ASX Small Caps Lunch Wrap: Energy saves the morning session

Via Getty

The local stock market took a dive to kick things off on Monday, but solid action in the Energy Sector is profoundly distracting, with the early money on oil stocks and the hungry money on anything that even whiffs of Yellow Cake.

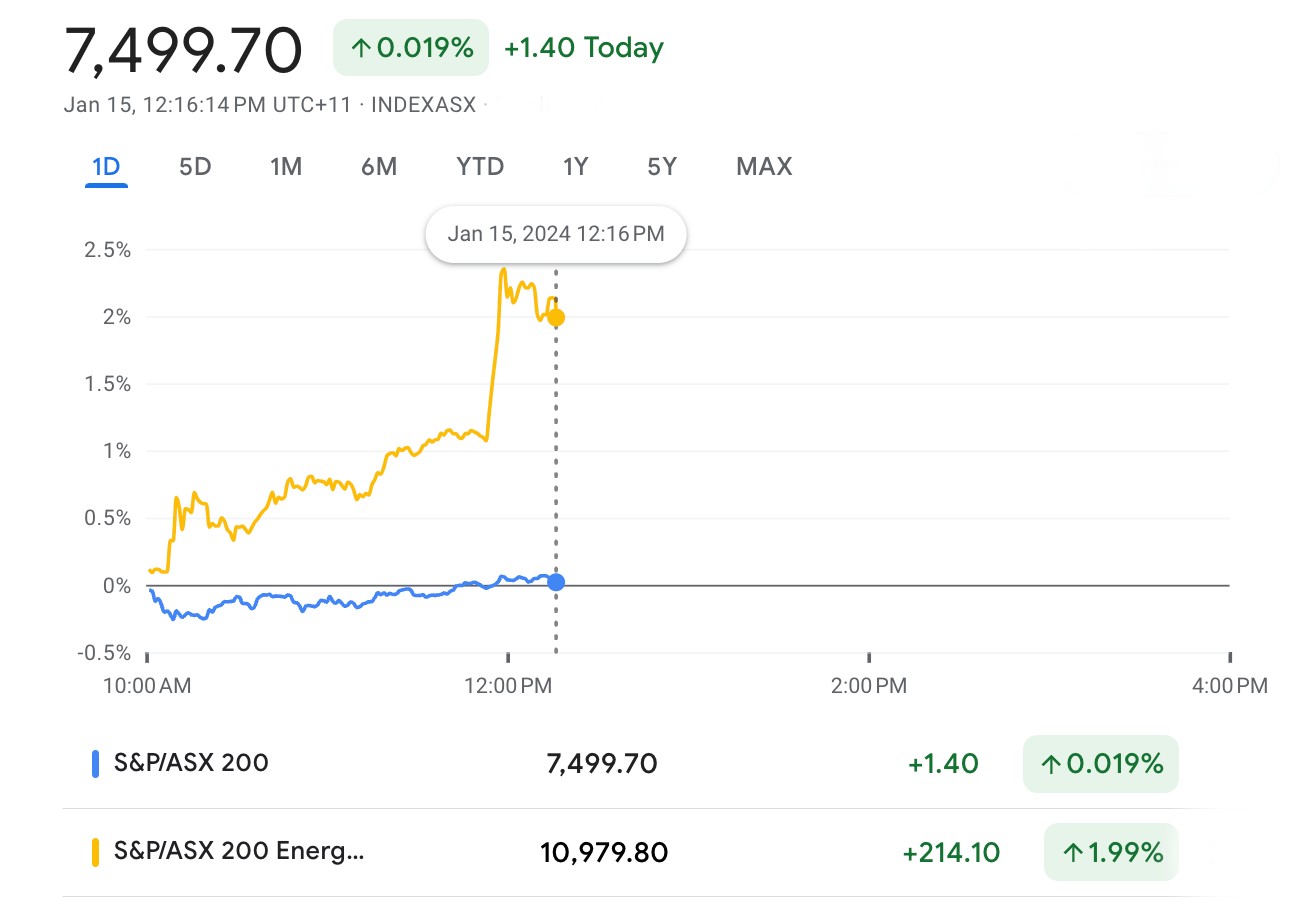

As a matter of fact, in the time it’s taken to whip up this little ditty about Jack and Dianne, the Energy Sector has ticked past a 2% gain, lifting the ASX benchmark by the breeches and hauling it into the green.

At 12.15pm on Monday January 15, the ASX200 was ahead by 1.4 points or 0.02% at 7450 points.

Friday on Wall Street was a mixed day of business after US CPI came in angrier than hoped for in the US, after Aussie November inflation dropped quieter than expected.

Crude prices climbed by around 1% as the nihilists at the World Bank felt it urgent to warn everyone of surging energy prices and higher inflation if conflict in the Red Sea spills over.

Which it then did.

But first, let’s talk U3O8.

In November, the spot price reached US$81.50/lb, on TradeTech’s assessment, but December witnessed the price breaking through US$90/lb for the first time in 16 years.

Amid increasing signs of strong demand and risks to supply, on Monday it’s getting hard to look past the action in the world of uranium, where prices smashed through US$92 a pound already this month – including a gain of well over US$6.50 on Friday – a blitz unseen in about 16 years and accelerating on the surge which began late in ’23.

No surprise then that the spot U3O8 has continued where it left 2023, breaking records and shunting some of the more obscure ASX small caps into the spotlight.

The Nuclear Energy Index increased US$176.15 or 8.9% since the beginning of the year, according to trading on a contract for difference (CFD) that tracks the uranium benchmark, leaving the NEI trading at an all time high over 2158 points.

For those to young to remember the heady days of the previous bull market circa 2006-07, the spot peaked at US$138 a pound and Paladin Energy (ASX:PDN) hit $10 a share despite looking a long way from delivering its first shipments.

Adding ballast to the sector, both West Texas and Brent oil futures lifted strongly over the weekend after we helped the Americans escalate the hell out of tension in the Middle East by launching a heap of air and sea strikes on Houthi targets in Yemen, following heaps of warnings against the heaps of Iran-backed Houthi attacks on the Red Sea’s critical shipping lanes.

Iran made the strikes a done deal when it snatched an oil tanker off the coast of Oman.

The Red Sea was already a hotbed of anxiety after months of Houthi rocket attacks on global shipping, which it says is in retaliation for Israel (and the US support of) military action in Gaza.

For the week, Brent prices rose nearly 2%, building on a 3% gain in the previous week.

At home, Santos has been given a timely boost after its $5.3bn Barossa LNG project was green-lit by the Federal Court which rejected a claim that the gas giant had failed to adequately consult and consider the impact of a 262km pipeline.

Santos (ASX:STO) has been banking on the Barossa development and the Monday announcement will relieve a multitude of sweaty stakeholder palms.

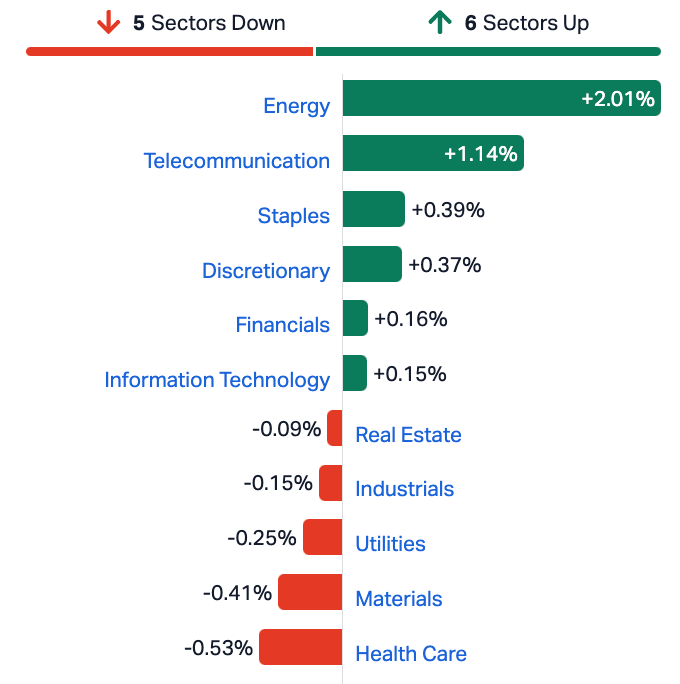

ASX SECTORS AT LUNCH ON MONDAY

On the bummer end of the bourse, Materials are weighing following a weekend decline in metals prices. The big names fell early across iron ore and metals producers, while gold stocks enjoyed the acceleration of fear and paranoia out of the Middle East.

Monday losses led early by both BHP (ASX:BHP) and Fortescue Metals Group (ASX:FMG) (down around 1%), Pilbara Minerals (ASX:PLS) (-2.5%) and Mineral Resources (ASX:MIN) (-2.3%).

It’s not nuts on the economic front this week, so the cues will largely come from China and the US, the latter taking a knee on Monday for the Martin Luther King holiday.

At home we’ve got consumer confidence and jobs data but not much else to light the way for the RBA’s ever important monetary policy outlook.

NOT THE ASX

In New York on Friday, the S&P 500 rose by +0.75%. The blue chips Dow Jones index was down by -0.31%, and the tech-heavy Nasdaq closed flattish.

Microsoft – a hard company to keep down at the worst of times – ended Friday back on the Mountain of Madness as the Universe’s Most Insanely Valuable Company, surpassing Apple. Again.

Microsoft rose circa 3.2% for the week, bringing its market cap to $2.89 trillion, while Apple’s stock dropped by almost the same, giving it a modest $2.87 trillion valuation.

It’s a critical week in the life of China and its gigantic/feeble economy, starting with the wrong card turning up again in Taipei after Taiwan went to the polls on Saturday.

Tensions with the US are also likely to be in the post as well after Taiwanese voters backed “Troublemaker” William Lai Ching-te as its President. China described the vote as a choice between peace and war.

Outside of that “probably nuthin'” moment in history, this week is all crucial data.

We’ll see the Q4 GDP read, a check up on maudlin retail sales, and industrial production, the ballpark unemployment numbers, and then finally the house price index under the shadow of a property crisis.

Earnings season is well underway Stateside.

The US banks JPMorgan Chase, Bank of America, and Wells Fargo all posted decent results on Friday.

The Nasdaq is performing at its usual pace, Meta gained +1.3% on no specific news, hitting 12-month highs.

Crypto-related stocks were mainly lower. Coinbase was down -6.7% and Marathon Digital by -12.6%, as the first US spot Bitcoin ETFs began trading.

ASX SMALL CAP WINNERS

Here are the best performing ASX small cap stocks for 15 January [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap YPB YPB Group Ltd 0.002 100% 384,000 $790,461 MOM Moab Minerals Ltd 0.009 50% 7,975,943 $4,271,781 EEL Enrg Elements Ltd 0.015 50% 22,216,517 $10,099,650 TZL TZ Ltd 0.034 36% 370,762 $6,418,953 CXU Cauldron Energy Ltd 0.049 32% 17,346,053 $41,915,046 T92 Terra Uranium 0.175 30% 1,897,234 $7,693,620 VAL Valor Resources Ltd 0.0045 29% 68,404,908 $14,606,672 ARE Argonaut Resources 0.135 29% 1,246,713 $19,932,719 KNB Koonenberry Gold 0.055 28% 36,395 $5,149,211 PEN Peninsula Energy Ltd 0.1325 26% 25,349,993 $132,353,061 ASV Asset Vision Co 0.01 25% 116,345 $5,806,693 GTI Gratifii 0.01 25% 500,001 $10,874,239 INP Incentiapay Ltd 0.005 25% 1,000,000 $5,110,859 IVX Invion Ltd 0.005 25% 236,086 $25,686,529 MCT Metalicity Limited 0.0025 25% 508,833 $8,970,108 ERA Energy Resources 0.055 25% 2,003,951 $974,525,164 1AE Aurora Energy Metals 0.16 23% 2,195,495 $20,696,901 GUE Global Uranium 0.16 23% 3,998,953 $27,587,166 ADD Adavale Resource Ltd 0.012 20% 8,713,393 $7,501,478 GTR Gti Energy Ltd 0.012 20% 20,071,514 $20,499,471 OAR OAR Resources Ltd 0.003 20% 3,000,000 $6,609,319 WCN White Cliff Minerals 0.012 20% 20,566,318 $12,768,593 LPE Locality Planning 0.043 19% 494,977 $6,487,359 BCM Brazilian Critical 0.027 17% 450,000 $17,019,007 NET Netlinkz Limited 0.007 17% 2,592,148 $23,032,885

It’s the Rise of the Uranium Caps on Monday.

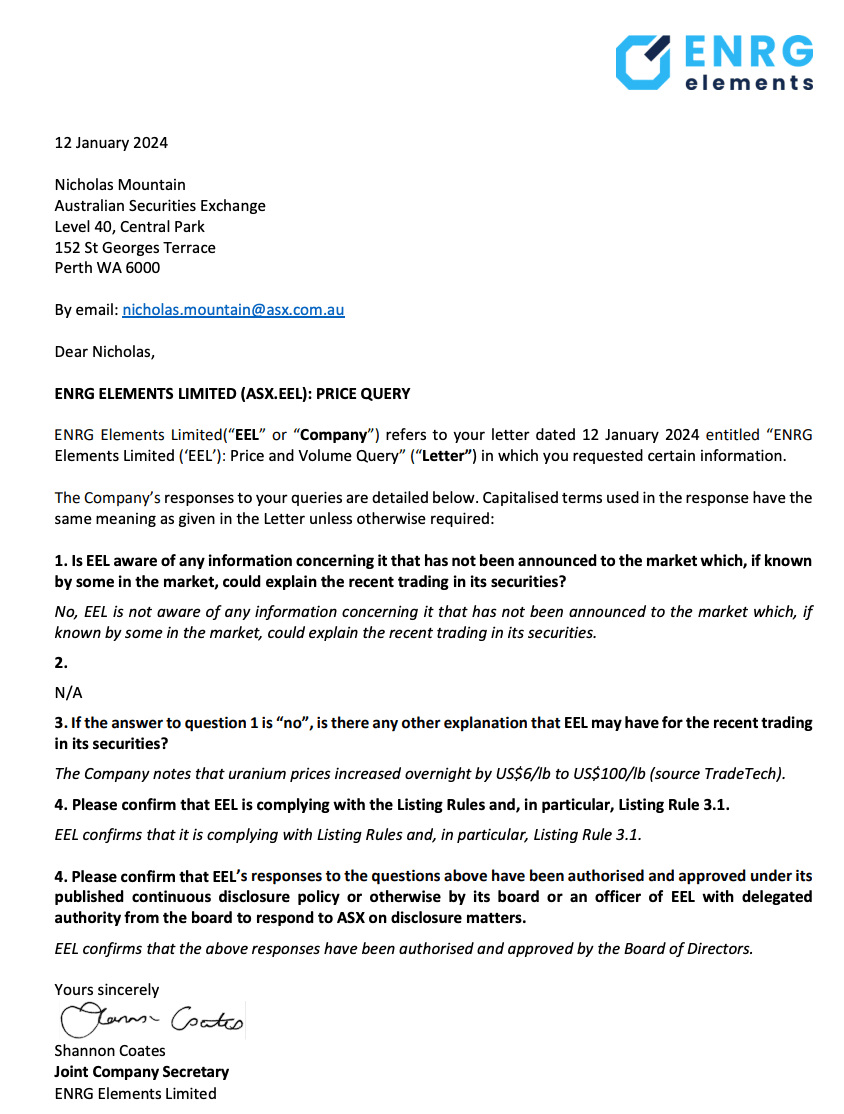

Way, way out in front is wee microcap ENRG Elements (ASX:EEL), where the outrageous outperforming began on Friday and didn’t fail to attract the notice of the ASX highway police.

EEL says it knows nothing, other than the leap in the price of uranium…

ENRG is up about 50% on Monday morning.

Meanwhile, White Cliff Minerals (ASX:WCN) has bolstered its blossoming Canadian portfolio with the acquisition of a historical mining operation in a region considered to have the strongest potential for IOCG-uranium style mineralisation in the country.

Previously focused on a range of exploration assets in Western Australia, WCN recently diversified its interests into Canada via the acquisition of some 61 mineral claims covering +805km2 in the Coppermine River area of Nunavut.

WCN says exploration has been largely non-existent in the area since uranium production ceased in the ’60s and silver and copper mining stopped in early ’80s.

Read More: This morning Stockhead’s Michael Washbourne’s all over White Cliff and anything else which has the Geiger counter ticking

Rounding out the top three is Terra Uranium (ASX:T92), which will also peg ground in Canada, this time in the Athabasca Basin.

ASX SMALL CAP LOSERS

Here are the most-worst performing ASX small cap stocks for 15 January [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap TAR Taruga Minerals 0.008 -27% 4,656,429 $7,766,295 BP8 BPH Global Ltd 0.0015 -25% 2,491,564 $3,671,126 CTN Catalina Resources 0.003 -25% 504,998 $4,953,948 DCL Domacom Limited 0.014 -22% 716,899 $7,839,032 BCA Black Canyon Limited 0.105 -22% 40,475 $9,469,097 KTA Krakatoa Resources 0.021 -22% 5,663,649 $12,746,895 FRB Firebird Metals 0.11 -19% 78,708 $19,218,789 OLL Open Learning 0.016 -16% 814,814 $5,089,512 MRZ Mont Royal Resources 0.11 -15% 38,424 $11,053,873 LBT LBT Innovations 0.011 -15% 61,123 $16,375,801 CY5 Cygnus Metals Ltd 0.1 -15% 601,905 $34,258,199 LVH Livehire Limited 0.05 -14% 69,161 $21,136,018 R3D R3D Resources Ltd 0.038 -14% 216,138 $6,704,349 HLX Helix Resources 0.0035 -13% 6,902,335 $9,292,583 LSR Lodestar Minerals 0.0035 -13% 1,027,484 $8,093,589 VMS Venture Minerals 0.007 -13% 338,635 $17,680,104 RDG Res Dev Group Ltd 0.04 -11% 5,019,911 $132,788,616 EXT Excite Technology 0.008 -11% 210,273 $11,963,176 GMN Gold Mountain Ltd 0.004 -11% 7,060,000 $10,210,854 NTM NT Minerals Limited 0.008 -11% 50,500 $7,739,126 TOY Toys R Us 0.008 -11% 4,206,249 $8,842,172 DCC Digitalx Limited 0.0465 -11% 1,292,056 $38,766,990 TNC True North Copper 0.086 -10% 566,023 $31,744,779 PIM Pinnacle Minerals 0.13 -10% 31,632 $5,026,152 NIS Nickel Search 0.062 -10% 5,744,653 $14,734,429

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.