Aussie ETF sector outplayed private managed funds last year by $40 Billion

Aussie ETF sector took in new money in 2022 as unlisted funds sustained heavy outflows. Pic:Getty Images

- Local private fund managers bled net outflows last year as the ETF sector hoovered them up

- Positive net flows still saw asset value declines on falling share and wonky bond markets

- A new record number of ETF launches in 2022

The Australian ETF industry well and truly out performed what ended as a shocking year for Australian managed funds, according to BetaShares’ Australian ETF 2022 Review.

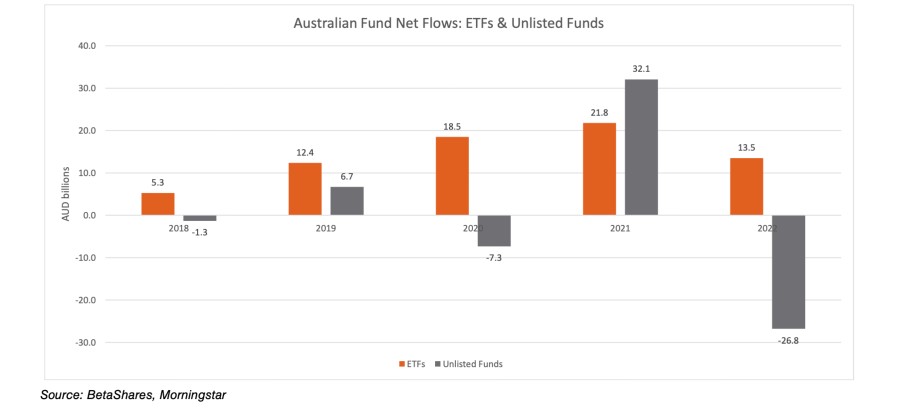

In total the Australian ETF industry received $13.5B of net inflows, in a year where the unlisted funds industry sustained net outflows of -$26.8B.

With the exception of 2021, ETFs have received higher flows than unlisted funds in four of the last five years.

Cumulative flows for the period were $71B versus the unlisted funds industry’s total net flows at ~$3B.

Inflows not enough to sustain asset value declines

Australia’s ETF industry’s positive net flows were unable to combat the asset value declines caused by falling share and bond markets.

The industry fell in value by 2% in 2022. Industry funds under management started 2022 at ~$137B but by year’s end were at $133.7B.

While 2021 saw an all-time record of $42 billion of growth 2022 was a different story with the change in total industry size for the year a decline of $3.2 billion.

However, BetaShares chief commercial officer Ilan Israelstam said net inflows still remained robust particularly given the broader picture for funds management, amounting to $13.5B .

This was 42% lower than the net flow figure recorded in 2021 of $23.2B, the highest net flows on record.

ETFs continue to grow in popularity

The industry saw 6% growth in the number of ETF investors with now 1.9 million Australians investing in ETFs,

“We also continued to experience strong trading values in the industry with annual ASX ETF trading value reaching an all-time high – with $117B of value traded on the ASX (compared to $95B in 2021, also previous record,” Israelstam said.

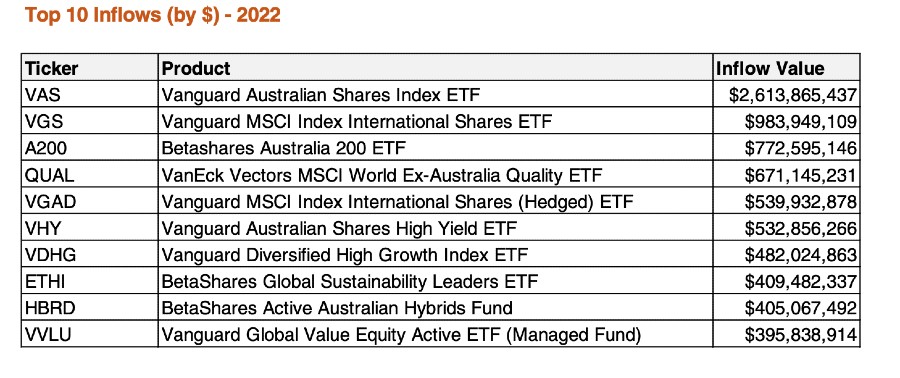

At an issuer level, the report showed ETF industry’s flows in 2022 were the most concentrated on record with the top 2 ETF issuers Vanguard and BetaShares receiving ~90% of the industry net inflows compared with 62% in 2021.

“With the number of participants in the industry now at 42, its notable that concentration levels are actually rising, rather than falling – illustrating the importance of scale in the industry,” Israelstam said.

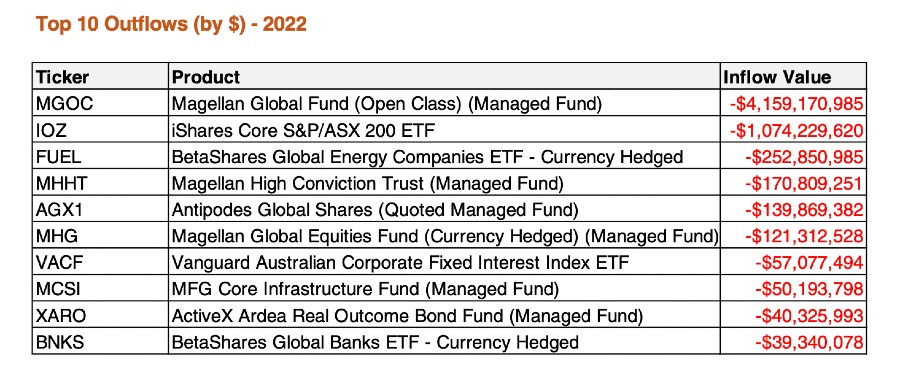

“Also notable was the fact that the 5 largest issuers for outflows in 2022 were all Active managers.”

Passive investing leads way in year of record ETF launches

It was the biggest year on record for product launches in the sector with 52 new ETFs launched on Australian exchanges in 2022, compared with 33 in 2021, while 13 products closed or matured.

There are now 319 exchange traded products trading on the ASX compared with 280 as at end 2021.

Similarly to the year before, a large proportion of the new launches in 2021 were active ETFs (33% or 17 new funds). As a result of the growing popularity of ETFs an increasing number of active fund managers are converting their traditional unlisted managed funds to ETFs via a dual access structure.

Israelstam said the majority of the new launches last year reflected this trend among unlisted fund managers.

“We would expect 2023 to again bring a number of new products, albeit not another record-breaking year given the breadth of product range currently available on ASX/CBOE,” Israelstam said.

He said 2022 was all about passive investing with significant outflows recorded in active ETFs, meaning more than 100% of the flows came from passive products.

“This trend is particularly striking given the large number of active ETF launches, with the actual flow activity seemingly not dissuading managers from launching active ETF classes of their unlisted funds,” he said.

Israelstam said within the passive category vanilla index-tracking funds once again dominated over smart-beta alternatives, although the smart beta category received 19% of total flows, a record to date.

Investors stay home in 2022

As geopolitical and economic concerns plagued global markets in 2022 overall Israelstam said global equity flows more muted than in previous years with the Aussie equities category leading net flows.

“Australian Equities ETFs received the largest amount of net flows, with ~$4.4B received versus $5.5B in 2021,” he said.

“International equities ETFs on a relative basis had a very quiet year, receiving $3.3B of net

inflows versus $11.8B in 2021,” he said.

Given market turbulence short leveraged US equity exposures were the best performing ETFs in 2022.

Israelstam said strong performance was also recorded in Global Energy and Australian Resources equity exposures given the popularity of these sectors in 2022.

Fixed income on comeback trail

Fixed income became the second most bought category of ETFs in 2022 with investors more willing to invest this asset class as yield rises began to taper off.

“Fixed Income ETFs had a very strong year with $3.6 billion versus $2.9 billion in 2021,” Israelstam said.

Reflections on 2022 and 2023 forecasts

In his end of year 2021 Israelstam said wrote regarding 2022: “we believe the industry will continue to grow strongly, although we doubt it will be as assisted by the market as occurred in 2021.”

He forecast total industry funds under management at the end 2022 to be in the range of $180-$190 billion.

“While I was correct that the market certainly hindered industry growth, I did not predict the extent of market declines which ultimately led to a small decline in the value of the industry,” he said.

“In terms of 2023, we believe that market conditions will continue to act as a hinderance to industry growth but expect net inflows to remain consistently positive and ultimately that the industry will return to a growth footing.

“As such, we forecast total industry FuM at end 2023 to exceed $150B in assets.”

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.