ASX Small Cap Lunch Wrap: Local stocks rise on Wednesday morning after US traders spend up ahead of cash rate call

Via Getty

It’s early days, so no-one lose their bottle just yet, but the benchmark Aussie index has made a positive start to November.

It’s lunchtime on Wednesday and local markets are tracking, in their own timid way, some of the sneaky gains made on Wall Street overnight as The Fed’s big monetary meet continues to overshadow fresh corporate quarterlies.

The Federal Reserve’s FOMC decision will drop tomorrow morning – 5am Sydenham time – if you’d like to get out ahead of that.

For now, the major mining and healthcare names providing the leads.

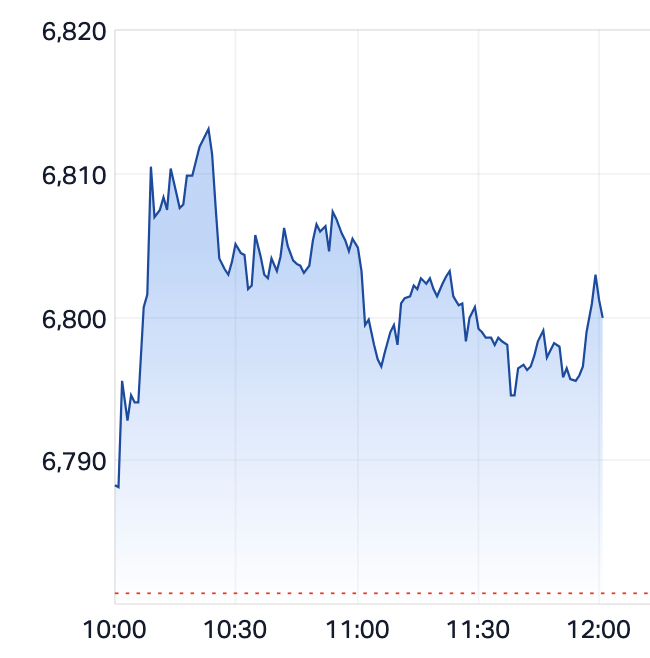

At midday AEDT the S&P/ASX200 was up 19 points, or 0.28%, at 6799.8 points.

The good news while we slept is that US indices rose overnight.

The S&P 500 benchmark closed +0.7% higher. The Dow Jones Industrial Average rose +0.4% and the Nasdaq Composite found +0.5%.

The bad news is October was Wall Street’s third straight monthly fall – a hat-trick which also happens to be the US markets’ worst streak of monthly contractions since COVID-19 broke them in April 2020.

The other October culprit, spikey US bond yields, only made marginal gains – traders also hitting pause ahead of the FOMC meeting (5am Sydney time) which is expected to be a low key affair as markets widely anticipate no change to the policy interest rate.

LUNCHTIME ON THE ASX200

ASX small caps continue to feature heavily in the ‘let’s sell’ corner of the local bourse. November so far doesn’t look too bad…

But last month and the last 12 months paint a clearer picture:

XSO — XEC

October — One Year

Meanwhile, Aussie home prices have lifted for a ninth straight month in October.

The 0.9% increase in property data firm CoreLogic’s capital city benchmark index released this morning describes an Aussie residential property market on the march, regardless of rising rates, inflation, cost of living pressures and all them other things.

Three Australian cities have now endured house price rises well into double figures in just the first 10 months of 2023.

-

Sydney (10.9%)

-

Perth (10.8%)

-

Brisbane (10.2%)

On the local bourse, local investors have turned to the big iron ore diggers and resources stocks after the Materials Sector’s losses on Tuesday which followed more grim economic data – manufacturing this time – out of China.

The BHP, Rio Tinto and Fortescue Metals all moved ahead, while the other market giant – healthcare company CSL – added almost 0.5%.

Elsewhere – at the smaller end of town – there’s movement afoot for Magnum Mining (ASX:MGU) which has signed an agreement with Midmetal of Saudi Arabia to jointly fund a feasibility study on producing zero-carbon “green” pig iron with Magnum.

Battery materials and tech company Novonix (ASX:NVX) announced that its NOVONIX Anode Materials division finalised its US$100 million grant award from the US Department of Energy to expand domestic production of high-performance, synthetic graphite anode materials at its Riverside facility in Chattanooga, Tennessee.

And also attracting attention on Wednesday is the newly listed lithium explorer Chariot Corporation’s (ASX:CC9) – our Nadine McGrath is digging around, noting a non-executive director has shown his support for the company, ponying up for 180,000 ordinary shares for ~$48k in an on-market trade.

ASX SECTORS AT MIDDAY ON WEDNESDAY

NOT THE ASX

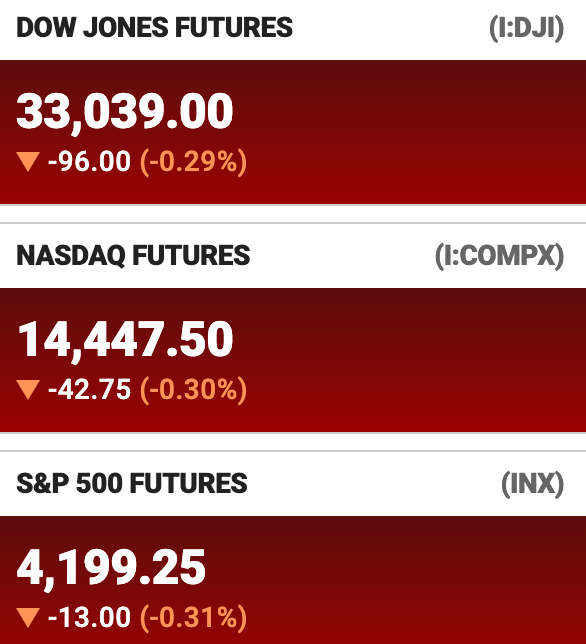

US stock futures have turned lower on Wednesday as pretty much everyone with a dollar in their pocket braces for the Federal Reserve’s November policy decision. The outcome might be a foregone conclusion – it is widely expected to hold interest rates steady – but how a priced-in but very fragile market responds could be interesting to watch.

In regular business on Tuesday in New York, all 11 benchmark S&P sectors ended the session higher led by real estate, financials and utilities.

The Dow rose +0.4%, the S&P 500 +0.7% and the Nasdaq +0.5%, as US indices climbed for a second session as October’s overselling attracts the opportunists.

It was another night of fairly mixed – let’s say hot and cold – corporate results, marginally rising US Treasury yields and the geopolitical background which continues to both deteriorate and add to broader economic uncertainty

Pfizer last night reported its first quarterly loss since 2019 as demand for its COVID-19 vaccine crashed by 70%, tearing a big hole on the big pharma’s revenue.

US futures at 9.30pm, Tuesday in New York

ASX SMALL CAP WINNERS

Here are the best performing ASX small cap stocks for 1 November [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap GHY Gold Hydrogen 0.435 50% 1,228,348 $16,507,677 BRU Buru Energy 0.17 42% 3,553,704 $71,525,170 LLI Loyal Lithium Ltd 0.57 37% 5,149,025 $33,789,764 VRX VRX Silica Ltd 0.12 29% 604,055 $54,254,205 DCL Domacom Limited 0.014 27% 582,971 $4,790,520 PIM Pinnacle Minerals 0.18 24% 4,767,911 $3,708,375 WML Woomera Mining Ltd 0.011 22% 8,845,553 $8,605,751 TG6 TG Metals 0.4 21% 7,072,569 $13,299,509 BFC Beston Global Ltd 0.006 20% 1,603,705 $9,985,234 TAS Tasman Resources Ltd 0.006 20% 1,000 $3,563,346 AUE Aurum Resources 0.13 18% 364,897 $3,455,000 EL8 Elevate Uranium Ltd 0.45 17% 1,194,114 $106,977,694 CPM Cooper Metals 0.105 17% 40,005 $4,789,588 RNO Rhinomed Ltd 0.035 17% 3,826 $8,571,591 ATH Alterity Therap Ltd 0.007 17% 70,429 $14,639,386 ETR Entyr Limited 0.007 17% 178,571 $11,898,623 HLX Helix Resources 0.0035 17% 701,737 $6,969,438 VAL Valor Resources Ltd 0.0035 17% 2,000,000 $11,620,004 NVX Novonix Limited 0.785 16% 7,962,170 $329,811,881 CPO Culpeominerals 0.036 16% 388,425 $3,324,147 NRZ Neurizer Ltd 0.029 16% 187,997 $31,918,481 AKN Auking Mining Ltd 0.044 16% 110,598 $7,755,941 SHP South Harz Potash 0.03 15% 496,157 $18,551,165 IDT IDT Australia Ltd 0.069 15% 1,163,740 $21,088,768

A delighted Loyal Lithium (ASX:LLI) gave the ASX an update on maiden drilling at its Trieste Lithium Project, located in… yes, the James Bay Region of Québec, in Canada.

“The drilling program is targeting Dyke #01, a large, prominent weather-resistant outcrop ridge, with all drill holes to date successfully intercepting spodumene bearing pegmatite. Dyke #01 remains open in all directions with drill core displaying large and abundant spodumene crystals from surface.”

The stock has gained 45% in morning trade.

Gold Hydrogen (ASX:GHY) says it’s locked onto significant concentrations of hydrogen and helium in its Ramsay 1 Well – which GHY reckons confirms historic measurement and demonstrating an active hydrogen system in the Ramsay Project area.

Here’s what they reckon they got:

Testing and laboratory results measured air-corrected hydrogen at 73.3% at 240m below ground level, consistent with the 76% air-corrected concentration of hydrogen reported in the Ramsay Oil Bore 1 in 1931.

“These measurements validate historical results, and confirm the presence of a hydrogen play at shallow depths in the Ramsay Project area,” the company reports.

“A major connected fracture zone was encountered in the Parara limestone, which is key for the migration of hydrogen from deeper sources to shallow zones.

“Helium was also detected with an air-corrected content of 3.6% at 892mMD depth. This is a relatively high concentration of helium which is a rare and valuable resource, and if found in commercial grades and quantities, could be a significant value-add to the Ramsay Project.”

Helium in its natural form is the rarest element in the universe – betcha didn’t know that. Globally there are projects producing helium at < 1% due to its high commercial value.

Managing director Neil McDonald:

“It is incredibly exciting that we have replicated the results of 100 years ago at 240m. With the additional find of helium, which could be a significant value-add to the project, we view these results as being better than planned.”

Next up, McDonald says, is the Ramsay 2 well – expected to spud in mid-November.

ASX SMALL CAP LOSERS

Here are the most-worst performing ASX small cap stocks for 1 November [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap AXP AXP Energy 0.001 -33% 131,340,258 $8,737,021 SIT Site Group International 0.002 -33% 5,340,000 $7,807,471 PAR Paradigm Biopharmaceuticals 0.43 -28% 5,482,247 $167,788,050 ALC Alcidion Group Ltd 0.0715 -26% 7,418,501 $123,232,028 PGY Pilot Energy Ltd 0.0245 -26% 32,556,520 $34,239,401 ADS Adslot Ltd. 0.003 -25% 8,024,412 $12,897,982 CCE Carnegie Clean Energy 0.0015 -25% 861,404 $31,285,147 PUA Peak Minerals Ltd 0.003 -25% 9,248,915 $4,165,506 NGS NGS Ltd 0.01 -23% 1,101,151 $3,265,956 EG1 Evergreen Lithium 0.19 -22% 50,000 $13,776,350 MGL Magontec Limited 0.36 -21% 181,850 $35,631,297 S3N Sensore Ltd 0.091 -21% 50,500 $4,185,222 NSX NSX Limited 0.027 -21% 169,971 $13,640,734 PVE Po Valley Energy Ltd 0.036 -20% 1,567,341 $52,153,273 LBT LBT Innovations 0.004 -20% 6,157,012 $1,779,502 MRQ MRG Metals Limited 0.002 -20% 19,531,395 $5,514,797 OSL Oncosil Medical 0.008 -20% 20,000 $19,758,411 SFG Seafarms Group Ltd 0.004 -20% 50,000 $24,182,996 AMT Allegra Orthopaedics 0.04 -18% 24,489 $5,860,940 ASH Ashley Services Group 0.385 -18% 152,122 $67,668,675 MXCDA MGC Pharmaceuticals 0.83 -17% 1,520 $4,427,969 EDE Eden Inv Ltd 0.0025 -17% 13,844,574 $10,090,911 ROG Red Sky Energy. 0.005 -17% 1,884,737 $31,813,363 HMD Heramed Limited 0.046 -16% 453,428 $15,373,281

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.