ASX Small Caps Lunch Wrap: What’s got one Japanese office worker losing his head this month?

Tinder really has a lot to answer for. What a terrible time to be alive. Pic via Getty Images.

The ASX has opened higher this morning, with investors feeling pretty confident that the June quarter inflation figure announcement by the Australian Bureau of Counting Things was going to bring good news.

Which, apparently, it did – and I’ll get to that in a minute or two, because there’s an interesting bit of news that I wanna tug on your coat about.

So, it’s time to head off to Japan, where news of a grisly murder in a dodgy ‘love hotel’ has the nation on edge.

The murder reportedly took place in one of the country’s so-called “love hotels” – ultra-short-stay accommodation most commonly used as a venue for a quick sexual tryst, but also very handy for anyone who feels like having a short nap in a sex swing bolted to the ceiling.

Police in Hokkaido say the body of a 62-year-old man, identified as office worker Hiroshi Ura, was found in the bathtub inside the hotel room, after he failed to check out within the agreed-upon time.

A search of the room discovered that the victim’s wallet, head, phone and clothes were missing.

Following a two-week investigation, police have arrested 29-year-old Runa Tamura, described by neighbours as “reclusive”, and by America’s ABC News as “a possible mental patient”, which seems like a pretty harsh sledge from the normally quite professional major US news network.

Just kidding. They’re monsters.

Police have also arrested the woman’s father, 59-year-old psychiatrist Osamu Tamura, on suspicion of being involved in the murder, along with his 60-year-old wife on conspiracy charges, after the victim’s head was found in their home.

The Japan Times says that an autopsy was carried out, and determined that the cause of death was “hemorrhagic shock”, which is a fancy way of saying “blood loss”, which – I’m told – is quite common when someone’s head gets cut off.

So far, there’s no idea on what might have prompted the bizarre killing, but as the story grips the nation, the Nikkei is down 0.5%.

Probably best that we move on to less gruesome news, and see if there’s anything causing local investors to lose their heads this morning.

TO MARKETS

Aussie markets opened 0.40% higher this morning, before flatlining ahead of the June quarter inflation figure announcement, which – thankfully – delivered some pretty good news.

The ABS revealed that inflation fell to 6% in the June quarter, down from 7% in the March quarter – and lo, there was much rejoicing and dancing in the streets.

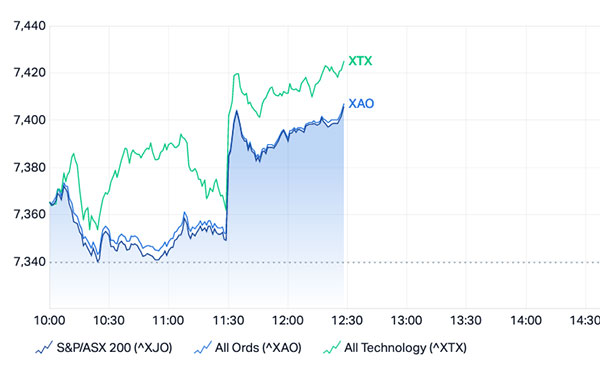

This handy chart should give you an idea of precisely when that ABS data went live:

I’m sure you’re all across it, but the baseline take home from the data is this:

- It lessens the likelihood that the RBA will raise rates again any time soon.

- The 6.0% figure is lower than market expectations, which were 6.2%

- The AUD has fallen because “no rate rise” = “cheaper money”.

The end result was the ASX hitting a 5-month high, up 0.9% from this morning’s open.

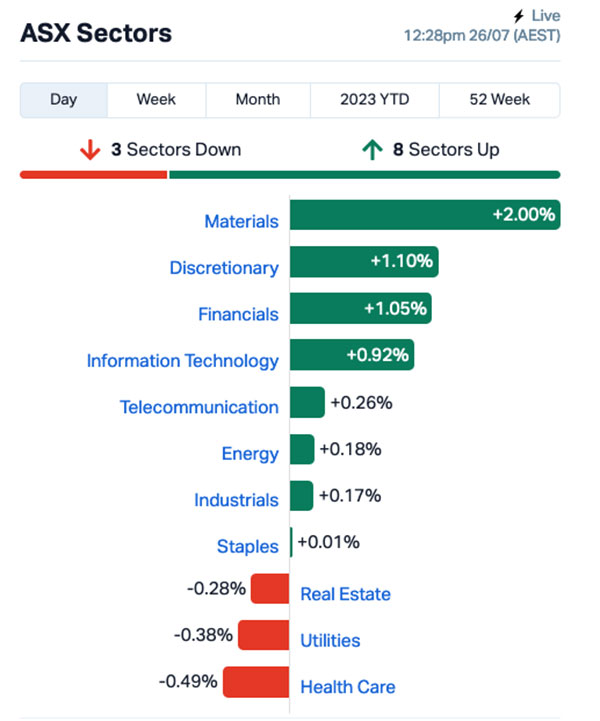

Sector-wise, there’s been a rush on Materials this morning, adding 2% to the running total, while Consumer Discretionary and Financials are locked in a tight race for second, adding 1.1% and 1.05% respectively.

Up the top end of town, where everyone’s neck-deep in caviar and even the toilet paper’s made out of gold, Beach Energy (ASX:BPT) has banked a 5.25% gain, and Champion Iron (ASX:CIA) is up 6.6% as well, sending conspiracy theorists’ social media into overdrive.

NOT THE ASX

It was a quiet-ish session on Wall Street overnight, but the mood was just positive enough to see the Dow – the venerable, creaky old man of US stock market indices – extend its winning streak to 12 days.

I don’t want to jinx it, but that leaves the Dow one short of equalling its longest winning streak ever, which was set in 1987, led by an almost unstoppable surge in the now-defunct Hair Spray and Cocaine sector.

The buzz around Wall Street that the Dow could set a new record is palpable. I know this because I’ve seen videos of Wall Street people palping, and when those people palp, things stay palped.

Anyway – the Dow rose 0.1%, the S&P 500 was up +0.3%, and the Nasdaq climbed 0.76%.

Earlybird Eddy reported this morning that Alphabet’s share price rose 6% after the bell as its Q2 profits beat expectations, with growth attributed mainly to steady demand for its Google Search and Cloud services.

Snap Inc plunged 19% after the bell as it announced that projected current quarter revenue is at the lower end of analysts’ estimates.

General Electric jumped 6% after raising its annual profit forecast, while General Motors fell 3.5% after posting a decline in profits and margins in North America.

US investors are now set to anxiously await the results of the latest Team FOMC meeting, with pretty much everyone expecting a 25bp rate hike, except for the people who aren’t expecting it, and a handful of people who are steadfastly remaining non-committal on the topic.

In Japan, the Nikkei has dropped 0.5% this morning because it’s a beautiful place full of dangerously weird people and things.

In China, Shanghai markets are down 0.26% as the nation ponders the disappearance of high profile foreign minister Qin Gang after less than seven months in the job.

It’s been an entire month since his last-known public appearance, and references to him are being methodically scrubbed from China’s foreign ministry website, leading many to believe he might – in diplomatic language – be a “goner”.

Meanwhile in Hong Kong, the Hang Seng is down 0.5% in early trade.

In the world of crypto, all eyes are once again on Doge – the dog-meme coin that is quite famously a favourite of TwitterX (or whatever it’s called today) part-owner Elon Musk.

It’s flying up the winner’s charts this morning on rumours ol’ Muskrat’s planning on using it as some kind of basis for turning his social media disaster into a rickety blend of far-right hate machine politics and an online payment system, possibly based on Doge.

ASX SMALL CAP WINNERS

Here are the best performing ASX small cap stocks for July 26 [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap AD1 AD1 Holdings Limited 0.007 40% 250,701 $4,112,845 OLY Olympio Metals Ltd 0.25 25% 605,521 $7,842,122 XTC Xantippe Res Ltd 0.0015 25% 12,380 $13,776,120 MRQ Mrg Metals Limited 0.003 20% 38,382,012 $4,964,797 TSL Titanium Sands Ltd 0.006 20% 2,877,105 $8,086,788 XST Xstate Resources 0.012 20% 397,038 $3,215,192 SBR Sabre Resources 0.033 18% 174,751 $8,161,613 ONE Oneview Healthcare 0.235 18% 446,900 $106,693,434 BDT Birddog 0.14 17% 136,480 $23,816,652 ILT Iltani Resources Lim 0.245 17% 12,663 $8,775,396 LNU Linius Tech Limited 0.0035 17% 1,046,250 $11,366,372 WSR Westar Resources 0.028 17% 8,739,141 $4,448,580 EMC Everest Metals Corp 0.18 16% 137,266 $20,062,132 ME1 Melodiol Glb Health 0.0115 15% 2,898,844 $26,885,538 KPO Kalina Power Limited 0.008 14% 1,155,026 $10,606,371 SIS Simble Solutions 0.008 14% 135,363 $4,220,655 WHK Whitehawk Limited 0.036 14% 2,281,746 $8,081,658 EXL Elixinol Wellness 0.0125 14% 510,302 $5,026,905 A8G Australasian Metals 0.17 13% 34,555 $7,818,074 AUN Aurumin 0.026 13% 642,344 $6,785,911 BFC Beston Global Ltd 0.009 13% 2,949,388 $15,976,375 IEC Intra Energy Corp 0.0045 13% 7,490,000 $6,483,126 MBK Metal Bank Ltd 0.036 13% 1,491,110 $8,847,537 ODM Odin Metals Limited 0.018 13% 1,000,000 $11,985,954 CDX Cardiex Limited 0.185 12% 268,749 $23,671,811

Up the top of the ladder this morning is Olympio Metals (ASX:OLY), which went booming 25% on no news this morning, until the ASX yanked on the handbrake at 11:48am with a trading pause.

Olympio has since requested a full-blown trading halt, to give it time to prep a response to the ASX’s “please explain”, and – tellingly – to put together an announcement about a “potential acquisition”.

Meanwhile, there’s been a bit of interest in Sabre Resources (ASX:SBR) this morning, again on no news – but the 17.8% jump in trading price has reversed some of the damage of the company’s recent steep loss that saw it fall around 40% since 21 July.

And Oneview Healthcare (ASX:ONE) is up 17.5% for some weird reason this morning, after dropping a less than positive quarterly showing a net operating cash outflow of €1.6 million (AUD$2.6 million), and 18% drop against the previous quarter, and 19% lower than the prior comparative period.

ASX SMALL CAP LOSERS

Here are the most-worst performing ASX small cap stocks for July 26 [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap SGC Sacgasco Ltd 0.005 -38% 26,017,716 $6,188,662 VPR Volt Power Group 0.001 -33% 299,998 $16,074,312 CLE Cyclone Metals 0.0015 -25% 4,137,327 $20,529,010 GCR Golden Cross 0.003 -25% 833,963 $4,389,024 ADR Adherium Ltd 0.004 -20% 9,919,794 $24,997,042 MTB Mount Burgess Mining 0.004 -20% 431,044 $4,415,856 IMI Infinitymining 0.125 -17% 163,133 $11,471,748 TMR Tempus Resources Ltd 0.025 -17% 830,354 $9,355,147 AJQ Armour Energy Ltd 0.0025 -17% 163,748 $14,764,026 NAE New Age Exploration 0.005 -17% 821,625 $8,615,393 ADO Anteotech Ltd 0.033 -15% 5,114,530 $79,947,603 DTZ Dotz Nano Ltd 0.21 -14% 306,425 $114,224,541 FAU First Au Ltd 0.003 -14% 5,818,333 $5,081,976 OPN Oppenneg 0.006 -14% 6,536 $7,816,757 APS Allup Silica Ltd 0.069 -14% 4,007 $3,078,168 SOM SomnoMed Limited 0.9 -13% 58,800 $85,242,094 1MC Morella Corporation 0.007 -13% 375,977 $48,788,644 ROG Red Sky Energy. 0.0035 -13% 973,774 $21,208,909 SI6 SI6 Metals Limited 0.007 -13% 2,320,291 $13,232,066 SLZ Sultan Resources Ltd 0.035 -13% 33,477 $5,927,602 LBT LBT Innovations 0.021 -13% 204,450 $8,299,096 KED Keypath Education 0.5 -12% 6,120 $121,963,543 AMA AMA Group Limited 0.1325 -12% 3,385,907 $160,960,533 ASB Austal Limited 2.28 -11% 5,100,610 $931,475,619 BCA Black Canyon Limited 0.16 -11% 154,088 $9,308,845

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.