ASX Small Caps and IPO Weekly Wrap: More downs than ups emerge from the latest 4-day week

While little Eduardo was having the time of his life, Grandpa Steve's Depends were copping the workout of a lifetime. Pic via Getty Images.

- The ASX 200 is on track to end the week pretty flat after last week’s losses

- Goldies struggled for traction after bullion prices retreated through the week

- Who won the Small Caps race? Read on to find out…

The ASX has improved somewhat over the past few days, which isn’t really that much of an achievement considering how poorly things turned out last week.

The gains this week have been modest at best, as investors struggled to figure out which way they wanted to jump.

The week’s forward momentum was hampered somewhat by news from the bean counters in Canberra, when the ABS revealed that the nation’s inflation rate had come in at 3.6% for the quarter on a year-to-year basis (+0.8% on a quarter-to-quarter basis) – higher than the 3.5% economists had forecast.

That knocked the wind out of the week’s mini-rally to slow the uptick to just +0.1% n Wednesday, as local investors paused to consider the lessening probability of an interest rate cut coming in 2024, since inflation is apparently refusing to cool the way it’s meant to.

Everyone in Oz took Thursday off to get on the piss and play two-up, and Friday began with an apparent nosedive after Wall Street took its own hard knocks through Thursday night local time.

That, coupled with the fact that a huge chunk of Australia’s workforce will have taken the opportunity to spend one day of annual leave in exchange for a four-day weekend – leaving just a skeleton crew keeping things ticking over today – has pretty much undone all of the progress for this week.

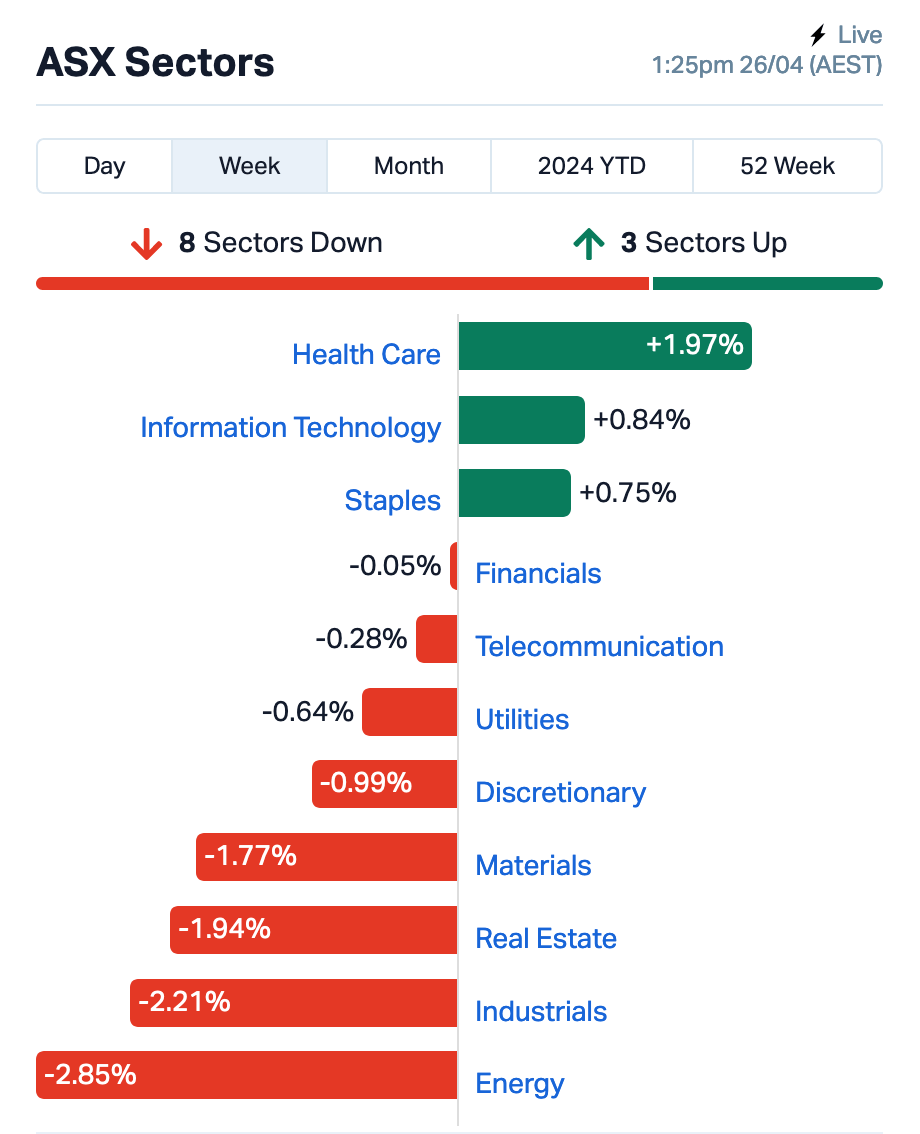

WHAT THE SECTORS DID

It was a tough week for a number of market sectors, with Energy bearing the brunt of investor squeamishness, shedding close to -3.0%. Industrials, Materials and Real Estate all posted losses north of 1% as well.

But the Health Care sector put in a stellar performance out in front, close to +2.0% ahead for the week with the help of market giant Resmed, which pumped out a very solid 7.0% gain early on Friday off the back of a highly positive quarterly – and news of a tasty divvy worth just shy of $0.05 to be paid later in the year.

Even with all the geopolitical upheaval around the place this week, the goldies have been surprisingly subdued. The usual safe haven took a hammering during the week after spot prices retreated to take a breather after a positive 5-week run, leaving that index with a single nostril above water, around 0.05%.

The best of the official indices belonged to InfoTech, with the XTX All Tech index showing about 0.60% of improvement.

SMALL CAP WINNERS THIS WEEK

| Code | Company | Price | % Week | Market Cap |

|---|---|---|---|---|

| OSX | Osteopore Limited | 0.41 | 242% | $3,511,754 |

| BSE | Base Resources | 0.2425 | 120% | $294,502,963 |

| RCR | Rincon | 0.053 | 89% | $9,067,206 |

| GLL | Galilee Energy Ltd | 0.05 | 79% | $13,589,786 |

| ORN | Orion Minerals Ltd | 0.022 | 69% | $105,233,124 |

| LNR | Lanthanein Resources | 0.005 | 67% | $9,774,545 |

| ZEO | Zeotech Limited | 0.041 | 64% | $59,616,384 |

| A3D | Aurora Labs Limited | 0.044 | 57% | $11,294,715 |

| ASE | Astute Metals NL | 0.051 | 55% | $16,831,299 |

| OZM | Ozaurum Resources | 0.063 | 54% | $11,430,000 |

| MRD | Mount Ridley Mines | 0.0015 | 50% | $11,677,324 |

| VRC | Volt Resources Ltd | 0.006 | 50% | $24,952,069 |

| WMG | Western Mines | 0.44 | 47% | $32,285,768 |

| VNL | Vinyl Group Ltd | 0.12 | 43% | $58,056,505 |

| CHW | Chilwa Minerals | 0.35 | 40% | $18,350,000 |

| SUM | Summit Minerals | 0.125 | 39% | $5,718,855 |

| ARR | American Rare Earths | 0.36 | 36% | $135,691,407 |

| M4M | Macro Metals Limited | 0.019 | 36% | $58,177,202 |

| L1M | Lightning Minerals | 0.1 | 35% | $4,644,757 |

| QPM | Queensland Pacific | 0.05 | 35% | $104,652,096 |

| AU1 | The Agency Group Aus | 0.035 | 35% | $15,000,181 |

| CT1 | Constellation Tech | 0.002 | 33% | $2,949,467 |

| EE1 | Earths Energy Ltd | 0.016 | 33% | $7,419,499 |

| GTI | Gratifii | 0.008 | 33% | $12,896,360 |

| IEC | Intra Energy Corp | 0.002 | 33% | $3,381,563 |

| JAV | Javelin Minerals Ltd | 0.002 | 33% | $4,352,462 |

| LNU | Linius Tech Limited | 0.002 | 33% | $10,393,481 |

| NNG | Nexion Group | 0.02 | 33% | $4,046,157 |

| SRY | Story-I Limited | 0.004 | 33% | $1,505,619 |

| LU7 | Lithium Universe Ltd | 0.033 | 32% | $13,585,998 |

| TSO | Tesoro Gold Ltd | 0.038 | 31% | $45,494,486 |

| RCE | Recce Pharmaceutical | 0.6725 | 31% | $139,707,026 |

| AUG | Augustus Minerals | 0.043 | 30% | $3,670,910 |

| NC1 | Nico Resources | 0.175 | 30% | $18,606,598 |

| CYM | Cyprium Metals Ltd | 0.031 | 29% | $45,741,370 |

| CPM | Cooper Metals | 0.135 | 29% | $9,794,456 |

| HOR | Horseshoe Metals Ltd | 0.009 | 29% | $5,830,008 |

| CY5 | Cygnus Metals Ltd | 0.095 | 27% | $27,115,000 |

| FRM | Farm Pride Foods | 0.125 | 26% | $17,982,232 |

| EXR | Elixir Energy Ltd | 0.145 | 26% | $164,234,293 |

| 1AG | Alterra Limited | 0.005 | 25% | $4,310,732 |

| AI1 | Adisyn Ltd | 0.025 | 25% | $4,056,040 |

| BLZ | Blaze Minerals Ltd | 0.005 | 25% | $3,142,791 |

| RB6 | Rubix Resources | 0.105 | 25% | $6,452,250 |

| SIS | Simble Solutions | 0.005 | 25% | $3,495,195 |

| TSI | Top Shelf | 0.2 | 25% | $41,735,172 |

| HCL | Highcom Ltd | 0.18 | 24% | $17,456,054 |

| WIA | WIA Gold Limited | 0.105 | 24% | $96,846,971 |

| CMD | Cassius Mining Ltd | 0.011 | 22% | $5,962,049 |

| DCL | Domacom Limited | 0.011 | 22% | $4,790,520 |

The best of the bunch this week turned out to be Osteopore (ASX:OSX) – which isn’t bad, considering it was the worst performing stock last week. It’s up a surprisingly massive +242%, rebounding and then some from the -68% beating it took at the hands of investors the week before.

The thing is, there’s not been a tangible reason for the stock to be moving the way that it has been – aside from suspensions and responses to several “Please Explain” postcards from the ASX watchdogs, there’s no real news coming out of OSX headquarters at the moment, so it’s a bit of a head-scratcher.

Base Resources (ASX:BSE) was next best in the list with an also-impressive +120% rise, thanks to news of a 100% takeover by US-based uranium and critical minerals producer Energy Fuels, by scheme of arrangement.

It’s a done deal, which will see Base’s investors score 0.0260 Energy Fuels common shares plus an unfranked special dividend of $0.065 for each Base Resources share held, equating to total consideration of approximately $0.302 per share.

That represented a premium to Base Resources’ last closing price of 188%, and a premium to the 20-day VWAP of Base Resources shares of 173%, correct at the date that the announcement was made, 22 April this year.

And in third place was Rincon Resources (ASX:RCR), with news of a string of new gravity targets to prioritise for drilling around its West Arunta ground. Those four new prospects are called K1, K2, Sheoak and Avalon, with three existing targets in the Pokali iron-oxide copper-gold prospect at Arrow, Dune and Surprise also enhanced by the ground gravity surveys. A program of works application has been submitted with WA’s mines regulator to enable RC drilling at all targets.

SMALL CAP LAGGARDS THIS WEEK

| Code | Company | Price | % Week | Market Cap |

|---|---|---|---|---|

| AXP | AXP Energy Ltd | 0.001 | -50% | $11,649,361 |

| TD1 | Tali Digital Limited | 0.001 | -50% | $6,590,311 |

| RFT | Rectifier Technolog | 0.009 | -47% | $15,201,823 |

| EMUDA | EMU NL | 0.016 | -47% | $1,012,386 |

| ECG | Ecargo Holdings | 0.018 | -42% | $10,459,250 |

| WML | Woomera Mining Ltd | 0.003 | -40% | $5,481,625 |

| KNB | Koonenberry Gold | 0.02 | -38% | $2,616,518 |

| OSL | Oncosil Medical | 0.0045 | -36% | $11,277,706 |

| BP8 | BPH Global Ltd | 0.001 | -33% | $1,954,116 |

| ERG | Eneco Refresh Ltd | 0.008 | -33% | $2,178,867 |

| GCR | Golden Cross | 0.002 | -33% | $2,194,512 |

| COB | Cobalt Blue Ltd | 0.096 | -31% | $35,935,019 |

| MBK | Metal Bank Ltd | 0.016 | -30% | $7,809,186 |

| AZI | Altamin Limited | 0.035 | -30% | $21,064,754 |

| BYH | Bryah Resources Ltd | 0.007 | -30% | $3,483,628 |

| NRZ | Neurizer Ltd | 0.0035 | -30% | $6,305,643 |

| NVU | Nanoveu Limited | 0.017 | -29% | $7,576,825 |

| NXS | Next Science Limited | 0.335 | -29% | $91,883,957 |

| AYT | Austin Metals Ltd | 0.005 | -29% | $6,425,957 |

| GTG | Genetic Technologies | 0.125 | -29% | $15,204,983 |

| SAN | Sagalio Energy Ltd | 0.005 | -29% | $1,023,301 |

| RR1DA | Reach Resources Ltd | 0.009 | -28% | $7,380,040 |

| SCN | Scorpion Minerals | 0.019 | -27% | $8,189,124 |

| LIO | Lion Energy Limited | 0.022 | -27% | $10,487,466 |

| ATP | Atlas Pearls Ltd | 0.1175 | -27% | $47,698,462 |

| VIT | Vitura Health Ltd | 0.125 | -26% | $60,466,748 |

| AM7 | Arcadia Minerals | 0.073 | -26% | $7,960,657 |

| DRO | Droneshield Limited | 0.83 | -26% | $514,780,515 |

| KGN | Kogan.Com Ltd | 5.15 | -26% | $513,506,724 |

| BUR | Burley Minerals | 0.061 | -26% | $7,952,628 |

| HAL | Halo Technologies | 0.093 | -26% | $11,963,185 |

| TNY | Tinybeans Group Ltd | 0.07 | -25% | $7,814,349 |

| ADD | Adavale Resource Ltd | 0.0045 | -25% | $5,079,898 |

| BDG | Black Dragon Gold | 0.021 | -25% | $4,966,889 |

| CYQ | Cycliq Group Ltd | 0.003 | -25% | $1,072,550 |

| EDE | Eden Inv Ltd | 0.0015 | -25% | $5,517,407 |

| KPO | Kalina Power Limited | 0.003 | -25% | $7,735,448 |

| LSR | Lodestar Minerals | 0.0015 | -25% | $4,046,795 |

| ME1 | Melodiol Global Health | 0.003 | -25% | $2,693,949 |

| MRQ | MRG Metals Limited | 0.0015 | -25% | $3,787,678 |

| OAR | OAR Resources Ltd | 0.0015 | -25% | $6,306,622 |

| WFL | Wellfully Limited | 0.003 | -25% | $1,478,832 |

| PAA | PharmAust Limited | 0.24 | -25% | $98,753,417 |

| FRE | Firebrick Pharma | 0.064 | -25% | $11,654,938 |

| HTA | Hutchison | 0.029 | -24% | $380,030,240 |

| NIM | Nimy Resources | 0.042 | -24% | $5,757,368 |

| FFF | Forbidden Foods | 0.013 | -24% | $2,953,905 |

| FCT | Firstwave Cloud Tech | 0.02 | -23% | $34,191,613 |

| FNR | Far Northern Res | 0.15 | -23% | $6,791,707 |

| C79 | Chrysos Corporation | 5.39 | -23% | $452,964,609 |

HOW THE WEEK SHOOK OUT

Monday 22 April, 2024

Absolutely circling the ASX from orbit on Monday was local critical mineral digger Base Resources (ASX:BSE) which revealed a proposed 100% acquisition by NYSE-listed uranium and critical minerals producer, Energy Fuels. Energy Fuels will offer 0.026 shares for every Base share as well as a special unfranked dividend of 6.5c per share, valuing the deal at 30.2c or $375 million. It’s a 188% premium to Base’s last closing price of 10.5c and 173% premium to its 11.1c 20-day VWAP as of April 19.

Next up, Orion Minerals (ASX:ORN) said initial results from diamond drilling at Flat Mine East, part of the Okiep Copper Project in the Northern Cape Province of South Africa, are showing the highest-grade drill intercept ever recorded in the area and confirm high-grade copper intercepts returned from drilling completed in 1995 by the previous owners, Goldfields.

Lightning Minerals (ASX:L1M) announced it would acquire option agreements over the Caraibas and Sidronio projects in Brazil’s ‘Lithium Valley’ within the mining state (literally) of Minas Gerais. L1M now holds projects in the three hot hard rock lithium districts globally of WA, Canada and Brazil. Caraibas and Sidronio cover 3372 hectares over seven tenements currently held by a private Australian company called Bengal Mining Pty Ltd.

Lanthanein Resources (ASX:LNR) said a new large lithium soil anomaly with a strike of ~4km has been identified in the recently completed soil sampling program at Lady Grey Project including a peak result of 454ppm Li2O, with a total of 527 samples returning ≥150ppm Li2O.

Rincon Resources (ASX:RCR) jumped after saying recently completed detailed ground gravity surveys have outlined multiple new anomaly high targets and enhanced three existing targets in the Pokali IOCG prospect (Arrow, Dune and Surprise). A program of works (POW) for reverse circulation drilling to test all targets has already been approved by the WA Department of Energy, Mines, Industry Regulation and Safety. A heritage clearance survey of new targets has also been submitted to accelerate drilling programs

Great Boulder Resources (ASX:GBR) said additional air-core (AC) and RC drilling at the Saltbush prospect has defined shallow, high-grade gold mineralisation over a strike length of ~300m. Highlights include: 4m @ 5.96g/t Au from 9m, and 3m @ 6.96g/t Au from 91m. Gold mineralisation appears to be plunging to the northwest, with RC drilling being planned to test this plunge in the next phase of drilling.

Tuesday 16 April, 2024

Augustus Minerals (ASX:AUG) says it may have have its copper targets at Tiberius and Claudius after releasing its rock chip assays today. Assays include a ripping 17.8% copper and 282g/t silver at Tiberius, which is currently 3m wide and 200m along strike. At Claudius, 11km to the south, results have outlined a number of parallel zones over 100m by 300m at grades of up to 6.6% Cu and 86g/t Ag.

Rincon Resources (ASX:RCR) jumped after reporting news of a string of new gravity targets to prioritise for drilling around its West Arunta ground. Those four new prospects are called K1, K2, Sheoak and Avalon, with three existing targets in the Pokali iron-oxide copper-gold prospect at Arrow, Dune and Surprise also enhanced by the ground gravity surveys. A program of works application has been submitted with WA’s mines regulator to enable RC drilling at all targets.

James Bay Minerals (ASX:JBY) says a field program is expected to start in the next four weeks to follow up airborne surveys, data from neighbouring properties and desktop studies completed since last year’s listing. “Our focus now is on ensuring that we target low-hanging fruit across all areas of the La Grande Project. This will ensure that we deploy capital efficiently on well-established targets,” said JBY’s executive director, Andrew Dornan.

Investors continued to digest Orion’s (ASX:ORN) big copper discovery at Flat Mine East, part of the Okiep project. That drill hit, by the by, was 49m at 4.86% Cu, well into the 99th percentile when it comes to copper discovery holes. The dual Australian and Johannesburg listed explorer also holds the fully permitted Prieska copper and zinc project.

Osteopore (ASX:OSX) popped big on news of the start of first-in-human clinical trials for knee preservation in Singapore, where the medtech specialises in “3D-printed biomimetic and bioresorbable” implants. Its first patient was treated for knee preservation with Heparan Sulphate 3 (HS3) and aXOpore via a High Tibial Osteotomy (HTO) at the National University Hospital (NUH), Singapore.”

Battery Age Minerals (ASX:BM8) says exploration targeting has begun at its Bleiberg Zinc-Germanium Project in Austria. It announced “senior geologists” had returned from Austria, “where they successfully accessed, collated and digitised over 100 years of historic mining data from the Bleiberg Zinc-Lead-Germanium Mine”. At time of its closure, the Bleiberg mine was the sixth largest producer of germanium globally and one of the largest outside of China.

Cyclone Metals (ASX:CLE) returned to the bourse with results of Phase 1 of the pilot plant test work for its flagship magnetite Iron Bear project. And the bourse liked what it saw. It also popped a quick 50% with $50k shares trading hands early on excitable quotes from CEO Paul Berend such as this: “The first phase of the pilot test work confirms the exceptional metallurgical properties of the Iron Bear deposit. We were able to produce one of the highest quality magnetite concentrates in the world with very high yields in an industrial setting.”

Wednesday 24 April, 2024

Western Mines (ASX:WMG) said a ~750m (and counting) deep drill hole hit ~700m of rock containing “disseminated nickel sulphide mineralisation and numerous sets of remobilised nickel sulphide veinlets” at the Mulga Tank project in WA. These cute veinlets — confirmed by spot pXRF up to 42.2% nickel — appear oblique to the drill core “indicating a possible source at depth”. Exciting times for the small explorer. The first 600m of core has been sampled and submitted to the lab for assay.

Canada focussed uranium and rare earths explorer, Newpeak Metals (ASX:NPM), completed a $300,000 share placement at 1.5c/sh to Gerhard Redelinghuys, founder of former small cap success story Bowen Coking Coal (ASX:BCB). NPM expects to have binding commitments for another $200,000 via placement shortly. It will also undertake a Rights Issue to raise not less than $500,000 at the same issue price as the Placement shares.

Also up strongly, Carbonxt Group (ASX:CG1) has had a good March quarter, with an 8% increase in quarterly receipts. Sales of Powdered Activated Carbon (PAC) were consistent q/q and up 56% on the prior period due to increased sales in non-coal fired power station channels. Aales of Activated Carbon Pellets (ACP) were up 37% on the last quarter.

Industrial Minerals (ASX:IND) has a maiden high purity quartz (HPQ) exploration target of 1.5-3 million tonnes grading 97-99% SiO2 at the Pippingarra quarry project in the Pilbara.

And Lycaon Resources (ASX:LYN) revealed that it has final permission to drill its Stansmore project, a proverbial stone’s throw from WA1 Resources’ (ASX:WA1) globally significant niobium find in the West Arunta region of WA.

Thursday 25 April, 2024

Market Holiday.

Friday 26 April, 2024

Osteopore (ASX:OSX) moved rapidly again (up +29.4% in morning trade) after getting another speeding ticket from the ASX about a sudden rise earlier in the week, which the company countered with some nonchalant whistling and a “nowt to see ‘ere, guvnor”.

And “Australia’s only ASX-listed music company” Vinyl Group (ASX:VNL) was moving rapidly in early trade, on news that Richard White’s investment vehicle RealWise Group will convert its convertible note into ordinary shares, giving it a 34% stake.

“I remain enthusiastic about Vinyl,” says billionaire and well-known stater of the bleeding obvious White, who is also CEO and founder of $30.5bn-capped Wisetech (ASX:WTC),

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.