MoneyTalks: There’s a commodity party and even lithium’s invited

Via Getty

MoneyTalks is Stockhead’s regular drill down into what stocks investors are looking at right now. We’ll tap our extensive list of experts to hear what’s hot, their top picks, and what they’re looking out for.

Today we hear from James Gerrish, lead author at Market Matters and PM at Shaw and Partners.

James tells Stockhead the game’s not done yet, despite the fact weakness across the lithium sector has lost its place in the financial press in the wake of rallying copper and gold stocks.

“Usually, more ‘clicks’ are achieved from bad news and crash-style stories, but the lithium bear market has grown old in the tooth. However, as we’ve seen with other commodities and related stocks, this year is starting to look exciting for the commodity space, and we believe lithium can join the party, at least for a while.

“We aren’t as bullish towards lithium as copper, for example, with the supply & demand dynamics far from clear, but we can see them enjoying a strong finish to this FY.”

James believes that from a risk/reward perspective, there’s room for a similar advance in the relatively near future after lithium enjoyed a small “squeeze” like move in early March.

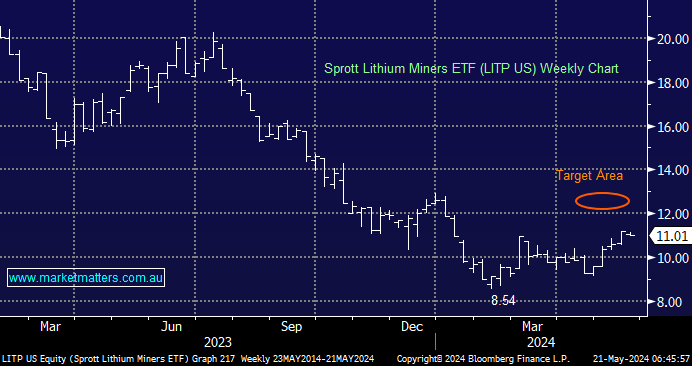

Since our early April, when Market Matters identified the opportunity, James notes that the Lithium ETF (LITP US) has advanced ~9%.

“Halfway to our $US12 target area. So far, so good. However, the stocks in the ETF have experienced a mixed performance.

“As of Tuesday morning in Sydney, the major five holdings are Mineral Resources, Pilbara Minerals, Albemarle (ALB US), Sociedad Quimica, and IGO (ASX:IGO), in an industry where Australian miners play a major role.”

About six weeks after Market Matters first posed the question – “Are lithium stocks about to pop on the upside?” James and his crew revisit three lithium plays and a Sprott ETF.

“We remain short-term bullish towards lithium miners, initially targeting ~8-10% upside from current levels.”

However, James says he remains highly conscious that the sector is hostage to the underlying lithium price, which Goldman Sachs reckons won’t bottom out until 2025.

“One of the reasons MM’s portfolios performed strongly in 2023 was that one of the core views was to step aside from the lithium miners; we have since reversed this stance and bought a number of plays into the sharp sell-off in early 2024,” James says.

Sprott Lithium Miners ETF (LITP US)

MM remain bullish towards the LITP ETF around the $US11 area.

Pilbara Minerals (ASX:PLS) $4.20

MM is long and bullish towards PLS in the short term

“We have followed PLS closely over the last 6-months, especially since we went long in mid-January.

“PLS is our preferred local pure lithium play, which comes with the added spice of over 21% of the stock being held short; a ‘short squeeze’ up towards $5 is easy to visualise if/when the weak traders start to capitulate.

“The company remains our preferred exposure in the volatile space, although it is unlikely to either ascend or descend as fast as many. This is a proven miner that turns a profit and pays a dividend, which should continue to cushion moves if weakness persists in the underlying lithium price. Over 20% of PLS is held short, which is both exciting from a squeeze perspective but also a concern because professional traders are betting against the stock/sector.”

“We can see PLS trading between $3 and $5 into 2025 and will act accordingly — MM is long PLS in our Active Growth Portfolio.

“This is a position that’s likely to be more active than some, and we won’t be adverse to selling it if it does squeeze higher.”

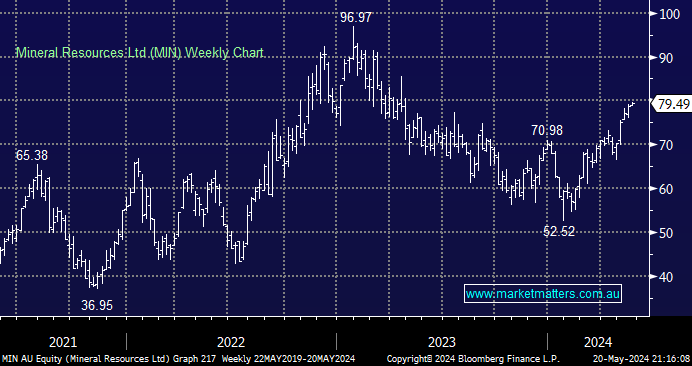

Mineral Resources (ASX:MIN) $79.49

MM remains bullish, and long MIN

“MIN is a two-commodity play, with a combination of lithium and iron ore driving the miner (along with a mining services division).

“Both have been on the nose since early 2023, but we are now seeing signs of a bottom for both, although how far they can/will bounce is a tougher call.

“The stock has already bounced almost 40% from this year’s low, but we’re not considering fading the move just yet, although if we do see a test of $80, we will be considering taking at least part profit.

“We have been patient with MIN, and as iron ore and lithium start to warm, we can see a test of $80 this FY – MM is long MIN in our Active Growth Portfolio.

“We have looked at MIN regularly throughout 2024, and the miner is currently enjoying a strengthening iron ore space as China stimulates its economy and a bounce in lithium prices, albeit from depressed levels. The moves in the respective commodities have propelled MIN over +50% higher from its 2024 low, scaling fresh 12-month highs in the process.

“The company remains our preferred exposure in the volatile space, although it is unlikely to either ascend or descend as fast as many.

“This is a proven miner that turns a profit and pays a dividend, which should continue to cushion moves if weakness persists in the underlying lithium price.”

“We can now see MIN testing $90 as iron ore and lithium gain further traction.”

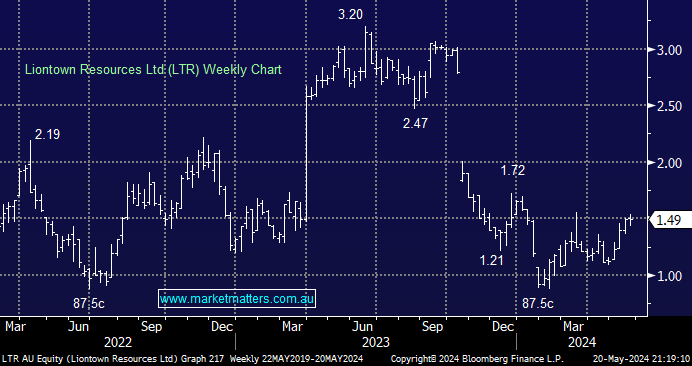

Liontown Resources (ASX:LTR) $1.49

MM is bullish toward LTR short-term

Lithium miner LTR is a lithium play with a twist, James reckons.

“It includes a short position of over 10%, which we believe is brave by all concerned, considering the previous and potential corporate activity; it was only a year ago that the stock was in play at $3!

“Gina (Rinehart) has a more than an 18% stake in the battery metals producer, making her an obvious candidate for a bid following Albemarle’s (ALB US) failed attempt in mid-2023.”

“That drama is why LTR has been regularly in the news over the last few years… from a failed/blocked $6.6bn takeover bid from US giant Albemarle to the significant stake taken by Gina and subsequent speculation whether she will consider a full takeover bid.”

“Either way, we believe the risk/reward looks great for active investors/traders around current levels and believe LTR is likely to test its recent swing high of ~$1.7, around 15% higher.”

The views, information, or opinions expressed in the interviews in this article are solely those of the interviewees and do not represent the views of Stockhead.

Stockhead does not provide, endorse or otherwise assume responsibility for any financial product advice contained in this article.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.