Guy on Rocks: Caruso-led, with leverage that’s ‘nothing short of spectacular’ – this fat lady’s just warming up

‘Guy on Rocks’ is a Stockhead series looking at the significant happenings of the resources market each week. Former geologist and experienced stockbroker Guy Le Page, director, and responsible executive at Perth-based financial services provider RM Corporate Finance, shares his high conviction views on the market and his “hot stocks to watch”.

Market Ructions: Gold

Gold closed last week up 2% to US$2,390/ounce and appears to be struggling to break through and hold US$2,400 before drifting back to US$2,309/ounce by mid-week.

Gold has traded in a US$100 range in just over a few days!

Silver had another strong week up 2.3% to finish at US$28.6/ounce while platinum and palladium were softer.

Platinum finished down US$45 to US$930/ounce while palladium closed at just over US$1,012/ounce down US$31 for the week before a sell-off on Monday to US$990/ounce, down US$22 for the day.

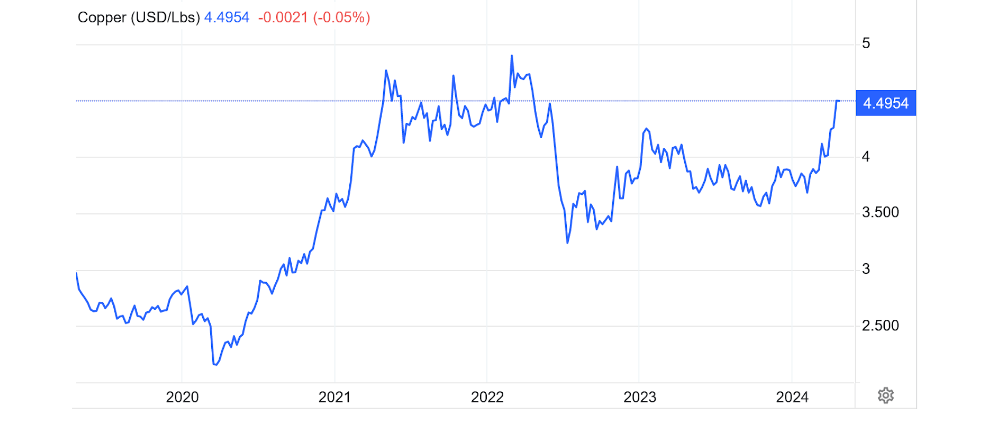

Copper soared last week 5.5% US$4.42/lb funds piled in for a 22-month high. Again, supply side concerns have seen copper soar in recent weeks with CODELCO projecting that production this year will come in at a 20-year low.

Morgan Stanley (April 2024) also cite a reinvigorated demand narrative on mid-term power grid upgrades/data centre requirements, as well as improving near-term China data as providing further tailwinds to the copper price and are estimating market deficits of 700kt/300kt/240kt in 2024/2025/2026.

Flight to safety however not necessarily into the US dollar with the DXY up 12 basis points to close at 106.14.

Some of the heat has come out of the middle east as the protagonists have gone back to the neutral corners. The Mercenary Geologist Mickey Fulp likens this to touch football.

WTI closed at US$83.24 off 4% for the week sliding below US$81/BBL by mid-week.

Rigs in the US were up 2, production was flat at 13.1MBOPD and inventories climbed +2.8MBBLS.

Imports remained flat at 6.3M BBLS and oil refineries were at 15.9MBOPD representing a 15-year high.

Gasoline in the US was up another 4 cents averaging US$3.63 gallon with Joe Biden again threatening to release more oil from the strategic reserve.

His latest fever dream was to restrict new oil and gas leasing on over 5 million hectares of a federal reserve in Alaska to help protect wildlife such as caribou and polar bears.

This follows on from the Biden administration’s earlier decision to reject an application for a 338km road into the northwest region of Alaska to open up various critical mineral deposits. The area is dotted with copper, cobalt, zinc, silver and gold deposits.

Uranium was steady at US$89/lb, steady after the last few weeks.

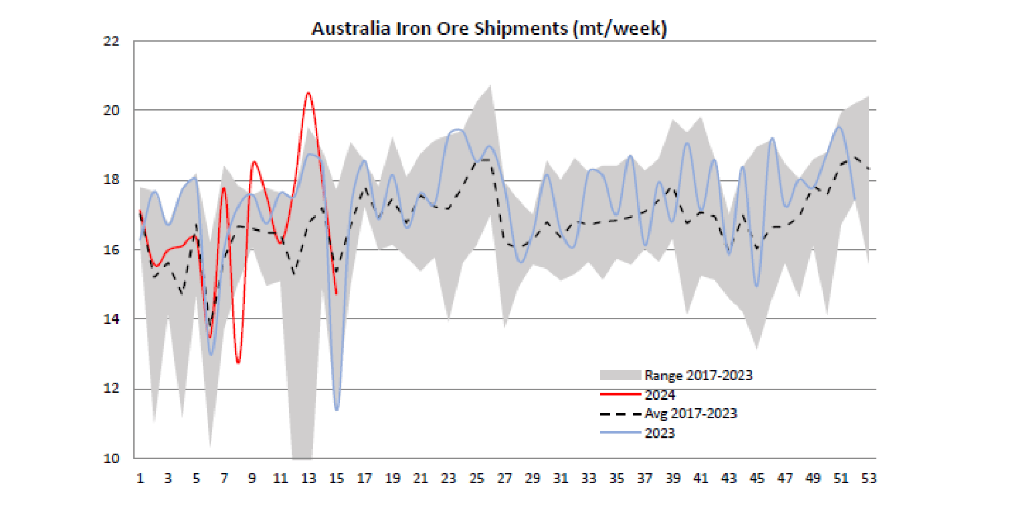

A 28% drop in Australian iron ore shipments (~6Mt – figure 4) since end-March has helped keep iron ore prices above US$100/tonne with cyclone Olga resulting in the closure of Rio Tinto’s Dampier and Walcott ports driving shipments down 52% in just two weeks.

BHP’s quarterly iron ore output also dropped 7% quarter on quarter with adverse weather contributing to the decline.

Meanwhile steel exports ex China were up almost 30% over March at 9.2Mt, their highest levels since June 2016.

New Ideas – The (potentially) Magnificent Caruso

Everest Metals Corporation (ASX:EMC) (figure 6) is a junior resource company headed by industry veteran Mark Caruso with a portfolio of exploration/developments in Western Australia.

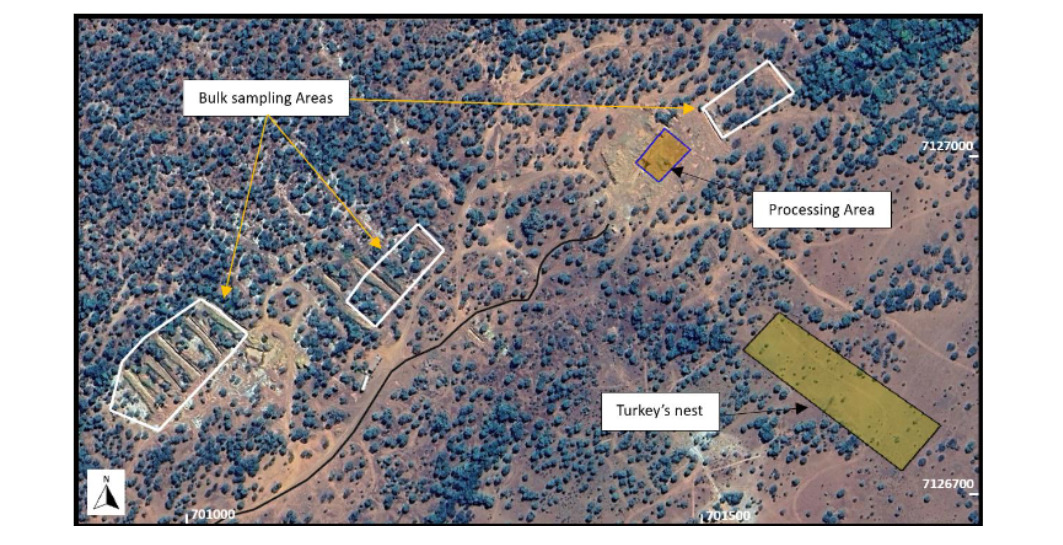

The Revere project (figures 8, 9 and 10) looks like a near-term gold development story and is situated just off the Great Northern Highway around 90km northeast of Meekatharra in the (Murchison, WA). The bulk sampling, which is scheduled to take around six months, should give greater confidence ahead of a JORC Resource late 2024/early 2025.

The company also has some near-term production potential at the Mt Dimer Taipan Gold Project that contains a JORC Resource of 48,545oz @ 2.1g/t Au and 89,011 @ 3.84 Ag on a granted Mining Lease. A development submission is due to be submitted in 2Q 2024.

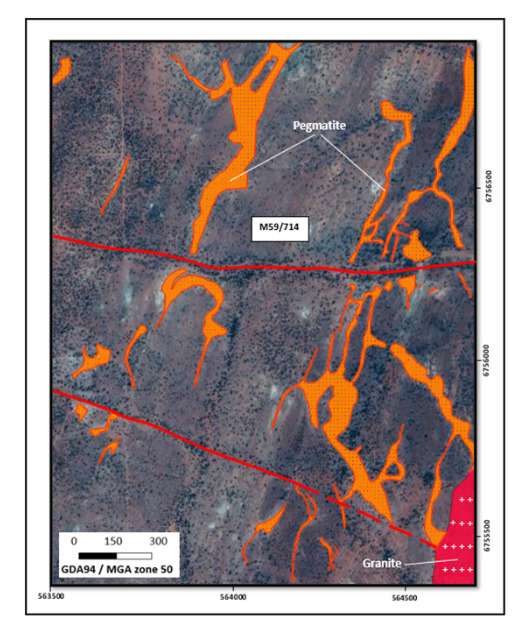

While both Revere and Mt Dimer have the potential to generate medium term cash flow at solid margins, I was somewhat intrigued by the Mt Edon Critical Mineral Project (figure 10) where a phase 11,200 metre RC program on the granted mining lease is scheduled to commence in the June Quarter.

High grade rubidium mineralisation is associated with irregular shaped felsic rubidium rich pegmatites that have intruded into a sequence of mafic, ultramafic, and sedimentary rocks.

A resource drilling program is scheduled for early June 2024 with a view of converting the Exploration Target (JORC 2012) of 3.2 to 4.5 million tonnes @ 0.23% to 0.35% Rb2O and 0.08% to 0.12% Li2O into a maiden Mineral Resource Estimate.

Mineralogical studies as part of an MOU with the ECU Mineral Recovery Research Centre are exploring methods for rubidium and potentially lithium extraction. This includes ore beneficiation and rubidium extraction from the concentrates designed to produce refined rubidium components notably salt, and metal.

The flowsheet is also reviewing options for purification and refining with the goal of producing a rubidium salt and metal.

It is early days at Mt Edon and too early to call but I would have thought a reasonable outcome would be to produce a rubidium (carbonate) concentrate as a base case if the ECU work failed to produce rubidium salt and metal?

An 80% recovery and 65% payability on a 100,000 tonnes @ an average grade of 0.30% could produce around 240 tonnes per annum, which would equate to payable metal of around US$150 million per annum with potentially very low capital and operating costs.

While the rubidium market (used in photocells among other things) is small at around 2.5 tonnes per annum, it is projected to grow to just under 4 tonnes by 2030. My limited research would suggest that if more could be produced, there is a reasonable chance the market could absorb more.

Given Mark Caruso’s background in mining, civil engineering and mining contracting I have a reasonable degree of confidence that the company can pull off not only the small-scale gold mining, and if the studies come in, the Mt Edon project. If the company gets this right, the leverage could be nothing short of spectacular.

Rest assured, if this chestnut comes in, I’ll be singing like that famous opera singer that all the Stockhead faithful would be familiar with, Enrico Caruso, or ‘the Magnificent Caruso’ as he is better known. At Cigar Social for some time to come…

Like Enrico, we both came from very humble beginnings…

Guy Le Page is a director and responsible executive at Perth-based financial services provider RM Corporate Finance. A former geologist and experienced stockbroker, he is involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting and corporate advisory roles.

He was head of research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July 1998. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada, and the United States.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.