Eastern Australia’s gas supply gap is widening. Here’s what might happen

The gap between gas supply and demand in eastern Australia is growing. Pic: Getty Images

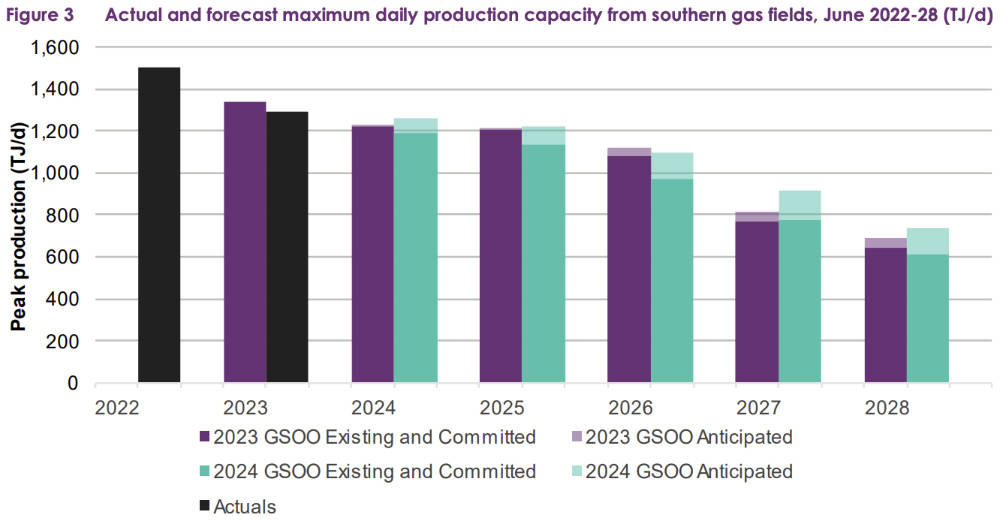

Major gas consumers in eastern Australia have been sweating bullets since the Australian Energy Market Operator forecast that the annual supply gap would increase in magnitude from 2028 as southern gas production declines.

And to make it worse, the operator of Australia’s largest gas and electricity markets and power systems added in its latest 2024 Gas Statement of Opportunities that the forecast demand for gas-fired electricity generation would increase from the mid 2030s due to the retirement of coal generators.

This could very well deepen the supply gap, which could in turn raise the spectre of load shedding during periods of peak demand.

Before this nightmare scenario comes to pass, eastern Australia could experience shortfalls on extreme peak demand days from 2025 and small seasonal supply gaps from 2026.

Gas supply/demand imbalance

Despite this, the irony is that Australia actually produces a lot more gas than it actually consumes and will continue doing so for decades to come.

So just how this sorry state of affairs come about?

For starters, much of eastern Australia’s gas production comes from Queensland while most of the demand is in the southern states – New South Wales and Melbourne.

While demand from these states had previously been sated by gas sourced from the Bass Straits, the continuing decline of the ageing fields in the region coupled with increasing demand is directly responsible for the AEMO’s dire forecast.

Efforts to access unconventional sources of gas – like coal seam gas – have been stymied by state governments with Victoria standing firm on its ban on fracture stimulation (fracking), which is key step in making CSG economic.

Matters are certainly not helped by NSW passing legislation earlier this year to ban offshore drilling and mining – a development that is likely to make it difficult to explore or develop some prospective resources that could have contributed significantly to the gas supply picture.

It is no surprise then that the southern states are turning to Queensland and its extensive coal seam gas fields to meet demand, though this has challenges of its own.

Firstly, there is insufficient capacity on the key Southwest Queensland Pipeline (SWQP) that transports the actual molecules from Queensland to its southern neighbours, a shortcoming that is being addressed to some extent by the ongoing Stage 2 expansion of the pipeline, which is due to be completed by winter 2024.

Even then, the AEMO believes that the pipeline’s capacity will still be insufficient to meet peak demand.

The other concern is that a large portion of the state’s demand is earmarked for the export market through the LNG projects in Gladstone.

While the Australian government could exercise the Australian Domestic Gas Security Mechanism and limit LNG exports in order to meet domestic demand first, doing so could prove detrimental to our otherwise stellar reputation as a trade partner.

LNG import and new gas sources

So just what can be done to address the southern state’s needs?

One option is to construct an LNG import terminal in the southern states, a process that is already underway and nearing completion.

Andrew Forrest’s Squadron Energy has nearly completed construction of an LNG import terminal at Port Kembla, which it claims will be enough to supply most of the needs of NSW and Victoria.

Once completed, it will provide the two states with a ready-made solution to import gas to meet their needs, albeit having to rely on more expensive LNG for supplies.

This could potentially be alleviated by developing new gas fields in Queensland and the Northern Territory that could be earmarked entirely for domestic uses and feeding the resulting gas into LNG plants on the proviso that they be shipped to the Port Kembla terminal, which could be cheaper than buying LNG off the market.

Project developers

On that note, here are companies that are developing new fields or expanding their existing gas fields to help meet domestic demand.

In Queensland, Comet Ridge (ASX:COI) holds 100% equity in three project areas within the Mahalo gas hub area and 57.14% in the Mahalo joint venture with Santos (ASX:STO).

These assets are being developed to supply gas into the east coast gas market with the Mahalo JV having gross proved and probable (2P) reserves of 266 petajoules of gas along with a pipeline connection to both the domestic Queensland gas pipeline and export GLNG pipeline.

COI also plans to deliver gas from its wholly-owned assets into nearby infrastructure and has the option to connect to its JV project with Santos.

Galilee Energy (ASX:GLL) is progressing the multi-well pilot program at its Glenaras project in Queensland’s Galilee Basin.

It currently has three wells online with a rotation strategy in place to collect further subsurface data to assist in determining the extent of any preferential, directional reservoir characteristics.

Additionally, the company has updated its subsurface model with contemporary Glenaras pressure data and recently acquired and interpreted 3D seismic data.

This work has confirmed that the target coals are only now approaching the critical desorption pressure required for material gas rates to result, which will in turn propel the Glenaras pilot into the final stages of achieving commercial gas rates.

The lure of providing gas to the east coast gas market also proved strong enough to convince Queensland Pacific Metals (ASX:QPM) to focus more on its producing Moranbah gas project.

Moranbah captures waste mine gas (methane) from coal mines, producing a not insignificant 10PJ of gas per annum from its current 2P reserves of 240PJ.

However, QPM is already taking steps to boost production and reserves.

It is continuing its well workover program, which seeks to bring offline or suspended wells back into production – a process that is expected to take the well count up from 118 producers up to 130 producers by the end of May.

The company has also started drilling the first of seven planned production wells in a highly productive area of the field. These wells are expected to deliver a significant boost to production once they are brought online progressively during the December quarter.

Meanwhile, Omega Oil & Gas (ASX:OMA) is preparing to drill the horizontal section of its Canyon-1 well in Q3 2024 once it secures a drill rig.

The company, which has independently assessed its wholly-owned ATPs 2037 and 2038 in Queensland’s Taroom Trough to host best estimate (2C) contingent resources of 1.73 trillion cubic feet (Tcf) of gas, will drill the horizontal well through the Kianga Formation before carrying out a multi-stage stimulation program.

This program is aimed at testing the productibility of gas from the deep Kianga Formation in the Taroom Trough.

Not all the activity is in Queensland though with 3D Energi (ASX:TDO) looking forward to a 2025 exploration drilling campaign of up to six wells at the offshore Otway Basin joint venture with operator ConocoPhillips (80%).

The drilling in permits VIC/P79 and T/49P within Commonwealth waters consists of two firm exploration wells and up to four contingent wells.

Bass Oil (ASX:BAS) has been moving to commercialise its deep coal resources in PEL 182 within the Cooper Basin, South Australia, that could host prospective in-place resources of up to 21Tcf of gas.

While prospective resources are unproven (undrilled) while in-place numbers represent the amount of gas present if the reservoir were filled to the brim rather than the economically feasible numbers, the sheer scale has the company preparing a study into the deep coal potential.

As part of this, it is also preparing to complete the Kiwi-1 gas discovery that is estimated to host mean resources of about 5.24 billion cubic feet of gas.

Should this be successful, it will allow the company to pull infrastructure to the northern Cooper Basin, connecting other plays between Kiwi and PEL 182 deep coals.

Metgasco (ASX:MEL) has stakes in producing gas fields along the border between Queensland and South Australia.

It has a 25% interest in PRL 211 in the South Australian Cooper Basin that includes the Odin-1 well that produced gas a gross rate of 4.7 million standard cubic feet of gas per day (MMscfd) during the December 2023 quarter.

MEL also holds 25% in ATP2021 on the Queensland side of the Cooper Basin. This includes the Vali-1 that produced 2.15MMscfd in the same period.

The Vintage Energy (ASX:VEN) led joint venture has plans to drill a further two wells at the Odin field.

Meanwhile, Red Sky Energy (ASX:ROG) has a 20% stake in the six licences that make up the Santos-operated Innamincka Dome gas project in South Australia that started production in the December 2023 quarter.

Santos will carry out processing and interpretation of recently acquired seismic over portions of PRL14, including Yarrow and PRL17 at the Innamincka Dome with results expected towards the end of 2024.

Results from this work will be used for a full field development plan.

Up in the Northern Territory, Tamboran Resources (ASX:TBN) and the Beetaloo joint venture has a binding long-term sales agreement to supply the Northern Territory government with 40 terajoules of gas per day from 1H 2026 for an initial nine-year term.

This represents about two-thirds of the NT’s requirements and will be delivered to the APA-owned Amadeus Gas Pipeline on a take-or-pay basis at a market-competitive gas price.

TBN has a 47.5% working intertest in the 51,200-acre area that will include the wells

required to deliver the proposed pilot project volumes.

At Stockhead we tell it like it is. While Queensland Pacific Metals is a Stockhead advertiser, it did not sponsor this article.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.