Guy on Rocks: A cheap copper stock to help keep the family together in Business Class

Just another day in Peppermint Grove watching the portfolio perform together. Picture: Getty Images

‘Guy on Rocks’ is a Stockhead series looking at the significant happenings of the resources market each week. Former geologist and experienced stockbroker Guy Le Page, director, and responsible executive at Perth-based financial services provider RM Corporate Finance, shares his high conviction views on the market and his “hot stocks to watch”.

Market Ructions: Iron ore bounces back

A reasonably flat week on the precious metal front with gold up US$6/oz to close at US$1755/oz, up with silver up 2.5% to US$21.44/oz. Platinum was also quiet, up US$6.0/oz last week while palladium was the big mover down 5% to US$1779/oz.

The overall mood was a little more subdued with the VIX (volatility index) back to 20.5 (after touching 30) closer to longer term means of around 18-19. The US dollar index was down 1% to 106.03 for the week with the 2–10-year inversion of treasuries now at 75 basis points (near on a 20-year record spread) which implies the market has already factored in a recession.

As the Stockhead faithful are well aware, the definition of a recession in Western Australia is where the kids travel Economy on the Canadian ski trip rather than Business Class. Not that anything like this has ever happened in living memory of course…

After spending most of the year in backwardation, copper futures finally moved into contango spurred on by continuing low inventories as well as supply side issues with workers going on strike at the giant Escondida copper mine (controlled by BHP) on 21 and 23 November due to labor demands. In 2017 the strike lasted 40 days. Chinese demand still appears tepid with copper ore and product imports, according to Morgan Stanley (23 November 2022), down 21% month-on-month and 1% year-on year.

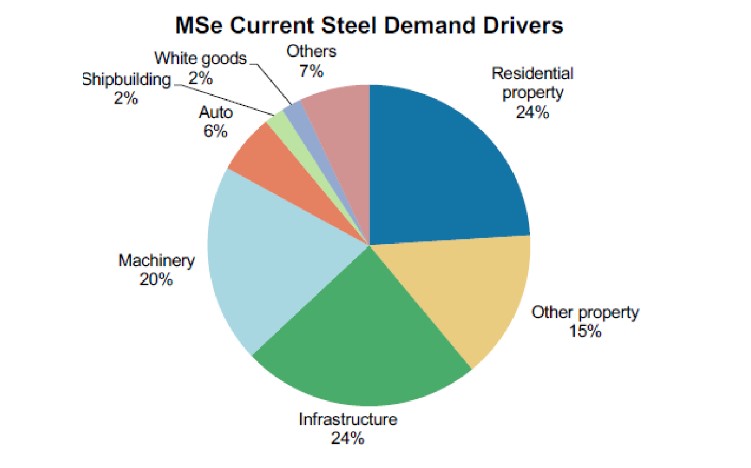

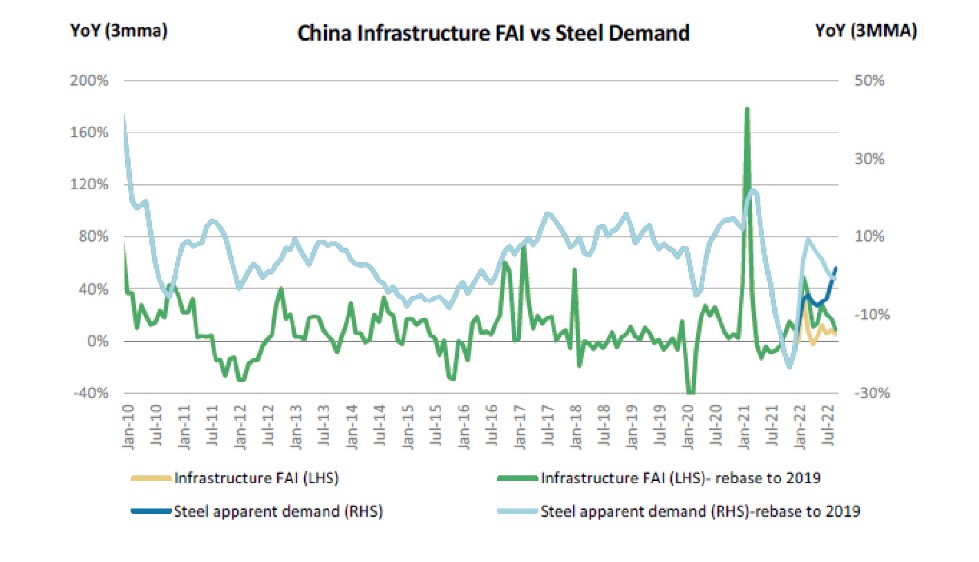

There are signs of life in the iron ore space (figure 1) with the spot price (62% fines) up over 25% this month as the Chinese government attempts to re-engineer policies towards economic growth. As figure 2 shows, steel demand is mostly leverage to infrastructure spending and property which appear to be turning the corner (figure 3) while infrastructure spending (figure 4) appears relatively flat.

China’s largest commercial banks have also agreed to extend $162 billion in new credit to private developers to counteract the recent liquidity crunch. The national bond authority also expanded by US$35 billion a program to support the sales of bonds after a series of defaults saw spiralling credit costs for residential builders.

CY 2022 was a difficult year for property with new starts falling 35.1% YoY in October and 44% YoY in September.

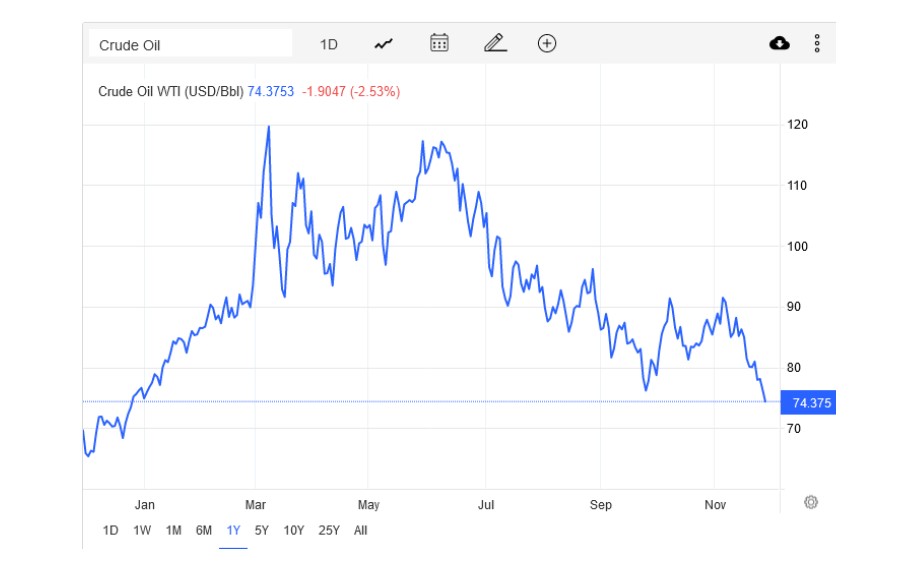

WTI crude oil lost another 5% last week to close at US$76.55/bbl (now sitting at US$74.37/bbl) (figure 5) with Grandpa Joe now using the proceeds from the sales of the US strategic stockpile to buy heating oil and diesel.

In other words, he is selling unrefined oil and buying in third party refined petroleum products. Or as Mickey Fulp would say, “buying high and selling low”, a good way to go broke real fast as oil inventories fall another 3.7MMBLS to nearly five-year lows. Fulp also points that the US has relinquished its role as the swing producer which has now reverted back to OPEC.

Plenty of economic data out this week in the US including revised Q3GDP, personal consumer expenditure, manufacturing PME and the jobs report. On the junior end our Canadian friends appear to be struggling somewhat (I always think a mining boom is more fun with the Canadians leading the charge) with the TSX-V flat at 576 unchanged for the week but down 41% year on year and 39% year to date.

Not sure how much Cristal champagne they are drinking in Toronto and Vancouver at the moment; another leading indicator of economic health I like to review from time to time…

New ideas… update

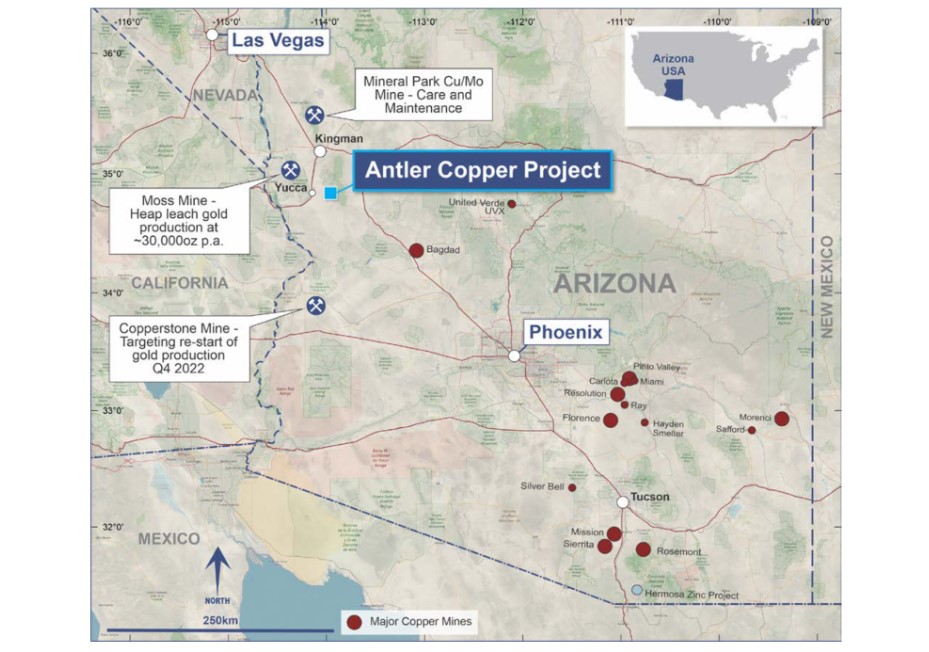

The last 12 months have delivered some impressive results for New World Resources (ASX:NWC) at its 100% owned Antler Copper project situated in Arizona (USA) (figure 7) which has been dormant since 1975. Interestingly inflation that year in the UK peaked at 24.2% and the price of petrol leapt by 70%.

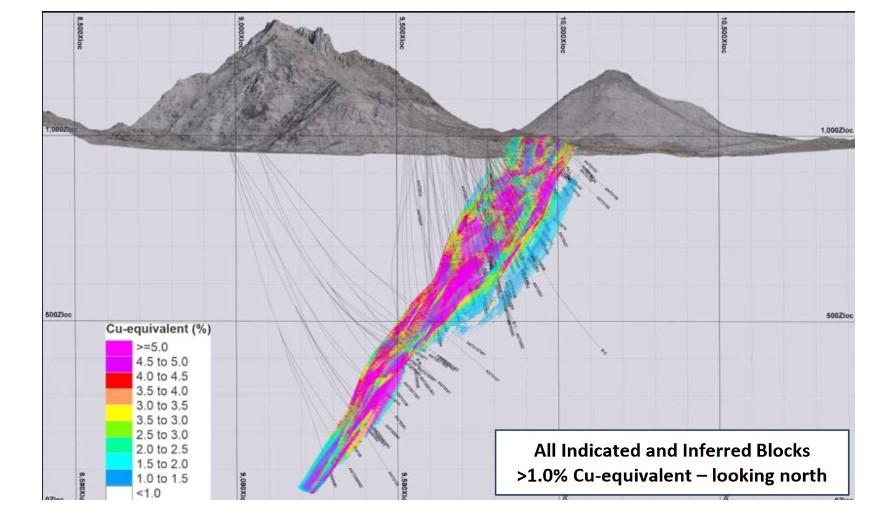

The company recently updated its JORC Mineral Resource Estimate (1% Cu equiv cut-off grade) to 11.4Mt @ 2.1% Cu, 5.0% Zn, 0.9% Pb, 32.9g/t Ag and 0.36g/t Au.

(4.1% Cu-equivalent*) representing a 48% increase in tonnes and 44% increase in contained metal since the 2021 maiden JORC Resource (figure 8).

While not a big fan of Scoping Studies, I do like the US$525m Net Present Value using a 7% discount rate with an impressive 42% internal rate of return (figure 9 – 2021 Scoping Study). I would think the significant increase in the 2022 JORC Resource has a good chance of improving these financial metrics at the Pre-Feasibility and Feasibility Stages. The Scoping Study contemplated a relatively simple flowsheet producing copper-gold, lead-zinc and silver concentrates at an operating cost (C1) US$1.66/lb copper equivalent.

I like the exploration upside (figure 10) which should feed into further resource upgrades and a better set of financial metrics as the project rolls into the more advanced study phases. The PFS is scheduled for completion in Q4 2023. I thoroughly recommend going to their website and reviewing the 2022 AGM presentation which I think has been very well put together.

Bottom line for this stock is I think +US$600m NPVs aren’t far away which should translate to, say, 20% discount to NPV (US$600m) at PFS = US$120m enterprise value (A$176m) or around +9 cents per share assuming no further share issues.

I think this is a little conservative and +10-15 cents is a better than even bet from here by mid to late next year. For those Stockhead faithful who believe we should see an uptick in commodities next year, this stock should provide excellent leverage.

At RM Corporate Finance, Guy Le Page is involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting, and corporate advisory roles.

He was head of research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July 1998. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada, and the United States. The views, information, or opinions expressed in the interview in this article are solely those of the interviewee and do not represent the views of Stockhead.

Stockhead has not provided, endorsed, or otherwise assumed responsibility for any financial product advice contained in this article.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.