Aussie Property: The beast is back and what that means for prices in 2024

Via Getty

I think now we’re halfway through December one can safely say – without any rampant exaggeration or fulsomely ranging hyperbole – that the Australian property market is back to being a beast.

And it’s going to continue being beastly next year, according to the latest calculations from property data firm PropTrack.

Recovery amid rising rates

Australian residential has regathered all the strength it lost post-pandemic, and has quickly reverted back to its preferred state of urgent expansion, with sales well up on last year, auction rates highly annoying and capital city prices back at all-time highs.

Australia’s property market proved resilient in 2023, says Cameron Kusher, PropTrack’s director of economic research.

Residential sales volumes have surged some 15.5% on the same time last year, and all this despite the Reserve Bank’s culling of Australian borrowing capacity via 13 staccato rate rises in just 18 months.

“Home prices have increased 5.5% so far this year to a record high, despite deteriorating housing affordability and interest rate rises significantly reducing borrowing capacities.”

And the rebound in home prices is likely to continue in 2024 says Kusher, with national prices expected to increase between +1% and +4%.

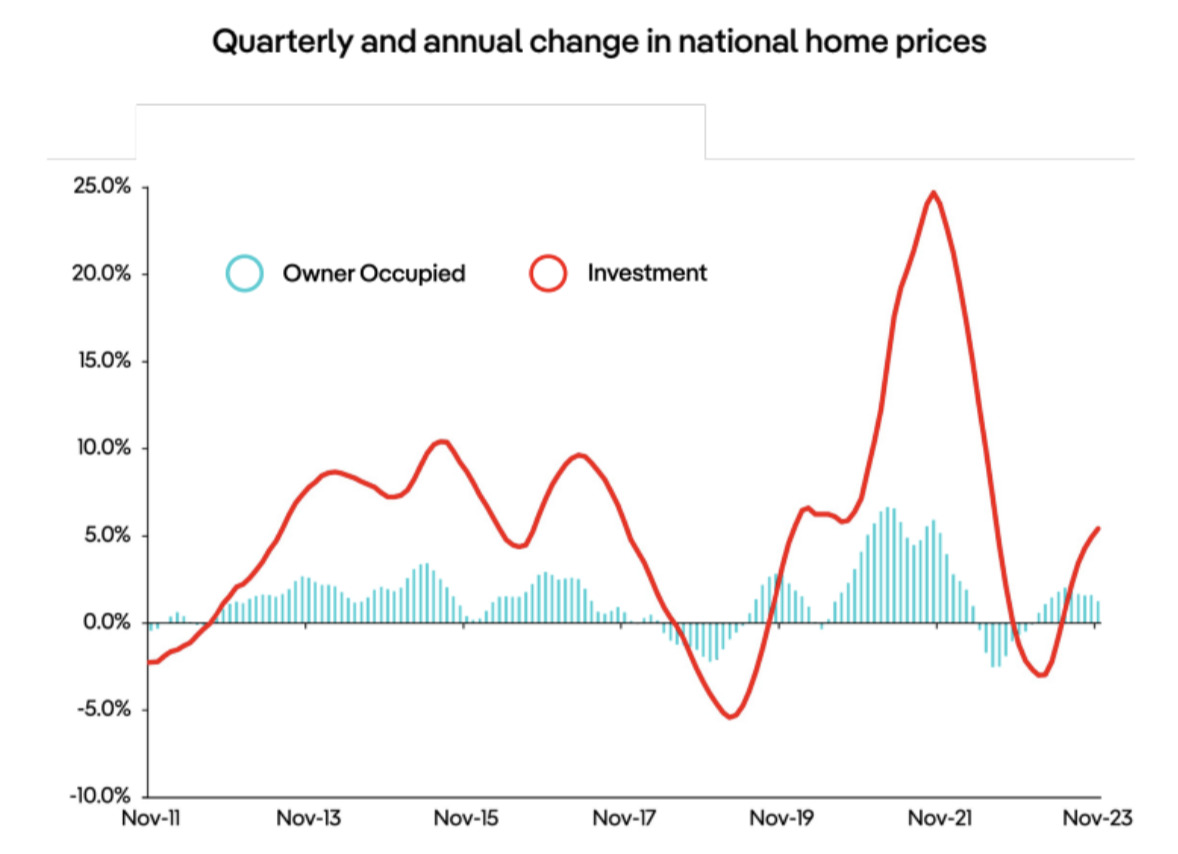

Everything is up

Aussie real estate, end 2023: the tale of the tape…

• In November 2023, home prices had risen 5.5% year-to-date to sit at a record high

• This has followed 11 straight months of price growth

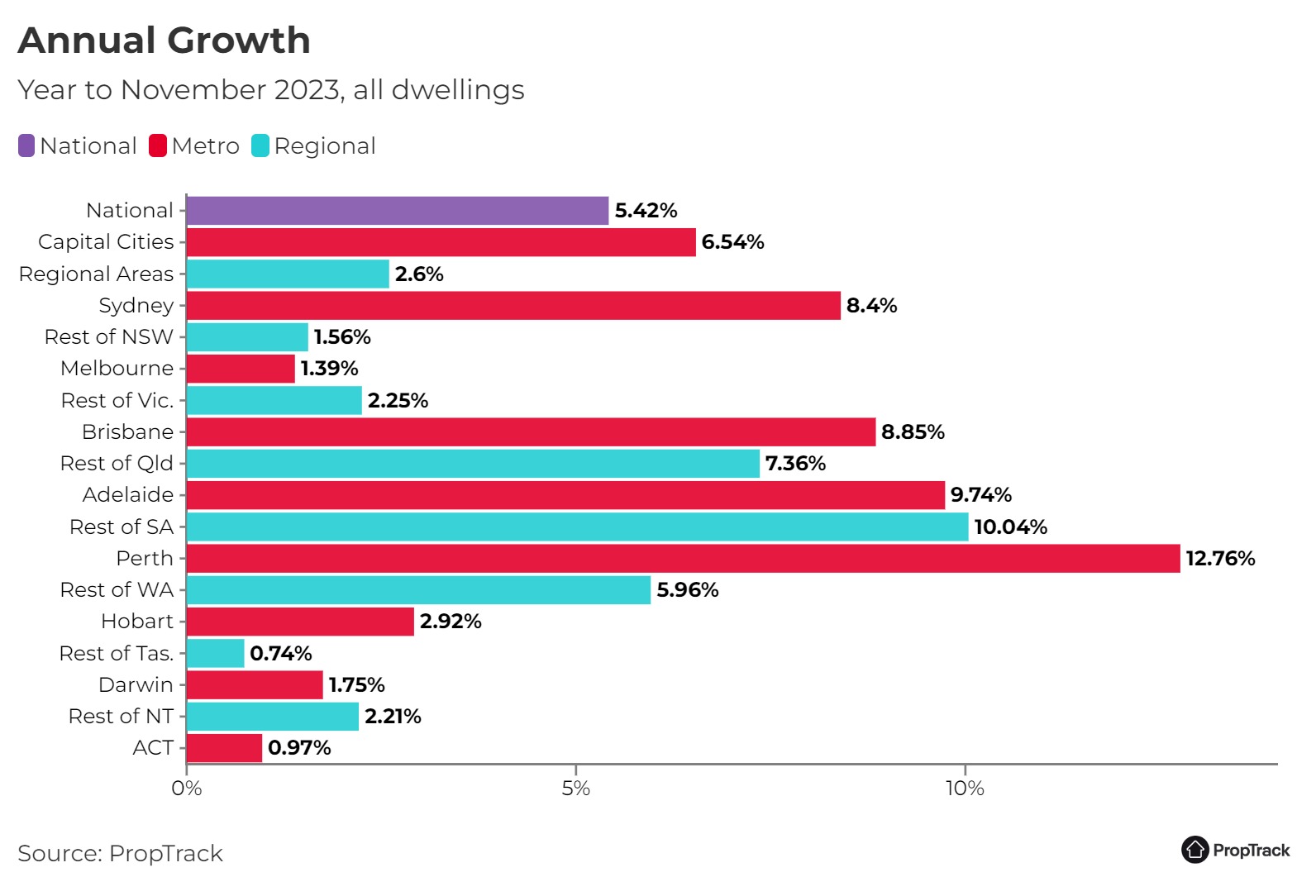

• Capital cities drove home price growth in 2023, rising 6.6% over the same period, compared to a 2.8% increase in regional areas

• Nationally, the total stock of properties for sale is historically low, sitting -23.9% below its November decade average.

• Buyers have been competing for a relatively low volume of stock. As a result, the number of enquiries per listing on realestate.com.au increased 20.5% year-on-year.

• Over the year, house prices have risen at a moderately faster pace than unit prices, with increases of 5.6% and 5%, respectively.

The score for 2024

Cameron Kusher says Aussie capital city house prices are rising faster (6.9%) than units (5.3%). The trend is reversed in regional markets, with stronger unit price growth (4.2%) than houses (2.5%).

Prices in Sydney (+2% to +5%), and Melbourne (+1% to +4%) are set to rise, though at a slower pace than they have in 2023.

Perth (+5% to +8%), Adelaide (+4% to +7%), and Brisbane (+3% to +6%) are likely to lead home price growth across the country after consistently recording strong gains in 2023.

Kusher adds that over the next 12 months, it is the smaller capital cities which may see slight declines or moderate gains over the year, including Canberra (-1% to +2%), Hobart (-2% to +1%), and Darwin (-3% to 0%).

Melbourne/Sydney auctions up +27% vs last year

Auction rates over the past four weeks are up some +18% on the same period before Christmas last year, although in Sydney and Melbourne – the auction capitals of the nation – scheduled auctions are up a staggering +27%.

Hobart is the only city with fewer auctions than last year, with the city taking longer to recover than others. However, Hobart has fewer auctions than the other cities, so this has not affected sales volumes.

Despite scheduled auctions being down compared to last year, sales in the regional areas are up everywhere… except Regional Tasmania.

Higher scheduled auctions indicate that agents think a higher price can be obtained by going to auction because demand is so high, according to PropTrack.

“The lower scheduled auctions in regional areas may show that agents don’t think the market is strong enough yet.”

Taxes and interest rates

Cameron says stage three tax cuts, due to kick off in July, will benefit higher income earners, and in turn, could lead to increased demand for higher priced housing.

“Interest rates are now at a 12-year high, and while they remained steady in December, there is a possibility of future increases, which could have an impact on buyer and seller sentiment.

“Reflecting on 2023, a number of factors drove the home price rebound. The volume of stock available for sale remained at persistently low levels while buyer demand also increased significantly, fuelled by a housing shortage and strong population growth. It’s likely these trends will continue into 2024.”

Capital growth

Capital city markets have led 2023’s price upturn, while regional areas have seen slower growth.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.