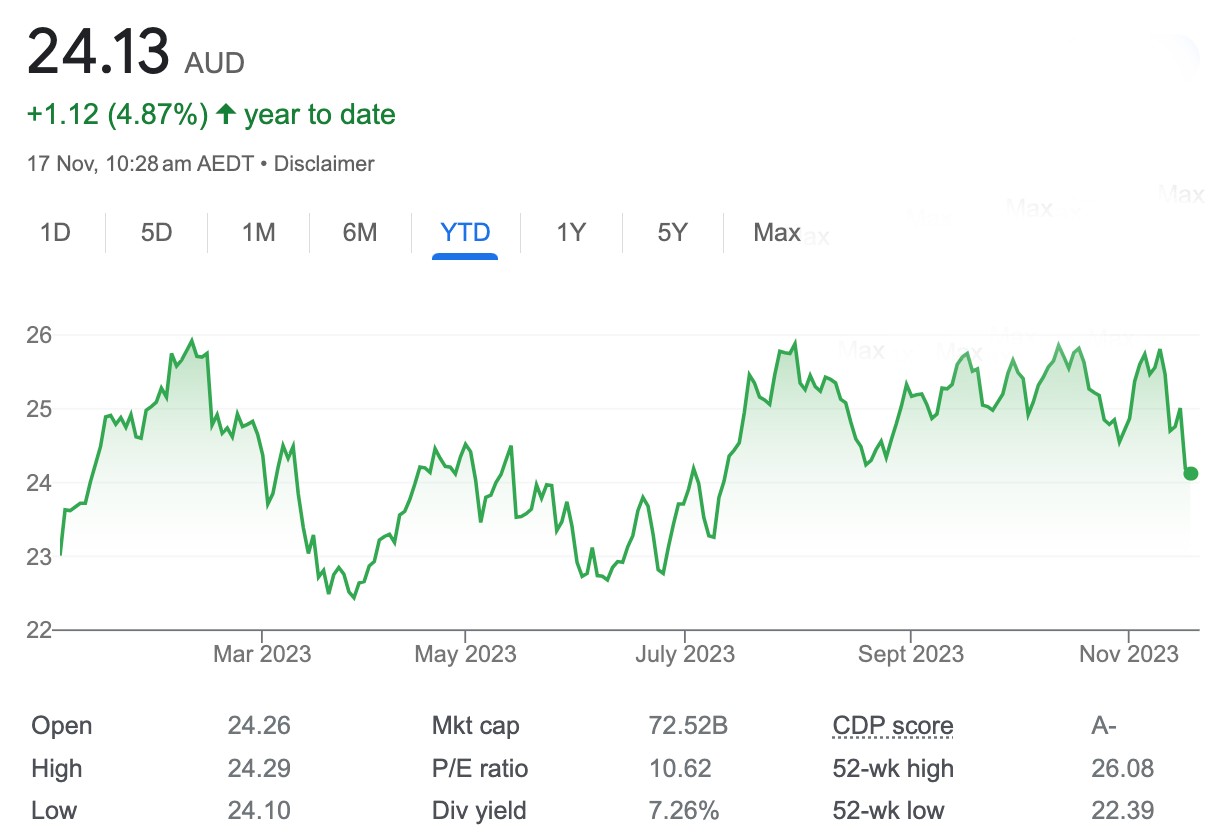

ANZ: Year-to-date

Citi says that even though the “miss” doesn’t appear to be significant, the analysts highlight the point that, compositionally, this is undoubtedly a “weak” result.

Despite some analysts already questioning ANZ’s low mortgage book of customers in arrears, credit impairment charges rose only 3bps.

Customers 90-days past due rose 4bps whole non-performing loans rose 7bps. ANZ’s collective provision coverage is much lower than peers and this will provide less buffer if the economic outlook deteriorates (although it is worth noting that ANZ is less exposed to recent mortgage vintage given their volume growth during and post-COVID).

Analysts have also fairly aggressively reduced ANZ’s FY24 and FY25 EPS targets by 7-9%.

Of particular interest is UBS, which has cut their dividend forecast for FY24 to $1.40, well below the $1.60 consensus and move to a sell rating.

The erosion of franking credits adds extra complexity, and investors should now factor in a partially (70%) franked dividend in their forecasts.

ANZ declared a final dividend of A$0.94 per share, comprising an A$0.81 dividend partially franked at 65% and an additional one-off unfranked dividend of A$0.13.

ANZ is trading at 11x P/E, in line with its historical average, although its almost 20% discount to peers is one standard deviation from its historical average of -10%. At 1x Price to Book, the stock is one standard deviation from historical averages.

Both market revenues and NIM proved a disappointment, offset by strong fee income and several one-offs. Citi also thinks opting for a bonus dividend instead of a buyback means there’s no benefit in terms of shares count moving forward.

Finding something on the upside, Citi says ANZ’s bad and doubtful debts were nearly half consensus forecasts.

So. That’s a little win.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.