The disinflation indicator making Chris Bedingfield sense the tailwinds of change

Via Getty

With the US economy showing signs of accelerating growth despite rising interest rates, Chris Bedingfield, principal & portfolio manager at real estate security focused asset manager Quay Global Investors, reveals why the refreshing winds of disinflation are ready to blow through the current economic uncertainty.

Chris is a co-founder at Quay Global Investors, and co-launched the Quay Global Real Estate Fund (Unhedged) in 2014. He has more than 30 years of experience working as a real estate specialist with a background in investment banking, equities research and investment management.

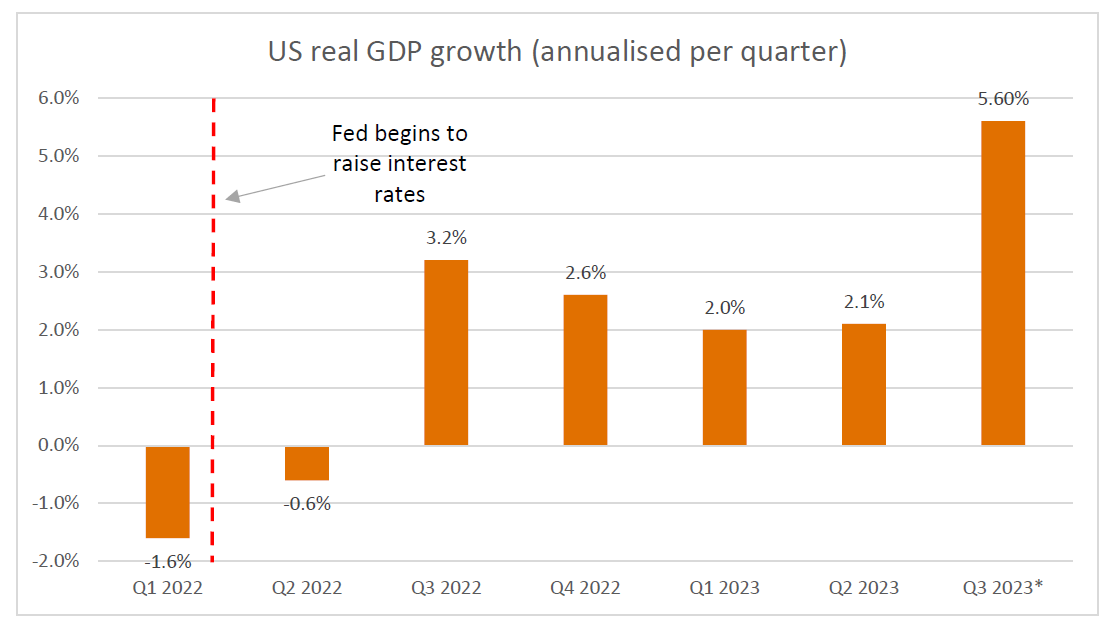

The first rule of Fight the Fed: There is no recession

“August saw a significant pivot in the global macroeconomic landscape,” says Bedingfield.

“Since the mini-banking crisis in March (remember that?), market expectations for the US economy have moved from a hard landing to a soft one, and now no landing at all.

“Based on the most recent US economic data, the world’s largest economy is now faced with accelerating economic growth – despite (or because of) higher interest rates.”

Source: US BEA, Atlanta Fed, Bloomberg, Quay Global Investors * 3Q GDP Estimate based on Atlanta Fed GDPNow (August 24)

Chris says the absence of the ever-looming US recession should come as no surprise.

“As Quay suggested back in September 2022, December 2022 and February 2023, rising interest rates in the US have a stimulatory effect on the US economy due to higher levels of fixed rate household mortgage rates, very large government debt, and associated accelerating net government interest expense (i.e. government spending).”

Just ahead of The Fed’s blockbuster Jackson Hole symposium in late August, a spike in US bond yields dragged Aussie long-term yields to decade highs.

The local 10-year rate climbing to a decade peak of 4.3%, as the US 30-year rate hit 4.47% a note not struck since 2011 and as the US 10-year bond yields clocked 4.37%, the highest since 2007.

In the face of stubborn US spending and doggedly economic progress the Federal Reserve’s message remains largely on song despite last week’s pause – “Higher for Longer” is the tune, and it’s while it’s not been an easy song to dance to, investors should soon be able to hum along.

“Bond investors have seemingly capitulated on 2024 interest rate cut expectations, and long-end rates have been on the rise,” says Bedingfield. “And while the observed data in other economies is starkly weaker relative to the US, long-dated bonds in non-US jurisdictions have risen in sympathy (which we believe is unsustainable, an argument we will leave for another day).

“But as far as the US is concerned, if the Federal Reserve believes interest rates will slow the economy when the opposite is true, then further interest rate hikes will continue to work against their objective. It’s akin to: ‘no matter how much fuel we put on the fire, it simply just won’t go out’.”

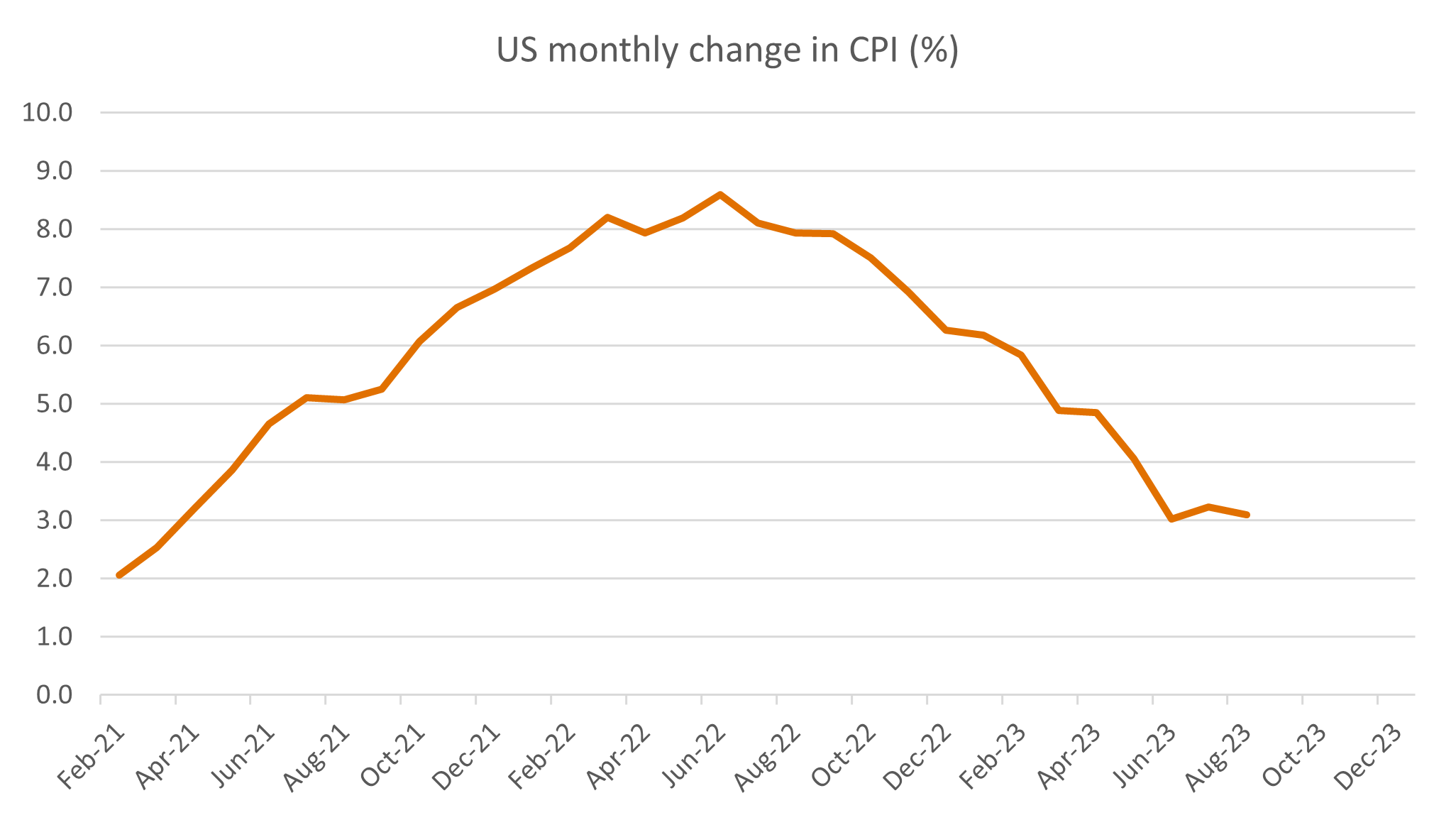

Some thoughts on recent US CPI

“Where does it all end?”

Chris says the light at the end of the tunnel may very well be the in data that kicked it off – US inflation.

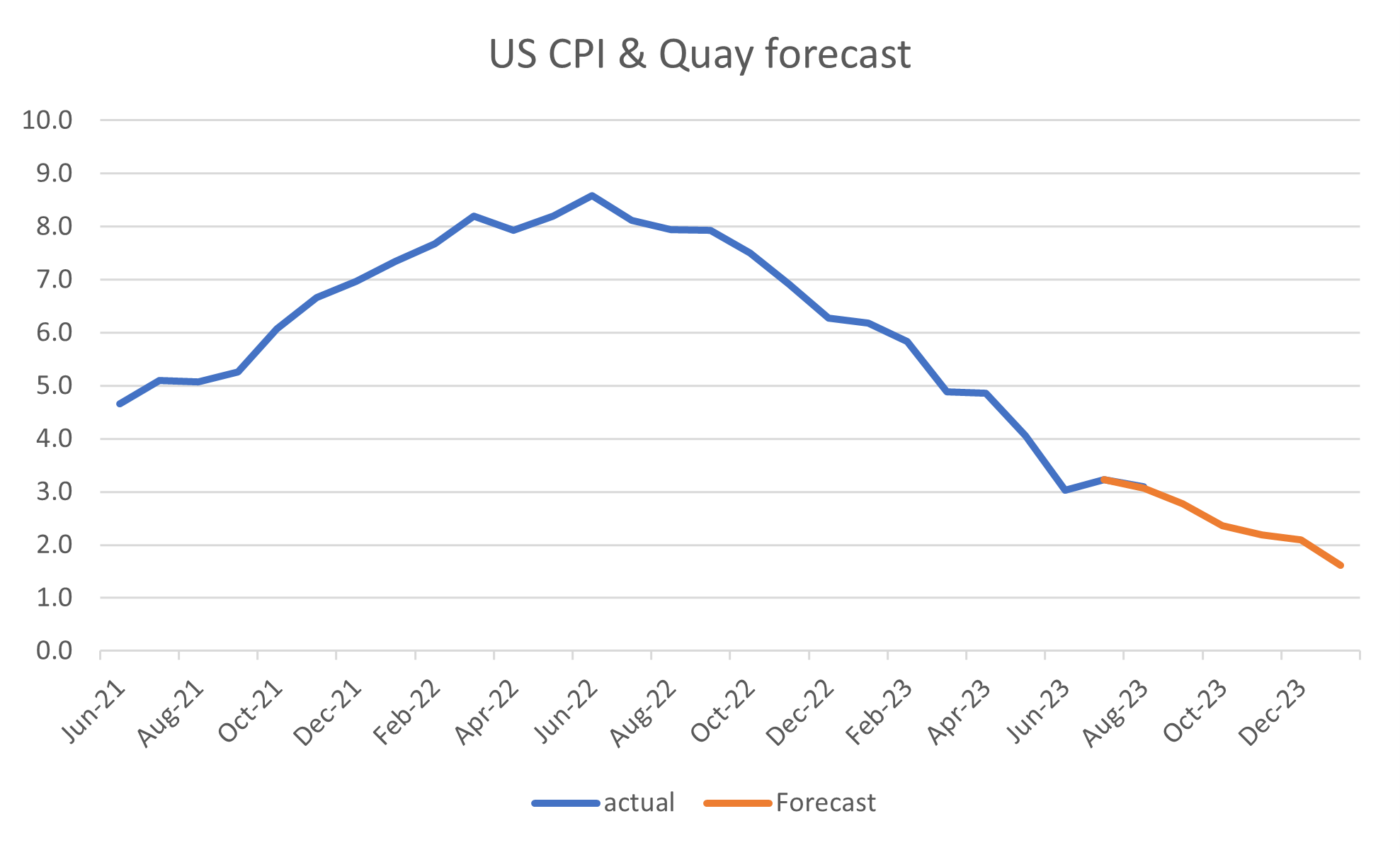

“Over the past year, headline inflation in the US has reduced significantly, from a peak of 8.6% in July 2022 to 3.2% exactly one year later.

“Much of this declaration has had very little support from the shelter component of the data series, however, that is soon to change. Unlike most CPI calculations around the world, shelter costs account for an outsized third of headline US CPI (and around 40% of core CPI). And rent accounts for the majority of these costs.

“Therefore, rent seems like a very important component of the most watched data series this cycle.”

So, calculators out please, and let’s dig in.

Source: BLS, Quay Global Investors

Let’s talk about rent, baby

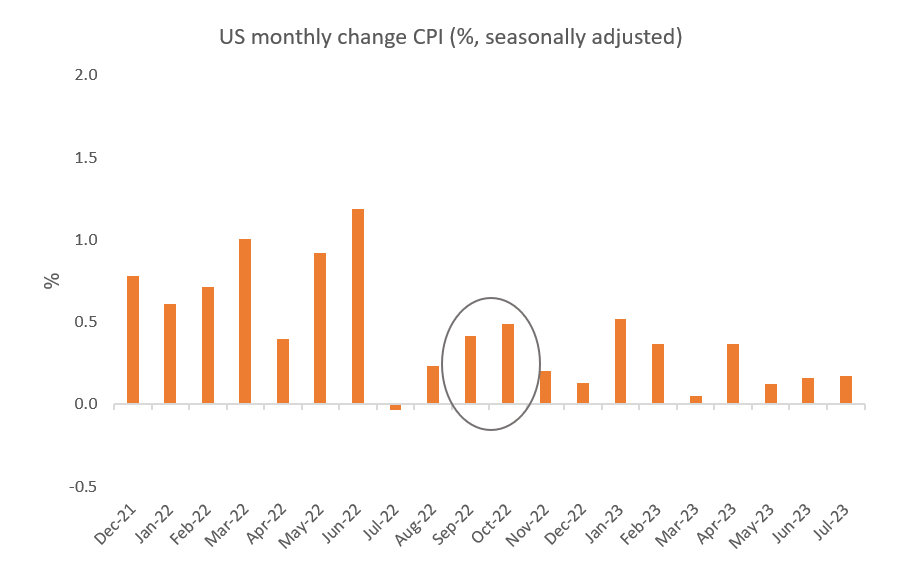

“Since early this year, private sector rental surveys (and publicly listed residential REITs) have reported a significant drop in rental growth since the ’21-’22 boom. And, as expected, annual shelter inflation in the recent CPI has also begun to decline from its peak.”

However, Chris says, in the August CPI release, the monthly rental number “bizarrely re-accelerated.”

“The index for rent rose 0.5% in August, and the index for owners’ equivalent rent increased 0.4% over the month. The lodging away from home index decreased 3.0% in August, its third consecutive decrease.”

Source: BLS, Quay Global Investors

“As shelter makes up 33% of CPI, the 0.44% shelter print accounted for 0.14% of the total 0.16% CPI print. So, ex-shelter, the CPI was barely positive. Given shelter growth re-accelerated in the most recent release, we would expect some give-back next month.”

So, maybe some good short-term news is in the offing, Mr Bedingfield?

“Well. The real question is – and the wider point – why is rental inflation still so high (5.3% monthly annualised) when private sector measures indicate rent growth has recently normalised (and in some areas, actually now recording negative growth)?”

“The fact is the Bureau of Labor Statistics (BLS) measures the price changes in rental leases in such a way that a ‘vintage’ of price effects is captured by the monthly measure – that is, the monthly shelter data includes new rental leases plus past leases. Each monthly CPI release includes 11 months of old rental data plus one month of new rental data.

“The BLS Spotlight on Statistics information page – Housing Leases in the U.S. Rental Market – provides more detailed explanations of this statistical quirk. It also explains why the headline CPI data appears ‘sticky’ – it’s because a very large component of monthly data is backward-looking.

“This ‘lag effect’ is well visualized by the following chart, comparing private sector rental surveys and the actual rental inflation used in the CPI.”

Source: Zillow, BLS, St Louis Fred, Quay Global Investors

In the most recent CPI release, annual rate of shelter inflation of 7.66% is now four months from the March peak (8.18%) and represents 93.7% of the peak rate (7.66%/8.18%).

“In contrast, four months on from peak, the private sector rent data (Zillow/Apartment association) was on average 91% of peak. So, the deceleration from peak for both the CPI and private sector are broadly in line, albeit with the above mentioned lag,” Chris explains.

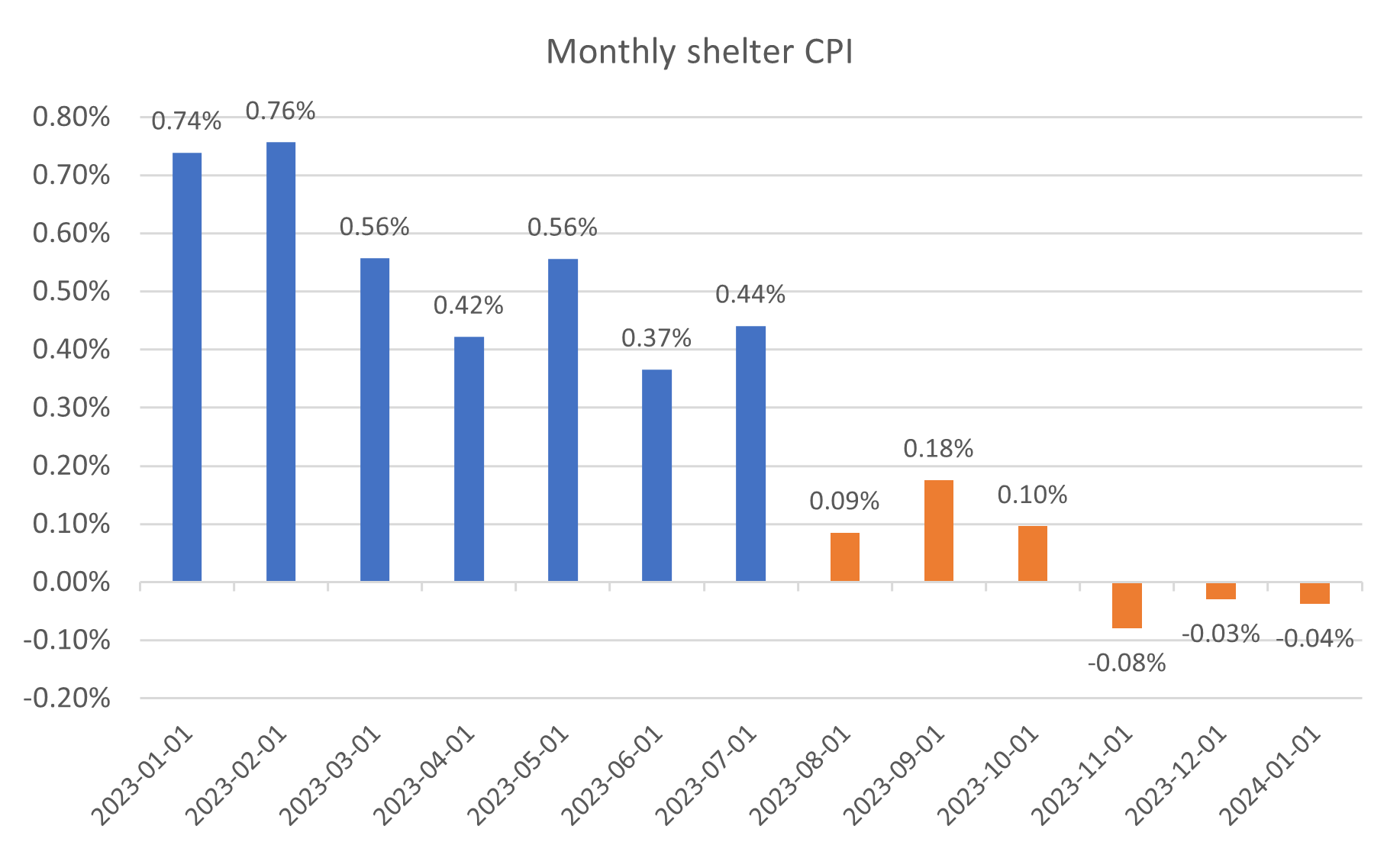

“Assuming the shelter CPI catches up with the private sector rate of deceleration, next month the annual rent inflation will drop from 7.66% to 7.03% (reflecting 86% of peak), implying a monthly rate of just 0.09% (down from 0.44%).

“In fact, since we have almost a year of private sector rent deceleration, we can apply the same ratio to the CPI series and construct a very realistic forecast for the remainder of 2023.

“For example, nine months from peak, private annual rent growth was roughly half of the peak. Assuming the same for the CPI by December, shelter inflation will be 4.1% compared to the March peak of 8.2%.”

Chris says that to get to such an outcome, the implied future monthly CPI shelter component looks like this:

Source: BLS, Quay Global Investors

“Given shelter accounts for 33% of headline CPI (and 40% of core), this data will provide a significant tailwind to the US dis-inflation story.”

Extrapolating the CPI data

“How much of a tailwind? Let’s dig further…”

Up until recently, Chris says the large declines in annual CPI have benefited from the so-called ‘base effect’.

“That is, large monthly CPI data rolling out of the annual series. This ended last month when the July 2022 monthly CPI data (0.0%) was replaced by the July 2023 data (0.2%). Hence, a 0.2% gain in annual CPI.

“This base effect is about to come into play again. After August (where the previous year CPI number was 0.2%) there are some bigger 2022 CPI numbers to roll out in the following months. Specifically, 0.4% in September and 0.5% in October.”

Source: BLS, Quay Global Investors

“As rents decelerate (using known private sector data), and assuming no material change in the non-rent component of the CPI, annual headline US inflation falls to low 2’s by December, and below 2% by January 2024 (as another large CPI number rolls out from the previous year).

Source: BLS, Quay Global Investors

“Of course, this forecast heavily relies on no material change in non-shelter CPI components, in which we have no real expertise. However, for CPI to accelerate from current levels (which some forecasters now expect), these components will need to overcome a significant disinflationary impulse from the known shelter data coming down the pike.”

A final thought

“It has been an interesting year.”

“Despite the fastest pace of interest rate increases in a generation, asset prices are higher (both equities, and residential property), the labour market has remained resilient, economic growth is accelerating (in the US), and inflation is falling.

“Aside from Quay’s regular followers, this might have surprised most. If anything, this underlines our philosophy that macro investing is hard. Even if you get the macro calls right, predicting how investors will react can be even more difficult.”

As always, Chris says that Quay’s team prefers to focus on “good quality companies with demand tailwinds, solid balance sheets and sensible management”.

However, he adds, for those who do focus on the macro, and in particular inflation… “there may be some good news on the horizon.”

The views, information, or opinions expressed in the interviews in this article are solely those of the interviewees and do not represent the views of Stockhead. Stockhead does not provide, endorse or otherwise assume responsibility for any financial product advice contained in this article.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.