Guy on Rocks: Gold’s on the rise, and this ASX junior has a titanic resource, coming in cheap

Picture: Getty Images

‘Guy on Rocks’ is a Stockhead series looking at the significant happenings of the resources market each week. Former geologist and experienced stockbroker Guy Le Page, director, and responsible executive at Perth-based financial services provider RM Corporate Finance, shares his high conviction views on the market and his “hot stocks to watch”.

Market Ructions: REE tensions re-emerge

There appears to be a sense of optimism in the junior space at the moment with a view that most of the “value destruction” is behind us and volumes starting to improve.

Global markets responded favourably to a drop in inflation to 2.97%, compared to 4.05% last month and 9.06% last year. Federal Reserve Chairman Jerome Powell indicated a few weeks ago that there are likely to be another two 25 basis point interest rate rises before year end, however the recent inflation numbers would suggest an imminent pause in rates.

I have heard it many times before that nobody rings a bell at the bottom of the market however I did stand on the corner of Hay Street and Emerald Terrace in West Perth and rang the bell on Friday, so clearly that old wives’ tale is fake news.

Precious metals had a good week with gold closing up US$35 to finish the week at US$1,955/ounce on the back of a big drop in the USD with the DXY down a whopping 300 basis point to close at 99.959, its biggest weekly move since November last year.

US 10-year treasuries were off 30 basis points to 3.76%. Silver also had a very good week closing up almost 8% to US$24.87/oz. Platinum finished the week up 6.5% to US$970/ounce while palladium which has been heavily sold off over CY 2023 and recently posted a four-and-a-half week low. It ended the week up US$24/ounce or 2% to US$1,246/ounce.

Axel Merk, president and chief investment officer at Merk, recently stated in a recent Kitco interview that despite the near-term selling pressure on gold, he thought the yellow metals was performing well in a challenging economic environment. Notably gold is still up US$200/ounce from its October 2022 lows.

Merk said he is not convinced that the Federal Reserve will be able to get inflation under control before it breaks something in the economy or financial markets. Looking at the inflation threat, he added that with so much debt in the system, there is very little political will to bring inflation down.

Copper (figure 1) closed the week at US$3.89/lb for a 3% gain after a sell-off on Friday but remains in a strong 3 cent contango for the three-month futures contract with warehouse levels remaining very low (figure 2).

Energy prices have also continued to tick up. WTI closed at US$75.20/bbl (after trading above US$77/bbl on Thursday) for a 2.1% gain for the week. 14% fewer rigs were operating this week and US inventories remain at low levels as exploration funding becomes increasingly difficult under the Biden administration as their war on fossil fuels rolls on.

Brent crude oil (figure 3) is heading for its longest run of quarterly losses over the last 30 years over concerns of softening demand.

Drilling activity in the state of California has plummeted with only seven drill permits approved this calendar year compared to 200 YTD in the corresponding period in 2022.

According to the Mercenary Geologist Mickey Fulp there are 1,400 drilling permits delayed or in process in the great state of California.

While base metals have been soft over CY 2023, largely in response to disappointing economic news from China, it appears the Chinese have around US$3 trillion in foreign exchange reserves which, according to Brad Setser, a former US trade and treasury official, are not reported in the books of the People’s Bank of China.

These funds appear as ‘shadow reserves’ in the assets of other entities like state commercial lenders and policy banks. These foreign reserves, according to Setser, have likely increased with China’s growing export surplus.

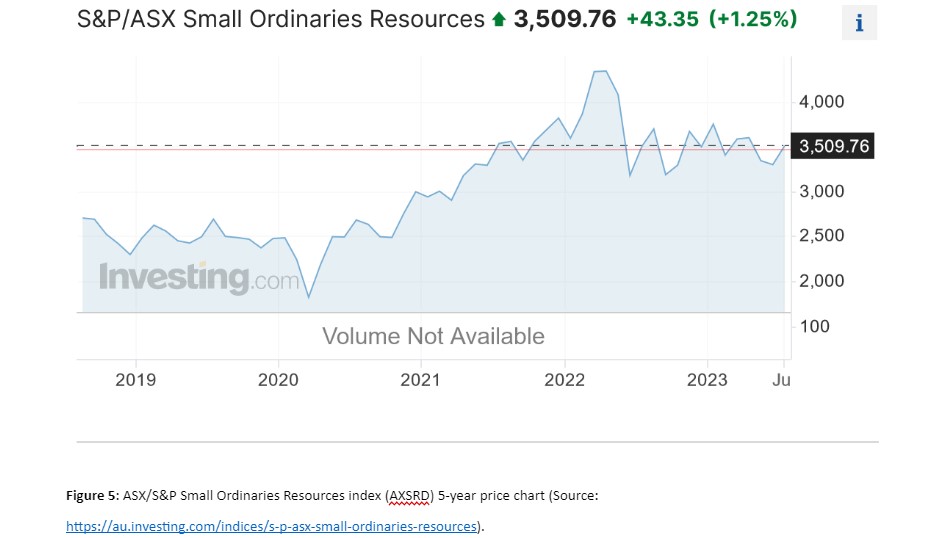

The TSX-V (figure 4) in Canada appears to be bouncing off the bottom on the back of a long period of low volumes around 15m shares per day but remains off 12% over the last five years compared to the S&P/ASX Small Ordinaries Resources Index (figure 5) which is up just under 20% over the same period.

Geopolitical tensions are again in focus as China’s Ministry of Commerce earlier this month announced restrictions on exporting gallium and germanium which are key parts of the semiconductor, telecommunications and electric vehicle industries. It will be interesting to see if similar restrictions are placed on other rare earths such as neodymium and praseodymium which are predominantly used in magnets used in high-tech applications.

China accounted for 70% of world rare earth production and 85% of the world’s processing capacity in 2022. It seems there is some urgency for the emerging rare earths sector to get its act into gear which will mean sorting out the metallurgy around the processing of clay-hosted rare earths.

Finally iron ore was up over 4% on Friday to close at US$114/tonne (figure 6) despite slowing steel production which fell 7.3% YoY in May, while apparent steel consumption fell 5.1% YoY.

Iron ore stocks at the 45 major ports in China declined by 0.80% week-on-week to 126.4Mt with iron ore volumes among 64 steel mills fell for the second week in a row by 2.5%.

Macquarie remains bearish on iron ore with supply outpacing demand as we move into 2024 with iron ore forecast to fall to US$100/t by Q4 (figure 7). This was qualified by the fact that much of this supply is coming from a handful of projects and is dependent on timely ramp-ups.

New Ideas: Big resource upgrade for Titan Minerals

The Peter Cook-chaired Titan Minerals (ASX:TTM) (figure 8) made a big splash last week coming out with a JORC Resource upgrade to 43.54Mt at 2.23g/t Au and 15.7g/t Ag for 3.12 million ounces of gold and 21.98 million ounces of silver from its Dynasty project (figure 9).

The project covers around 14,000ha in Ecuador with the JORC Resource comprising mostly epithermal mineralisation likely associated with a nearby porphyry. Importantly the resource contains a high-grade core of 17.3Mt @ 3.77g/t Au, 24.0g/t Ag for a contained 2.09 million ounces of gold and 13.33 million ounces of silver.

The other positive is that over half of this JORC Resource lies within 100m of surface. The previous JORC resource stood at 2.1 million ounces of gold and 16.8 million ounces of silver.

From the July 6 ASX announcement, it appears TTM intends to continue with an aggressive exploration program over its 9km footprint (figure 10). Trenching and drilling is also planned at Papayal and Trapichillo prospects where the company had previously identified multiple vein sets exposing high-grade gold and silver.

Regional mapping and gradient-array IP surveys to assist in the mapping and drill targeting of sulphide-rich veins are also planned.

At an EV of just under $100 million the stock is trading at an enterprise value of just under $30/ounce with plenty more in the tank by the look of it. The stock may well come back after the spike last week but under 10 cents it looks cheap in a sector that continues to trade at a discount.

At RM Corporate Finance, Guy Le Page is involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting, and corporate advisory roles.

He was head of research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July 1998. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada, and the United States. The views, information, or opinions expressed in the interview in this article are solely those of the interviewee and do not represent the views of Stockhead.

Stockhead has not provided, endorsed, or otherwise assumed responsibility for any financial product advice contained in this article.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.