PETER STRACHAN: REE prices are rising again, but who’s winning the ASX race to production?

Picture: Getty Images

Peter Strachan is a capital markets veteran, resources analyst and lover of the oil and gas game. The brains behind the popular weekly StockAnalysis investment letter, which launched in 2003, Peter has worked in capital markets for over 35 years, and is a qualified metallurgist and geologist.

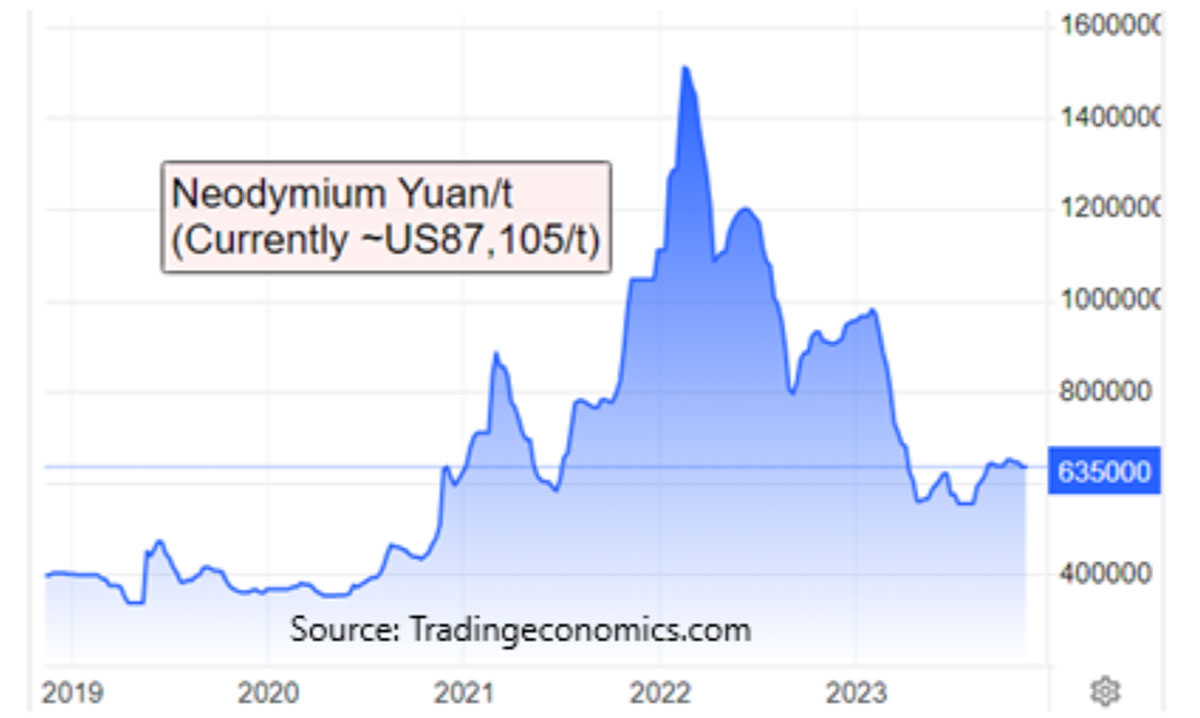

Australian rare earth element producer Lynas Corp (ASX:LYC) reports that through both June and September quarters this year the average price of neodymium/praseodymium oxide was steady at around US$60/kg but averaged US$63/kg through the month of September.

The price of dysprosium saw a steady price recovery from US$257 to US$290/kg quarter on quarter but averaged US$315/kg through the month of September ‘23, while the price of terbium also recovered though the September quarter from an average of US$934/kg to finish through the month of September at an average price of US$1,012/kg, almost reaching the levels seen through the June ’23 quarter of US$1,058/kg.

Lynas reports that demand for Heavy Rare Earths continues to increase, driven by the development of electric vehicles. Dysprosium prices increased rapidly during the quarter as Chinese quotas for Heavy Rare Earths remained flat and exports from Myanmar to China continued to be limited.

Commercial rare earth mineralisation can be divided roughly into two categories. Primary, carbonatite or trachyte hosted monazite mineralisation or weathered, ionic clay hosted REEs.

The Mt Weld REE deposit is a massive, high-grade source of REEs, with a world beating Resource grade of 7.5% total rare earth oxides (TREO).

Hard-rock projects waiting in the wings include Arafura’s (ASX:ARU) Nolans Bore, grading 2.9% TREO, RareX’s (ASX:REE) Cummins Range and Dreadnought’s (ASX:DRE) Yin/C3, both expecting a feed grade of 1% TREO and Hastings’ (ASX:HAS) Yangibana with 0.9% TREO, while Australian Strategic Minerals (ASX:ASM) quotes 0.74% TREO.

Processing hard-rock occurrences can be a complex and bespoke metallurgical puzzle with high hurdle capital costs. Arafura has bumped its initial CAPEX up to $1.7 billion. In NSW, ASM, which has begun by leveraging off its REE refining and processing intellectual property to build a downstream REE metals plant in Korea, sees a spend of $1.1 billion to bring its Dubbo project online.

Processing ionic clay hosted REE deposits, which typically grade 0.07% to 0.13% TREO, is relatively simple and low cost. The flowsheet involves screening out a fine component containing REEs, leaching out the REOs into solution with hydrochloric acid, precipitating impurities and finally precipitating a mixed rare earth carbonate product for sale.

Keys to success are the proportion of high priced REEs recovered the capital and operating costs for each type of mineral assemblage and the value of the final product sent to market. The further that processing moves down the value trail towards magnet metal, the higher will be the price, but also the more capital will be involved to achieve a result.

ASX listed REE developers

Heavy Rare Earths (ASX:HRE) offers substantial leverage to rare earth project development with a market capitalisation of just $5.7 million and about $1.7 million of cash as of 30 September 2023.

The company’s clay-hosted rare earth project at Cowalinya near Esperance in Western Australia has a JORC Inferred Resource of 159Mt grading 870ppm TREO, with an exploration target that promises to be at least twice as large. The project’s REE assemblage is rich in high value elements, with 28% of the metals in the magnet rare earth category. Metallurgical recovery test work on composite mineral samples from Cowalinya shows high leachability of the magnet rare earths, averaging 82.9% recovery with low acid consumption, averaging 18.1kg per tonne for most samples.

In the Northern Territory, approximately 50km northwest of Tennant Creek, historic drill chip and soil sampling at HRE’s 100% owned Duke project shows potential for a large saprolite-hosted rare earth deposit, like the Cowalinya deposit.

Over coming months, investors will be able to come to grips with the value proposition that evolves from HRE’s efforts to wrap numbers around estimated costs and sale value for a proposed REE concentrate.

Processing mineralised clay samples from Victory Metals’ (ASX:VTM) North Stanmore deposit near Cue in Western Australia has produced a mixed rare earth carbonate (MREC) containing 12.46% TREO made up of 96.4% valuable heavy REEs, including dysprosium and terbium, with an indicative basket price for MREC of A$114/kg, along with by-product copper, cobalt, and nickel.

Victory estimates a Mineral Resource at its Cue tenements of 250Mt grading 520ppm TREO with an Exploration Target of over 700Mt containing 33% of the more valuable heavy REEs. The project is well located in a mining region of Western Australia, with access to skills and transport infrastructure. Planned exploration and ongoing metallurgical processing work should lead to feasibility work, illuminating capital and operating cost estimates for the $18.6 million company with $3 million of cash on 30 September ’23.

With a market cap of $401 million, Arafura Rare Earths’ Nolans Project in the Northern Territory, north of Alice Springs, is one of the most mature undeveloped REE projects in Australia. The project is expected to produce 4,400 tpa of NdPr oxide plus 144Ktpa phosphoric acid and 474 tonnes other HRE oxides over a mine life of 38 years, delivering an EBITDA of $573 million pa, once in production post 2027.

The company is well advanced on early works at the main processing site, road access, accommodation camp and water supply and is making progress on final engineering design for its hydrometallurgical processing plant. Final funding for the estimated $1.7 billion project is progressing with ~$1.2 billion of debt in the wings for H1 ‘24, with main construction activity to follow through 2025/26.

With a market cap of $20.5 million and cash plus investments valued at ~$7.6 million, RareX has a tiger by the tail at its 100% held Cummins Range REE and phosphate project in the East Kimberley region, south of Halls Creek in Western Australia. The project has a global resource of over 500Mt but plans to process an initial 31.7Mt grading 0.7% TREO plus phosphate content.

The company plans a staged development of this battery and fertiliser materials project, initially investing $45 million to mine 250Kt pa of direct shipping, high grade rock phosphate from 2025, for which it has a ready, local sales off-take agreement for a product that offers very high bioavailability of phosphate for direct application fertiliser.

After two years of this effective pre-strip operation, the project will need $304 million to build a processing plant that will produce both a phosphate concentrate for fertiliser and LiFeP batteries and a REE concentrate for sale from the Port of Wyndham, commencing in 2027.

The company’s feasibility work estimates an after tax NPV of $333 million, which compares favourably with its current enterprise value of $13 million.

The views, information, or opinions expressed in the interviews in this article are solely those of the interviewees and do not represent the views of Stockhead. Stockhead does not provide, endorse or otherwise assume responsibility for any financial product advice contained in this article.

At Stockhead, we tell it like it is. Arafura Rare Earths, RareX, Hastings Technology Metals, Heavy Rare Earths and Victory Metals are Stockhead advertisers.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.