ASX Small Caps Lunch Wrap: Which idiot picked the worst possible time to go drink-driving last night?

I'm sorry, ossifer - I got confused when the red lights started blinking blue, and I thought I saw the President or something." Pic via Getty Images.

Local markets are up this morning, thanks to investors on Wall Street spending the session with their fingers in their ears, pretending not to be able to hear repeated words of warning from some frankly pretty knowledgeable people at the US Fed about rate cuts.

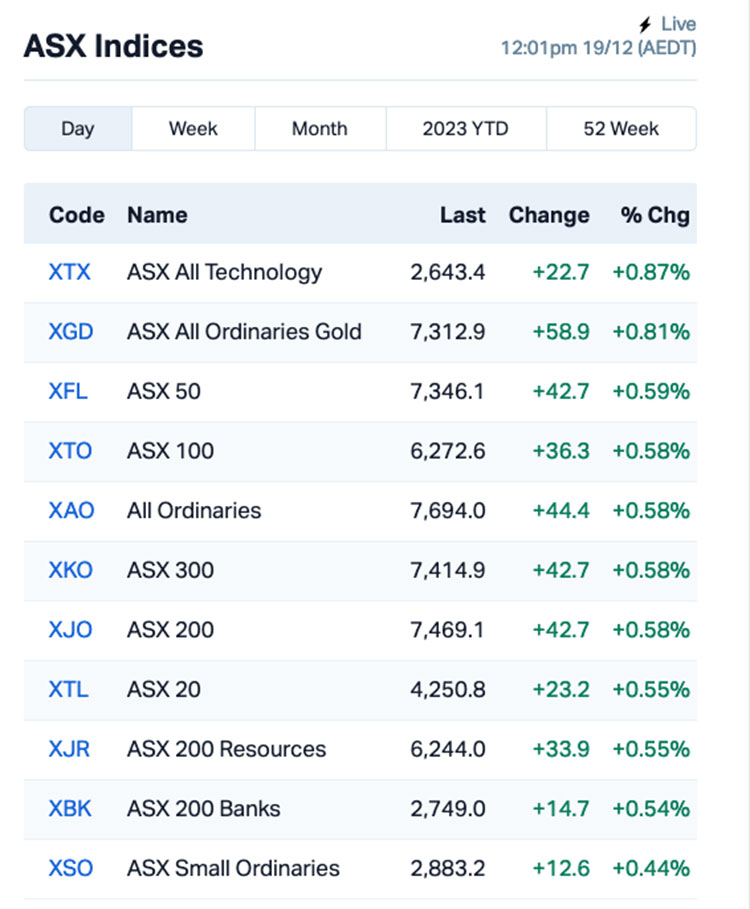

The mini surge on Wall Street, which is threatening all-time highs alongside the S&P 500’s best run since 2017, was enough to lift the ASX off the floor this morning, leaving it up more than 0.55% as lunch time trundled into view

I’ll get to the specifics of that in a second, but first we’re once again off to the US, where one driver is definitely going to be rueing their decision to get behind the wheel with a skinful last night, after drunkenly hitting a parked-up SUV in Delaware.

This is, at face value, a pretty solidly ho-hum piece of news – until I do one of those annoying big reveals… by telling you that particular SUV was part of US President Joe Biden’s motorcade.

As news footage taken from the moment when the accident occured shows, it startled the President pretty badly, and I’m willing to bet a good-sized chunk of this week’s pay cheque that a little bit of presidential wee came out.

Obviously, there’s never a good time to be getting behind the wheel when you’re drunk – and you’re a colossal piece of sh-t if you do, just so we’re clear – but there’s “having an accident while you’re driving” drunk, and then there’s “hurtling headlong into the presidential motorcade” levels of intoxication.

Turns out that nobody was seriously injured in the accident, but you could probably bet dollars to donuts that whoever was behind the wheel spent a decent slab of their evening staring down the barrel of several Secret Service firearms, as well as a lengthy stint behind bars.

The lesson here: Don’t drink and drive this Christmas. Or at all, really. It truly is a dick move.

TO MARKETS

Local markets are rising this morning, well above this morning’s prediction that had the ASX 200 index futures pointing up by +0.2% at 8:00am.

As lunchtime poked its head out through the top of the nation’s lunchpails and brown paper bags, the benchmark was climbing through 0.6% and showing plenty of upward momentum, as local investors tag along on the coattails of a surging Wall Street crowd.

But, right on cue, that momentum was curtailed by the release of the RBA Board’s minutes of its last meeting, which offered insight into why the board left local interest rates on hold when it met earlier this month.

It should come as no surprise that the highlights of the minutes are that the board has seen “encouraging signs” that the long, tortuous beating with the blunt instrument of rate hikes might actually have started to work in bringing inflation under control.

To which, Australian borrowers are saying “about f@$ing time, you bastards”, while investors pile back into a market that’s been running pretty hot for the past few weeks.

Once again today, there are some big gains at the top end of town. Liontown Resources (ASX:LTR) is surging, up more than 12% this morning, and Neuren Pharmaceuticals (ASX:NEU) is up another 8.3% so far today, off the back of yesterday’s strong news from the Phase-2 clinical trial of its NNZ-2591 drug for kids with Phelan-McDermid syndrome.

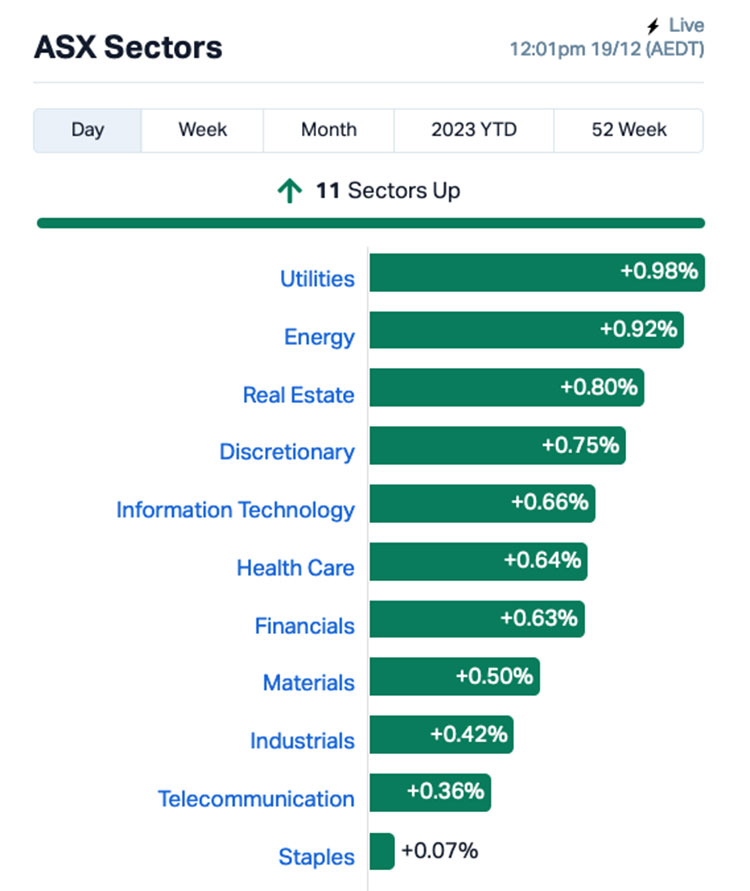

A look at the sectors shows a pretty buoyant snapshot this morning, with nothing absolutely racing for the metaphorical boundaries, just plenty of quick singles to be had.

And that exhausts my list of cricketing analogies for the summer… just so you know not to expect any more of that kind of nonsense from me.

Utilities and Energy are out in front, the latter experiencing upward pressure by a turnaround in oil prices overnight, in the wake of BP announcing that it was suspending oil shipments through the Red Sea, because some bastard keeps attacking the company’s boats.

I’m paraphrasing, of course, but that’s the basic gist of the news releases from BP headquarters.

That news sent crude prices up sharply, by more than 2.0%, or so I’m told – but at the time of writing, Brent crude was nudging US$78 a barrel, while WTI was still down around the US$72.30 mark.

On a more granular level, the XTX ASX All Tech Index is leading the market on +0.87%, and the XGD All Ords Gold Index reveals that the goldies are back in the good books this morning, adding 0.81% after a fairly wonky few days.

NOT THE ASX

Wall Street appears to have listened politely to the US Fed trying to hose down reports that it’s got rate cuts up the spout and it’s itching to pull the trigger, before summarily ignoring board members’ pleas for sanity and pushing hard for more gains this morning.

It was the turn of Cleveland Fed president Loretta Mester to be ignored last night, after she told the Financial Times that the market is a ‘bit ahead’ of the central bank on rate cuts as she tried to calm investor exuberance driving up stocks and bonds.

“The next phase is not when to reduce rates, even though that’s where the markets are at,” Mester said, her words falling on ears packed solid with thick, waxy pre-Christmas greed.

That’s why the S&P 500 rose by +0.45% – driving that index to its the longest weekly winning streak since 2017 – while the blue chips Dow Jones index was flat, and the tech-heavy Nasdaq lifted by +0.61% overnight.

In US stock news, Earlybird Eddy reports that Amazon was up 2.7% after a report from The Wall Street Journal suggested the company was in talks to invest in bankrupt Diamond Sports Group (DSG).

Steelmaker US Steel surged 26% after Japan’s Nippon Steel said it wants to acquire the company for US$14.9b. The move has outraged certain sectors of the political spectrum in the US – union leaders are furious that the company’s being sold to a non-union outfit, and conservatives are losing their minds that US Steel is being sold to a bunch of foreigners.

Apple shares fell almost 1% as the company said it will halt sales of its smartwatch to comply with a US import ban after a trade agency found it violated patents of a competitor.

ASX SMALL CAP WINNERS

Here are the best performing ASX small cap stocks for 19 December [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap MTM MTM Critical Metals 0.04 90% 1,807,347 2,088,179 NVO Novo Resources Corp 0.22 47% 1,687,551 6,740,720 CPO Culpeo Minerals 0.041 37% 28,697,570 3,496,871 1TT Thrive Tribe Tech 0.019 36% 768,281 4,152,701 AMD Arrow Minerals 0.004 33% 27,469,846 9,071,295 RGS Regeneus Ltd 0.004 33% 577,757 919,311 TKL Traka Resources 0.004 33% 127,000 2,625,988 ADR Adherium Ltd 0.045 32% 124,464 11,336,959 SGA Sarytogan 0.255 31% 2,375,235 15,005,232 DVL Dorsavi Ltd 0.014 27% 632,068 6,563,278 OEC Orbital Corp Limited 0.12 22% 466,115 14,289,060 KCC Kincora Copper 0.036 20% 811,382 5,995,052 LBT LBT Innovations 0.012 20% 53,667 12,564,543 AR9 Archtis Limited 0.125 19% 170,241 29,997,127 NGS NGS Ltd 0.013 18% 523,438 2,763,501 VTI Vision Tech Inc 0.27 17% 10,000 11,797,604 VAL Valor Resources Ltd 0.0035 17% 2,853,012 11,770,004 VR8 Vanadium Resources 0.05 16% 290,444 24,092,909 1AE Aurora Energy Metals 0.087 16% 804,544 11,940,520 LYK Lykos Metals 0.045 15% 394,043 2,433,600 KGL KGL Resources Ltd 0.15 15% 20,442 73,747,942 CL8 Carly Holdings Ltd 0.015 15% 1,075,590 3,488,815 ZMM Zimi Ltd 0.038 15% 1,000 3,973,114 RDN Raiden Resources Ltd 0.039 15% 39,829,903 90,215,174 ANX Anax Metals Ltd 0.032 14% 742,731 13,465,694

The big winner this morning is Novo Resources (ASX:NVO), which has slammed a 53.3% homer on news that SQM Australia has agreed to pay A$10 million for a 75% interest in five of Novo’s prospective lithium-nickel tenements in the West Pilbara.

SQM Australia, in case you missed all the other memos this year, is a wholly-owned subsidiary of Chilean giant Sociedad Química y Minera de Chile, which is 49% owned by China’s Tianqi Lithium Corporation, helmed by CEO Ricardo Ramos, and busily buying up everything it can get its lithium-stained hands on.

That deal will see the formation of the Harding Battery Metals Joint Venture, and also allows for an option over additional Novo Pilbara tenements down the track.

The Harding Battery Metals JV tenements are within neurological spitting distance of Azure Minerals (ASX:AZS) Andover lithium–nickel project, so everyone’s pretty excited about what the new collab is going to produce.

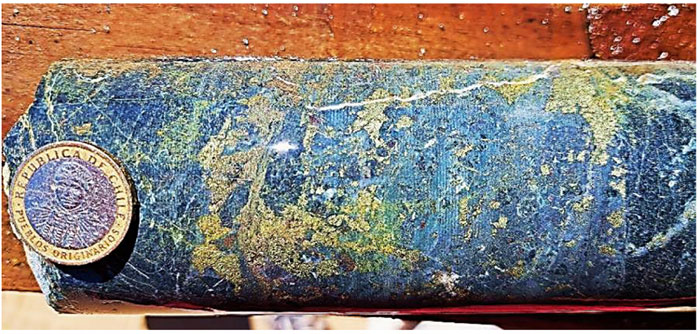

Meanwhile, Culpeo Minerals (ASX:CPO) has revealed that it has hit “significant widths of visible copper mineralisation” at shallow depth during drilling at its El Quillay Prospect, Fortuna Project in Chile.

Culpeo’s not kidding when it says that the copper is visible, either…

… the company says that’s indicative of a 40m intercept from a depth of just 15m from drillhole CMEQD002, where the near surface mineralisation was dominated by malachite and chrysocolla while in the primary zone the main copper mineralisation was in the form of chalcopyrite and to a lesser extent bornite.

(That last bit’s just a little sumthin’ sumthin’ for all you hardcore rock nerds out there… Happy Xmas, rockhounds…)

And Sarytogan Graphite is busting out the Christmas bubbly this morning, with news that the first spheroidised graphite from the Sarytogan Graphite Deposit in Central Kazakhstan has been produced.

The company says that a high combined spheroidisation yield of 54% achieved ideal D50 sphere sizes of 32, 18, and 12μm after classification, with high tap densities ranging from 0.91 to 0.99g/cm.

“What a way to end the year!” said an obviously very happy Sarytogan managing director, Sean Gregory.

“This result allays all doubts of the giant and exceptionally high-grade Sarytogan Graphite deposit’s suitability to vie for a share of the rapidly growing lithium-ion battery market for electric vehicles and other uses, subject to customer qualification.”

ASX SMALL CAP LOSERS

Here are the most-worst performing ASX small cap stocks for 19 December [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap CLE Cyclone Metals 0.001 -33% 2,568,878 $15,706,757 LNU Linius Tech Limited 0.0015 -25% 5,503,686 $9,383,581 MHC Manhattan Corp Ltd 0.003 -25% 510,209 $11,747,919 RML Resolution Minerals 0.003 -25% 100,000 $5,029,167 ID8 Identitii Limited 0.015 -25% 1,635,980 $8,604,760 88E 88 Energy Ltd 0.004 -20% 13,716,148 $123,204,013 CTN Catalina Resources 0.004 -20% 1,785,525 $6,192,434 MRD Mount Ridley Mines 0.002 -20% 700,000 $19,462,207 AML Aeon Metals Ltd 0.009 -18% 132,000 $12,060,407 TNY Tinybeans Group Ltd 0.12 -17% 39,329 $12,236,164 BTE Botalaenergyltd 0.075 -17% 80,359 $6,528,500 TMR Tempus Resources Ltd 0.005 -17% 4,907 $2,070,870 CI1 Credit Intelligence 0.18 -16% 57,344 $18,929,720 PHO Phosco Ltd 0.062 -16% 50,000 $20,306,588 CR9 Corellares 0.022 -15% 306,804 $12,092,363 TOY Toys R Us 0.011 -15% 427,000 $12,772,026 SNT Syntara Limited 0.023 -15% 512,683 $19,510,584 ADY Admiralty Resources 0.006 -14% 377,355 $9,125,054 CVR Cavalier Resources 0.12 -14% 32,198 $4,456,048 EXT Excite Technology 0.006 -14% 495,308 $9,304,692 H2G Greenhy2 Limited 0.006 -14% 146,303 $2,931,291 ORN Orion Minerals Ltd 0.013 -13% 1,189,849 $87,675,520 SHN Sunshine Metals Ltd 0.014 -13% 15,042,642 $19,584,135 AYA Artrya Ltd 0.175 -13% 79,500 $15,729,799 PBL Parabellum Resources 0.058 -12% 370,000 $4,111,800

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.