ASX Small Caps Lunch Wrap: Has Japan unleashed a new colossal death robot this week?

Pic via Getty Images

Local markets have dipped this morning, with most sectors off slightly, leaving the goldies and healthcare out in front through the early part of the session. By the time lunch time hit, the ASX 200 was down -0.18%, and everyone was just about asleep.

There’s not a whole lot of news around today, market-wise, so let’s skip straight into something a little more entertaining from Japan, where it appears that the nation just cannot seem to stop flirting with disaster, by building enormous robots.

West Japan Railway has unveiled its latest mechanical monstrosity this week, and you can tell just by looking at it that it is 100% going to come to life, gain sentience and lay waste to the surrounding countryside.

Standing several metres tall, the robot is able to reach a vertical height of 12 metres with its massive arms, which are capable of hoisting payloads up to 40 kilos with ease, and can be fitted with paintbrushes, which is great – and industrial chainsaws, which is not great.

West Japan Railway’s new 40-foot-tall humanoid employee resembles a robot overlord from a 1980s sci-fi movie. It is, however, being utilized for far less sinister tasks like trimming tree branches along rails, the company says. pic.twitter.com/ghoa0F6J1O

— DW News (@dwnews) July 4, 2024

Weirdly, the robot doesn’t appear to have been given a fancy Japanese name, which is something that I suspect the people who built it have done on purpose. Once you name one of these monsters, it’s pretty much a foregone conclusion that it will rise up and destroy all humans.

But the robot’s developers have – I hope – covered off that eventuality as well, denying this mechanical beast the ability of independent locomotion. It is – for now – firmly anchored on the back of a truck, where it will be pressed into services trimming trees and fixing overhead railway wires.

Until it gets hit by lightning or stolen by an army of smaller, more nimble robots – and then, all bets are off.

TO MARKETS

It’s been a rocky start to the day for the ASX on Friday morning, without any action from the US to nudge us in any particular direction as Wall Street was closed for July 4 celebrations.

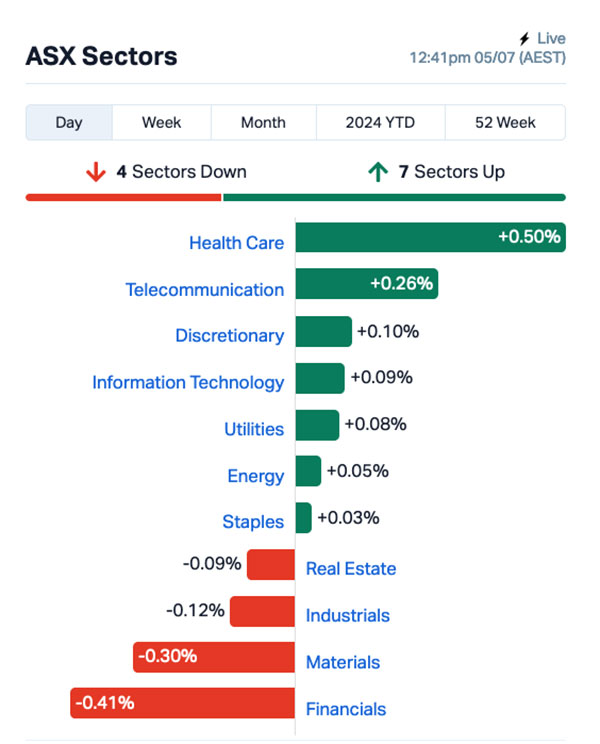

That left the market wide open and ready to rumble, which it did – quietly and slowly marching backwards for the most part, with most sectors down in early trade.

The exceptions were Health Care, which has enjoyed something of a gain this morning, mostly likely down to Melbourne-based Clinuvel Pharmaceuticals (ASX:CUV) , which released the results from a study (CUV151) evaluating the DNA-repair capacity of afamelanotide on skin of healthy volunteers exposed to ultraviolet (UV) radiation.

The company says that its testing showed that afamelanotide was able to reduce the number of differentially expressed genes in skin exposed to UV by a factor of 3.4 (from 625 to 183), and presented its findings at the British Association of Dermatology Meeting held last night.

And Utilities were up slightly, despite Santos retreating after reports that the company was being eyed for a takeover by Saudi Aramco and Abu Dhabi National Oil Company were scuttled by Aramco’s denial that it was interested.

On the way towards lunch, the ASX sectors looked like this:

The ASX Indices looked like this:

I looked and felt like this:

And I think it’s best we just move on from here.

NOT THE ASX

US markets were closed for Independence Day celebrations, so there weren’t no action from the mean streets of New York overnight.

In the UK, they’ve had an election, which looks almost certain to dump the Tories out of power and usher in a fresh round of Labour Party incompetence that will drive UK voters into the arms of the Far Right, and then we all just need to prep for the end of the world.

But that’s, like, ages away. Six months, at least, I reckon. In the meantime, European markets were broadly higher, with the FTSE up +0.86%, the Dax up +0.46% and everything else was broadly being pretty cool about the whole UK election thing.

Yields on UK government bonds were slightly higher just before midday in London, with the two-year yield up two basis points to 4.182%. I wish Eddy wasn’t on holidays. He’d know what that means.

In Asian markets this morning, Hong Kong’s Hang Seng is relatively flat at -0.15%, Japan’s Nikkei is up +0.39% and Shanghai markets are falling, down -0.52%.

ASX SMALL CAP WINNERS

Here are the best performing ASX small cap stocks for 05 July [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Change Volume Market Cap WML Woomera Mining Ltd 0.003 50.0 2,165,400 $2,436,278 EQS Equitystorygroupltd 0.022 46.7 376,585 $1,634,902 AQC Auspaccoal Ltd 0.096 35.2 675,072 $37,899,866 PUA Peak Minerals Ltd 0.004 33.3 34,070,200 $3,124,130 ZLD Zelira Therapeutics 0.460 27.8 9,817 $4,084,976 CCM Cadoux Limited 0.070 27.3 119,004 $20,400,467 TTT Titomic Limited 0.120 26.3 8,966,592 $96,010,406 SPD Southernpalladium 0.425 25.0 45,607 $30,515,000 ASR Asra Minerals Ltd 0.005 25.0 350,000 $8,144,317 LRL Labyrinth Resources 0.005 25.0 4,448,355 $4,750,175 SIS Simble Solutions 0.003 25.0 35,749 $1,506,901 VKA Viking Mines Ltd 0.010 25.0 1,087,931 $8,202,067 AL3 Aml3D 0.210 23.5 31,031,721 $64,106,835 GLA Gladiator Resources 0.018 20.0 886,325 $11,374,452 JPR Jupiter Energy 0.030 20.0 300,000 $31,841,305 DMG Dragon Mountain Gold 0.006 20.0 8,178 $1,973,358 ITM Itech Minerals Ltd 0.074 19.4 1,138,733 $7,581,581 WIN WIN Metals 0.026 18.2 1,486,732 $7,021,433 BWF Blackwall Limited 0.470 17.5 70,898 $67,121,026

Peak Minerals (ASX:PUA) was rising on Forday morning on news that the company has executed binding agreements for the acquisition of 80% of the highly prospective Kitongo and Lolo Uranium Projects and the Minta Rutile Project in Cameroon, West Africa. The acquisition includes six exploration permits under valid application covering an area of ~2,400km2, including the areas previously held by Mega Uranium Ltd (TSX:MGA) and actively explored until 2011.

iTech Minerals (ASX:ITM) was celebrating rock chip sampling results from Reynolds Range, which have come back with samples as high as 182g/t Au, with totals for copper, silver, base metals and lithium still pending, but they are expected to arrive in the coming weeks. =

And Zelira Therapeutics (ASX:ZLD) was performing well after recieving a shot in the arm – and a show of confidence – from the company chairman Mr Osagie Imasogie, who has provided the company with a $1.4 million unsecured loan. The loan was announced several days ago, and Zelira has informed the market that the money has arrived, and will be used to support the advancement of the HOPE SPV clinical trial, as well as general working capital purposes.

ASX SMALL CAP LOSERS

Here are the most-worst performing ASX small cap stocks for 05 July [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Change Volume Market Cap LPD Lepidico Ltd 0.002 -33.3 115,000 $25,767,358 MTL Mantle Minerals Ltd 0.002 -33.3 204,505 $18,592,338 88E 88 Energy Ltd 0.002 -25.0 29,633,864 $57,785,344 TMG Trigg Minerals Ltd 0.009 -25.0 1,171,724 $5,168,168 ALM Alma Metals Ltd 0.007 -22.2 280,000 $12,985,910 MMM Marley Spoon Se 0.026 -21.2 162,004 $3,884,905 GMN Gold Mountain Ltd 0.002 -20.0 2,200 $7,944,359 MRQ Mrg Metals Limited 0.004 -20.0 78,393,793 $12,625,593 ROG Red Sky Energy. 0.004 -20.0 214,090 $27,111,136 SMM Somerset Minerals 0.004 -20.0 2,984,362 $5,154,994 HT8 Harris Technology Gl 0.010 -16.7 66,653 $3,589,626 ME1 Melodiol Glb Health 0.003 -16.7 10,203,439 $691,387 BOC Bougainville Copper 0.480 -15.0 76,630 $226,600,313 ADG Adelong Gold Limited 0.006 -14.3 1,891,655 $7,825,923 ECT Env Clean Tech Ltd. 0.003 -14.3 33,025 $11,101,336 LML Lincoln Minerals 0.006 -14.3 200,000 $14,393,317 MOH Moho Resources 0.006 -14.3 2,744,480 $3,774,247 MPP Metro Perf.Glass Ltd 0.075 -12.8 7,919 $15,942,515 AAU Antilles Gold Ltd 0.004 -12.5 4,307 $3,986,140 TMX Terrain Minerals 0.004 -12.5 72,000 $5,726,683

IN CASE YOU MISSED IT – AM EDITION

It’s been a slow news day, so there’s nothing to see here. Go on, now… move along.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.