MoneyTalks: The hour has come for Regis, Resolute, Paladin and Bannerman

Start your engines. Via Getty

MoneyTalks is Stockhead’s regular recap of the ASX stocks, sectors and trends that fund managers and analysts are looking at right now.

Today we hear from Fairmont Equities managing director Michael Gable.

Michael says his team have been bullish on resources for a while now.

“If you follow our work over at Fairmont, you’d know well we’ve been particularly bullish on gold, copper, and uranium.”

He says, while the number of pure play copper stocks on the Australian market is “fairly limited.”

“There are, nevertheless, plenty of gold stocks to choose from. And when it comes to uranium, I believe that the upside from here is immense.”

“So, I propose, we take a look at what is happening with gold and uranium, and I’ll describe a few local stocks which we believe, should do extremely well from here.”

Gable’s Gold

Last year gold was getting bought up heavily by central banks around the world with China being the major player, Michael tells Stockhead.

“At the time, it was sitting under a major resistance level which was just under US$2100/ounce. It was on the cusp of a major breakout, and it was only a matter of time until it got moving. We finally got that breakout at the start of March and it has been on a great run since then. If inflation stays high, gold will be bought.

“If interest rates start to head lower, gold will be bought.

“Central banks are still buying gold so there are plenty of reasons to stay long. Even from a technical point of view, this recent breakout, when viewed on a longer-term chart, is only the start of the move.

“When it comes to stocks, Michael says he’s have a found a couple of smaller producers which are still in either the base forming stage, or are consolidating back near their lows.

“Upside breaks from a large bases and sideways consolidations can lead to big moves.”

Resolute Mining (ASX:RSG)

“RSG is an African focused producer,” Michael tells Stockhead. “Its market cap is still just under $1bn but that looks set to rapidly increase from here.”

“The company is unhedged and can capture the future upside in the gold price.”

“The average analyst target is over 70c, and although I don’t usually agree with analysts, I can see that being easily achievable based on the share price chart.”

In March 2023, RSG shares had a solid run on very high volumes.

“Since then, they ‘ve consolidated sideways on lower volumes. This is a bullish sign and usually means that a stock is getting ready to make the next big move.

“Recent trading in the shares are indicating to me that it is nearly ready for that move. I can see resistance here at 50c… A break above that would have me targeting levels near 80c.

“A more bullish case, using some Elliott Wave theory could see numbers closer to $1.20 by year end.”

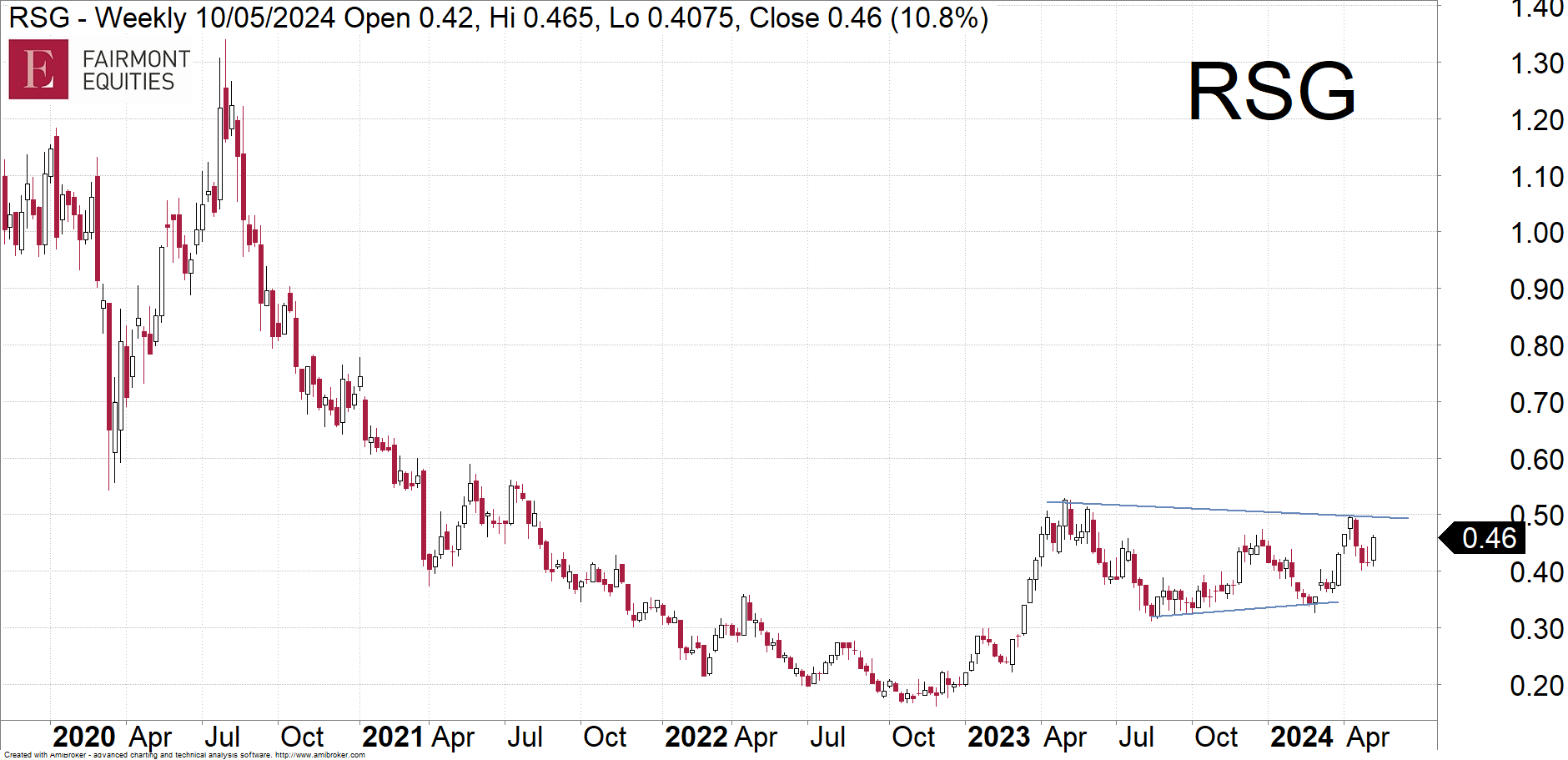

Regis Resources (ASX:RRL)

“RRL looks very exciting to me because it has been forming a large base for over two years now. Remember, the bigger the sideways move, the bigger the breakout,” Mike says.

“This Aussie gold producer has recently approved the development of two more projects. It is also unhedged and therefore can capture the future upside in gold.

“I can see RRL moving up towards the top of its base, which is near $2.50. A break above this base would give a technical target near $3.50 as a minimum.”

You and Uranium

Uranium is the next big trade in Mike’s opinion.

“We had lithium a couple of years ago, and Buy Now Pay Later before that. But this one could eclipse both of them.

“Uranium is in short supply due to a decade of underinvestment, and we now have demand picking up substantially.

“The sector will remain in deficit for years to come and so will the supply response. Until then, uranium prices will head higher and share prices will follow.

“Uranium got quite a bit of attention earlier this year when the spot price spiked higher, but it has fallen off many people’s radar. Despite the US recently passing legislation in the senate to phase out Russian supplies, it is still not grabbing the headlines.”

Mike says this is short-memory stuff is exactly what we want to see, because share prices are climbing higher under the radar.

“Like the previous big trades before it, stock prices front run what will happen in the future, then it starts to get people’s attention.

“Big investors pile in, analysts start upgrading numbers, retail investors get hold of it, the story hits the front pages, and you get a FOMO rally taking share prices probably higher than where they need to be.

“We are yet to see this play out, which is why I am very excited to see how the rest of the year pans out.”

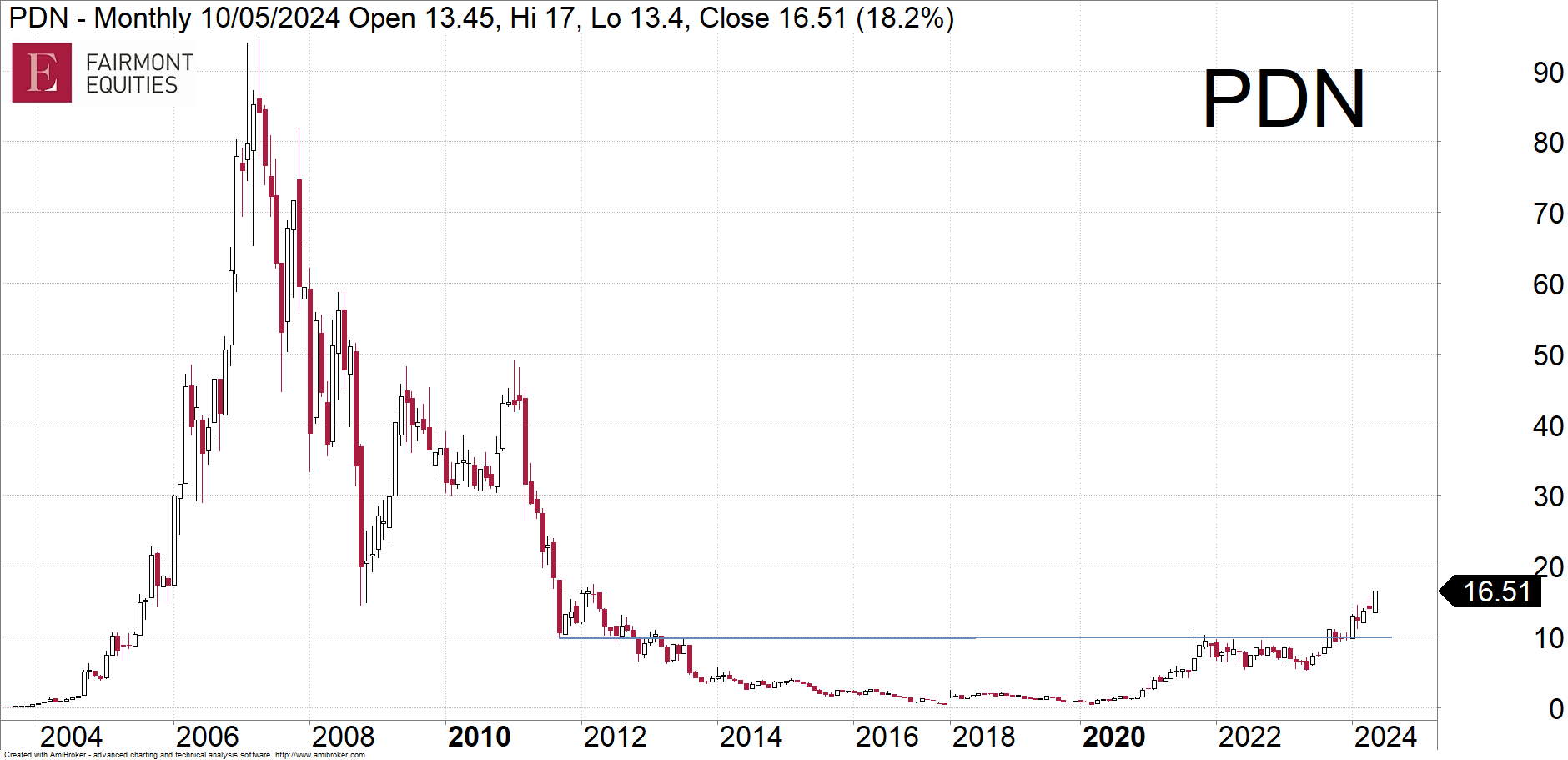

Paladin Energy (ASX:PDN)

PDN is the top of Michael’s list in playing the uranium trade.

“They are in production again, have a track record, and get the most coverage from the big analysts.”

He says that earlier this year spot prices rallied and PDN stock was pushing beyond $10 (adjusted for the recent share consolidation).

“It then cooled off and investors were asking me if the move was over.

“Well, I just pulled out my monthly chart of PDN – which, by the way, I carry around with me in my back pocket. I took it out, patted it gently and said – The answer is ‘no, this thing has only just started’.

“If a stock like RRL looks bullish for spending two years forming a base, then have a look at PDN. It has built a base for over 10 years. The recent 50%+ rally since the start of the year is a mere pimple on the chart.”

Michael says, if this breakout is the real deal – and he thinks it is…

“Then we have quite a bit more upside from here over.

“I am looking at PDN to move multiple levels higher from where we are right now.”

Bannerman Energy (ASX:BMN)

BMN is not producing yet Mike says, but has one of the largest undeveloped uranium mines in the world around the corner from Paladin’s mine in Namibia.

“Usually when a commodity price takes off, it’s the smaller quality stocks that have more leverage to the upside.”

BMN is in this camp for Michael.

“The overall chart looks similar to PDN which is why I like it, but it has greater upside potential over time.

“Like PDN, this breakout has only just started.”

The views, information, or opinions expressed in the interviews in this article are solely those of the interviewee and do not represent the views of Stockhead.

Stockhead does not provide, endorse or otherwise assume responsibility for any financial product advice contained in this article.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.