FREE WHELAN: A Beatle, Consumer Spend, BoJ Week. Also Albo, Beijing Bikini’s, Barron’s Curses and Anticipation

Via Getty

In this Stockhead series, James Whelan Managing Director Barclay Pearce Capital Asset Management offers his insights on the key investment themes and trends across domestic and global markets. From macro musings to the metaverse and everything in between.

This week I will be dropping in and out of IMARC (International Mining and Resources Conference) from the 31st October to the 2nd November in Sydney.

If you’d like to reach out and say g’day and talk about core samples or copper grades, please do so…

I can’t promise I’ll be able to talk about them but I love hearing stock stories and people’s outlooks on various sectors.

Saturday night event of a lifetime just passed. Seeing Sir Paul McCartney with my father at Allianz. Just an amazing experience. Something stuck with me though as he commented:

“There’s fans who come to all our concerts, and that’s not cheap. We still haven’t figured out how they’re paying for it…”

*laughter from the stadium crowd*

There’s me thinking about US Consumer data being up 0.7% in September vs 0.5% forecast.

“STOP SPENDING MONEY” says Area Man live from ex-Beatle rock concert.

The US Consumer simply will not stop, doesn’t know how to stop and yet every bullish consumer number that’s come out has always been attached to “but it’s expected to slow down soon” in the media.

When? WHEN? it’s been a year of this. Maybe it needs to go on Barron’s cover.

Japan Reiteration

A happy BOJ week to all who celebrate! Remember that the Band of Japan have a two-day meeting Monday – Tuesday with the monetary policy decision appearing out of that. My pick is for a proper direction on abandoning Yield Curve Control.

There’s debate on this call, and there’s debate on what happens following. As a standard, buying Japanese banks wouldn’t be the worst idea. Higher yields = better for banks, all things being equal.

I’m happy to be more of a generalist and happy to back the index while being long Yen. This is a reiteration of the theme pointificated by Blackrock a few weeks ago that there is a massive pit of money sitting in Japanese savings accounts that has to go to work and will do it in the easiest way there is to beat persistent (but not super high) inflation – and that’s plowing head long into Japanese equities.

Yields will rise so money will go into Yen too so it’s a perfect cacophony.

If you’d like to know more about this sort of idea please let me know.

The Curse…

The Barron’s Cover Curse is a well known, very funny, yet partially true phenomenon in which Barron’s Monthly will run a cover that is almost always calling the exact wrong direction in a moving market. (I.E. Europe rallies for a few months and they run a cover – “Europe and why the smartest guys have to be there” – and as sure as God wears sandals, there’ll be a 15% correction in Europe by the time the week is through.)

They’ve just run this on bonds and it makes me think yields have a way to go higher.

Still, if you have a set retirement objective then actually buying a government bond with a fixed date is a great way to go. If you were looking to trade them and pick the bottom in bond prices then thanks a bunch Barron’s.

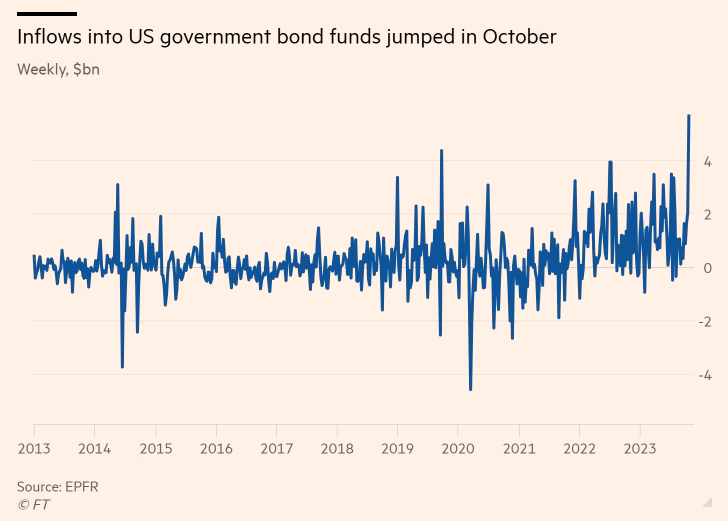

That being said, inflows by the big end of town into bonds has been extraordinary.

Despite what Sir McCartney says the economy is still seen as slowing and yields set to decline a little. Don’t get in the way of a freight train of money.

Theory of Thing Podcast: with more of these types of ideas, so have a listen and let me know what you think.

Also Albo

…is on his way to China this week.

First PM to do so since Turnbull in 2016.

I wrote then about the emerging phenomenon of the “Beijing Bikini” and after 7 years I’m happy to report it’s still very much in use.

I’m not sure if your social credit score drops in China if you’re caught doing this but it should.

Please brace yourself for the photo…

But seriously, look for further thawing of the China/Oz relationship, especially in the wine trade.

Until then all eyes on the BOJ!

All the best and stay safe,

James

The views, information, or opinions expressed in the interview in this article are solely those of the writer and do not represent the views of Stockhead.

Stockhead has not provided, endorsed or otherwise assumed responsibility for any financial product advice contained in this article.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.