ASX Small Cap Lunch Wrap: Conditions suit the ASX

An old school commodity feast. Via getty

Like this girl I know, local markets are on fire. Not literally, otherwise I wouldn’t be sat here writing “this girl I know is on fire”.

I’d be chucking a bucket of water at her, or rolling her up in a blanket or something.

Anyway markets = hot. Put it down to an old school rally in commodity prices, the backbone of the ASX benchmark.

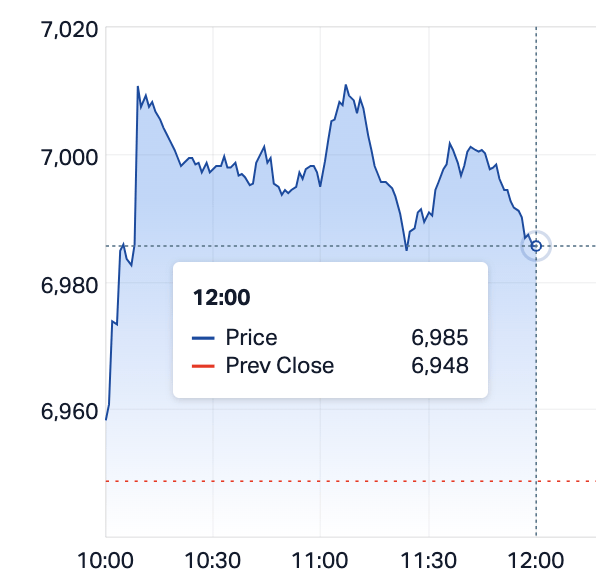

At 12pm on Tuesday, the benchmark ASX 200 (XJO) index is up 41 points or +0.59% to 6,990.

All the major miners have come out to play – BHP (ASX:BHP), Rio Tinto (ASX:RIO) and Fortescue Metals Group (ASX:FMG) lifted more than 1% each as iron ore futures extended gains into a fourth consecutive day.

Gold and lithium producers also climbed.

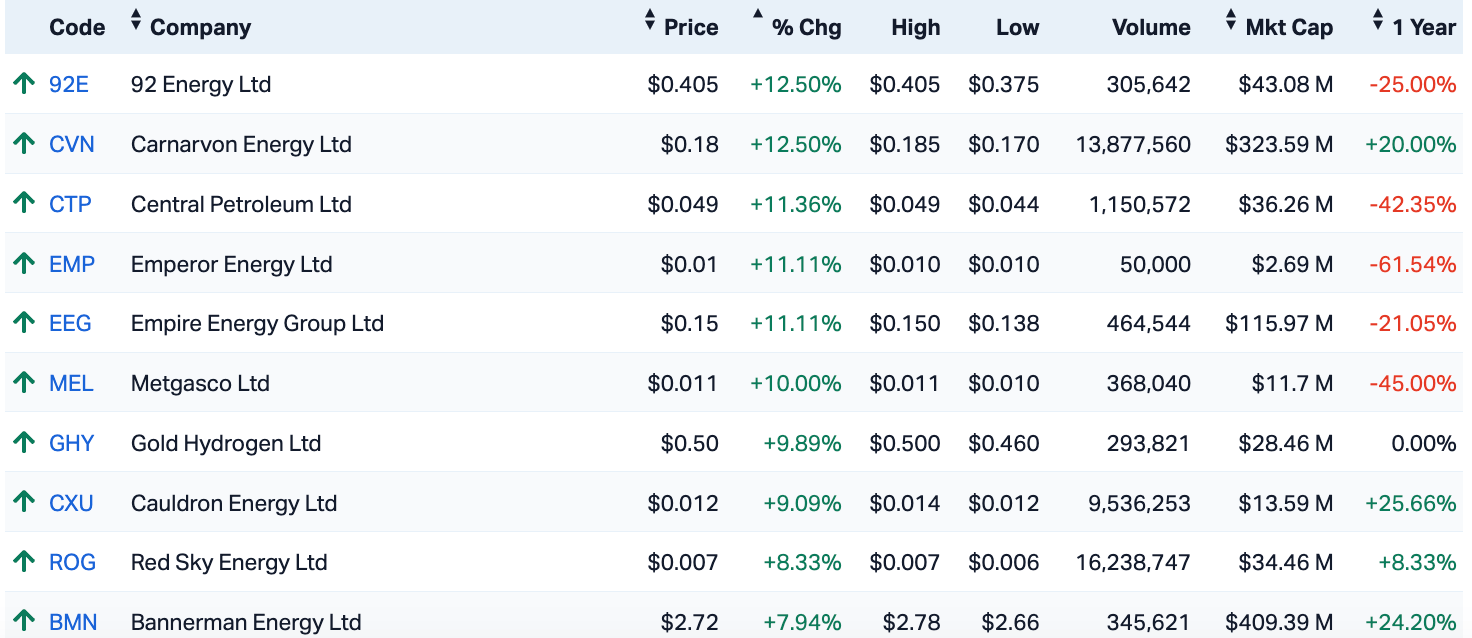

But the real strength is in the Energy Sector. How’s this look for a happy top 10 for the ASX Energy (XEJ) index:

Elsewhere gold and iron prices have rallied overnight with Goldman Sachs predicting increased returns of 21% on commodity prices over the next 12 months, led by energy and industrial metals.

Goldman believes commodities will rise as monetary policy eases, and because traders will be buying commodities to hedge against geopolitical supply risks.

NAB has gone ex-divvy, short some -2.7%.

This might come as no surprise at all, but Aussie consumer sentiment is now wallowing somewhere down at “deeply pessimistic” levels, according to the constant reminder that is the Westpac-Melbourne Institute Consumer Sentiment read.

The index fell 2.6% to 79.9 points thanks in no small part to the Reserve Bank’s return to hiking the cash rate this month.

And a few minutes ago, NAB’s business confidence index fell to -2 for last month, its lowest read since May.

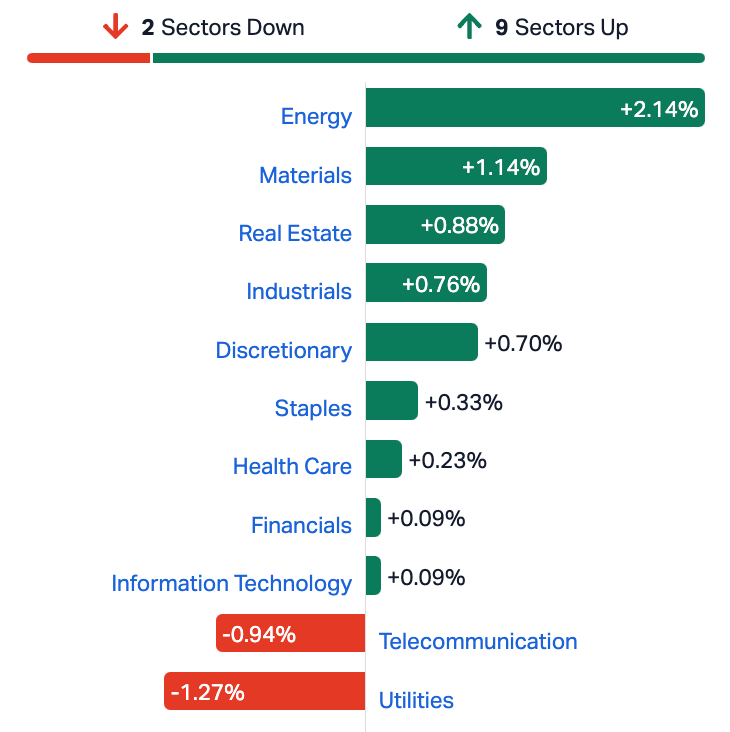

The big end of town’s outperforming along with industrials, real estate, discretionary, materials and tech.

ASX SECTORS ON TUESDAY

Lots of movement in Smallville on Tuesday, A2B Australia (ASX:A2B) says it’s exchanged contracts for the sale of its Downing Street, Oakleigh VIC, property for a cool $8m, bringing A2B’s total sales across all three of its properties, including the two in Sydney’s Alexandria – to $105 million.

A2B will enter into a two-year lease back over the Downing Street premises to enable the company to properly consider its longer-term property requirements, while the net impact to FY24 EBITDA is circa $275k.

Also making progress on Tuesday, Kingfisher Mining (ASX:KFM) after lobbing an update from its ongoing exploration at Mick Well within the highly prospective Gascoyne Province.

KFM executive director and CEO James Farrell say they’re seeing some significant additional carbonatites and REE mineralisation.

Farrell says there’s significant new strike lengths of REE mineralisation discovered from reconnaissance mapping close to the recently identified gravity targets as well as a substantial REE system confirmed, with more than 13.5km of mineralisation mapped so far within a very large 7km by 4km carbonatite complex.

“The latest discoveries confirm Mick Well is a very large and exciting REE system that extends over an area of more than 7km by 4km.

“Our ongoing fieldwork has also identified outcropping ferrocarbonatites together with monazite veining proximal to the recently identified carbonatite plug targets. These are the main ingredients for the World’s largest REE resources.”

Not the ASX

The major US averages were in a tangle overnight in New York, ending mixed in this fashion:

The S&P 500 down a smidgen, by -0.09%.

The Dow Jones was up by +0.16%.

The Nasdaq Composite fell by -0.22%.

US traders are agog, waiting for crucial US inflation data that will decide how, when and if the Federal Reserve again hoists US interest rates. Treasury yields rose slightly ahead of the US inflation report tonight, Sydenham time. A Reuters poll of economists reckons for a continued overall decline in inflation, led largely by easing energy prices.

Overnight Wall Street also digested the downgrade on the US credit outlook to Negative from Stable, by Moody’s. The ratings agency sees increased downside risks to US fiscal strength. I’m no ratings agency, but the US economy looks pretty resilient.

Among US stocks, Nvidia rose +0.6% following the announcement of updates to its H100 artificial intelligence processor.

Tesla gained +4.2%, and Boeing took off +4% on news that China might start buying its planes again.

Futures tied to the S&P 500, the Dow Jones Industrial Average and the Nasdaq were all higher at lunchtime in Sydney… by the barest of margins.

ASX SMALL CAP WINNERS

Here are the best performing ASX small cap stocks for 14 November [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

[Code Company Price % Volume Market Cap CPM Cooper Metals 0.285 104% 6,588,664 $7,450,471 AVE Avecho Biotech Ltd 0.005 43% 8,653,595 $9,444,022 ADS Adslot Ltd 0.004 33% 493,617 $9,673,487 KED Keypath Education 0.345 30% 20,948 $56,894,092 CCO The Calmer Co Int 0.005 25% 4,010,229 $3,268,477 CRB Carbine Resources 0.005 25% 500,000 $2,206,951 ME1 Melodiol Global Health 0.0025 25% 5,493,695 $7,668,207 MBK Metal Bank Ltd 0.033 22% 266,581 $9,701,200 BXN Bioxyne Ltd 0.012 20% 2,625,271 $19,016,454 ESR Estrella Res Ltd 0.006 20% 2,650,167 $8,795,359 RDN Raiden Resources Ltd 0.056 19% 55,362,699 $112,146,570 14D 1414 Degrees Limited 0.045 18% 365,451 $9,050,404 CXU Cauldron Energy Ltd 0.013 18% 9,821,253 $12,453,798 AKO Akora Resources 0.17 17% 33,650 $13,772,508 MTC Metalstech Ltd 0.14 17% 1,234,508 $22,632,551 ATH Alterity Therap Ltd 0.007 17% 8,263 $14,639,386 LML Lincoln Minerals 0.007 17% 3,280,171 $10,163,072 AI1 Adisyn Ltd 0.022 16% 22,000 $2,655,960 TG1 Techgen Metals Ltd 0.068 15% 2,811,884 $4,552,929 ACW Actinogen Medical 0.023 15% 5,419,899 $45,081,202 ERW Errawarra Resources 0.155 15% 1,054,435 $12,949,290 TMR Tempus Resources Ltd 0.008 14% 248,185 $2,400,460 LIS Li-S Energy 0.24 14% 98,963 $134,442,048 GHY Gold Hydrogen 0.52 14% 400,057 $25,899,975 AZL Arizona Lithium Ltd 0.049 14% 44,920,026 $142,707,799

In a cracking update this morning, Cooper Metals (ASX:CPM) says it’s got some significant assay results in hand from its Brumby Ridge and Raven Cu-Au Prospects at the Mt Isa East Cu-Au Project.

Initial RC drill hole 23MERC024 intercepted 50m at 1.32% Cu from 80m including 2m @ 6.1% Cu & 0.23g/t Au at the Brumby Ridge Cu-Au Prospect, which is the best assayed drill intercept at the Mt Isa East Cu-Au Project to date.

Follow-up drilling at Brumby Ridge, which commenced last week, intercepted an amazing 72m @ 1.5% Cu from 113m to end of hole, estimated from portable XRF (pXRF) hosted in strongly altered iron oxide copper-gold brecciated mafic volcanics.

Mineralisation at Brumby Ridge prospect is open in all directions, the company says, and appears to be improving with depth with this phase of drilling almost complete and assays due in December.

More significant mineralisation has been intersected at Raven, including 15m @ 1.0% Cu & 0.1g/t Au from 35m within a wider intercept of 28m @ 0.63% Cu & 0.061g/t Au from 34m (23MERC019).

Cooper Metals (ASX:CPM) MD Ian Warland says RC drilling should be done this week with results in December.

“To say we are pleased with the results of the initial scout drilling on five Cu-Au prospects is an understatement.

“The Brumby Ridge drill intercept is the single strongest mineralised intercept drilled by Cooper Metals in the last two years. Raven continues to expand with another great intercept into a home-grown conceptual target.

“These two prospects are now the Company’s main focus and are being followed up as we speak, as Cooper continues to test its pipeline of quality Cu-Au prospects in the region. This cluster of prospects, including Mafic Sweats South, are only around 30km to the SE of Mt Isa, close to infrastructure and worthy of further priority investigation and exploration by Cooper.”

Meanwhile, MetalsTech (ASX:MTC) has shared the results of a Scoping Study on its 100%-owned Sturec Gold Mine in central Slovakia, (if you must know – between the town of Kremnica and the village of Lučky, 17km west of central Slovakia’s largest city, Banská Bystrica, and 150km northeast of the capital, Bratislava).

“The Study confirms Sturec Gold Mine can support a Base Case scenario with an underground-only mining operation delivering gold and silver concentrate production of ~1.134Moz AuEq production over an initial mine life of 9 years at 2.3Mtpa plant production capacity.”

Keypath Education (ASX:KED) is holding its AGM today with chair Diana Eilert saying the company had a strong cash position of US$46.8 million at the end of June and remains confident of achieving profitability in the second half of FY24.

Metal Bank (ASX:MBK) says rock chips returned from reconnaissance work at its Malaqa project in Jordan include up to 8.70% copper from the Malaqa NW area ~3km from the historical Um el Amad and up to 2.51% copper in the vicinity of the Um el Amad mine.

ASX SMALL CAP LOSERS

Here are the most-worst performing ASX small cap stocks for 14 November [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

[Code Company Price % Volume Market Cap AQX Alice Queen Ltd 0.008 -43% 2,253,677 $1,771,208 AMD Arrow Minerals 0.0015 -25% 5,000,000 $6,047,530 XF1 Xref Limited 0.14 -22% 431,215 $33,511,732 EYE Nova Eye Medical Ltd 0.145 -22% 1,672,117 $35,266,345 RMX Red Mount Mining 0.004 -20% 2,014,238 $13,367,880 NGL Nightingale Intelligent Systems 0.044 -17% 23,518 $5,693,993 AUH Austchina Holdings 0.0025 -17% 316,356 $6,233,651 ICN Icon Energy Limited 0.005 -17% 175 $4,608,082 OSX Osteopore Limited 0.04 -17% 297,845 $7,436,094 RML Resolution Minerals 0.005 -17% 3,502,085 $7,543,751 NAG Nagambie Resources 0.031 -16% 1 $21,523,874 OCN Oceana Lithiuml 0.105 -16% 114,559 $6,634,563 3PL 3P Learning Ltd 0.96 -16% 139,440 $313,216,457 BRU Buru Energy 0.115 -15% 511,861 $80,465,816 ALM Alma Metals Ltd 0.006 -14% 1,571,429 $7,798,006 BFC Beston Global Ltd 0.006 -14% 1,600,000 $13,979,328 CCZ Castillo Copper Ltd 0.006 -14% 148,571 $9,096,537 GSR Greenstone Resources 0.006 -14% 4,128,385 $9,557,914 BKT Black Rock Mining 0.1 -13% 1,635,816 $126,191,759 LSA Lachlan Star Ltd 0.061 -13% 42,349 $14,530,124 AL8 Alderan Resource Ltd 0.007 -13% 4,544,429 $8,854,890 LNR Lanthanein Resources 0.007 -13% 2,554,807 $8,972,605 MTB Mount Burgess Mining 0.0035 -13% 1,000,000 $4,062,587 MTL Mantle Minerals Ltd 0.0035 -13% 1,068,460 $24,589,783

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.