Chain Reactions: UK continues innovation-friendly moves towards crypto; Bitcoin up 3%

Getty Images

Hope you’re taking note over there in the US of A, Chairman Gary Gensler, Senator Elizabeth Warren, and Sleepy Joe Biden… because the crypto game is afoot in the UK. Not to mention in Russia, the Middle East and Asia.

But let’s start with the UK, because some innovation-friendly language pertaining to crypto and blockhain has just come to light from one of the nation’s top financial regulators – the Financial Conduct Authority (FCA).

FCA Executive Director Sarah Pritchard was speaking at London’s City Week conference overnight (AEDT), and she emphasised the importance of collaborating with industry on crypto regulations.

“We want industry’s input to make sure we get the future regulatory regime for crypto assets right,” said Pritchard, adding:

“Let’s work together, to shape our rules and regulations to benefit markets, consumers and firms as crypto goes from niche to mainstream.”

Blimey.

It’s obviously a bit early to assume UK regulations will help foster crypto-industry growth in one of the world’s biggest economies, but it sure makes a nice change to hear a major financial watchdog speak in reasonably open and accommodating terms regarding the nascent technology and its participants.

And there have been some other pretty good signs recently, too, that the UK could be setting itself up to become something of a crypto/blockchain hub.

In her speech at #CityWeek2023, Sarah Pritchard spoke about the regulation of #cryptocurrency and how effective early engagement can support regulation that benefits all. https://t.co/w6Zv6K5FP1

— Financial Conduct Authority (@TheFCA) April 25, 2023

That said, the FCA is consulting with counterparts in the US, so let’s hope Gary “Ever Since I Became SEC Boss I Can’t Officially Tell You if Ethereum is a Security” Gensler doesn’t muddy the waters for the UK regulator too much.

— Brian Armstrong (@brian_armstrong) April 26, 2023

Pritchard also described crypto as a “one-time symbol of alternative rebellion,” acknowledging that it has “become more widespread”.

“Effective early engagement supports regulations that benefit all and helps firms be prepared when regulations come into force,” the regulator added.

This line is encouraging, too:

““Crypto assets and blockchain offers opportunities for more efficient and innovative financial services and products … There are plenty of advantages in terms of efficiencies and innovation, which we want to support.”

Meanwhile, over in Russia

Take this, too, how you will (obviously), but Russia has reportedly (according to Bitcoin.com and Russian news outlet Tass among others) announced it has plans to launch a new payment system that will be “bound by no restrictions” and will enable the use of digital currencies for international payments.

On Monday, the country’s finance minister Anton Siluanov is reported to have said: “Digital currencies could be used in cross-border payments. This is just the earliest phase of discussions, but the future lies with the use of the digital ruble, the digital yuan, and other similar currencies.”

Of course, he’s mainly talking about CBDCs (central bank digital currencies) there, but along with the clear effort to continue Russia’s “de-dollarisation” efforts, the hazy reference to “other similar currencies” is the interesting part of his sentence.

We can only speculate at this stage as to whether he might mean various stablecoins and other cryptocurrencies in his rhetoric about unbound restrictions.

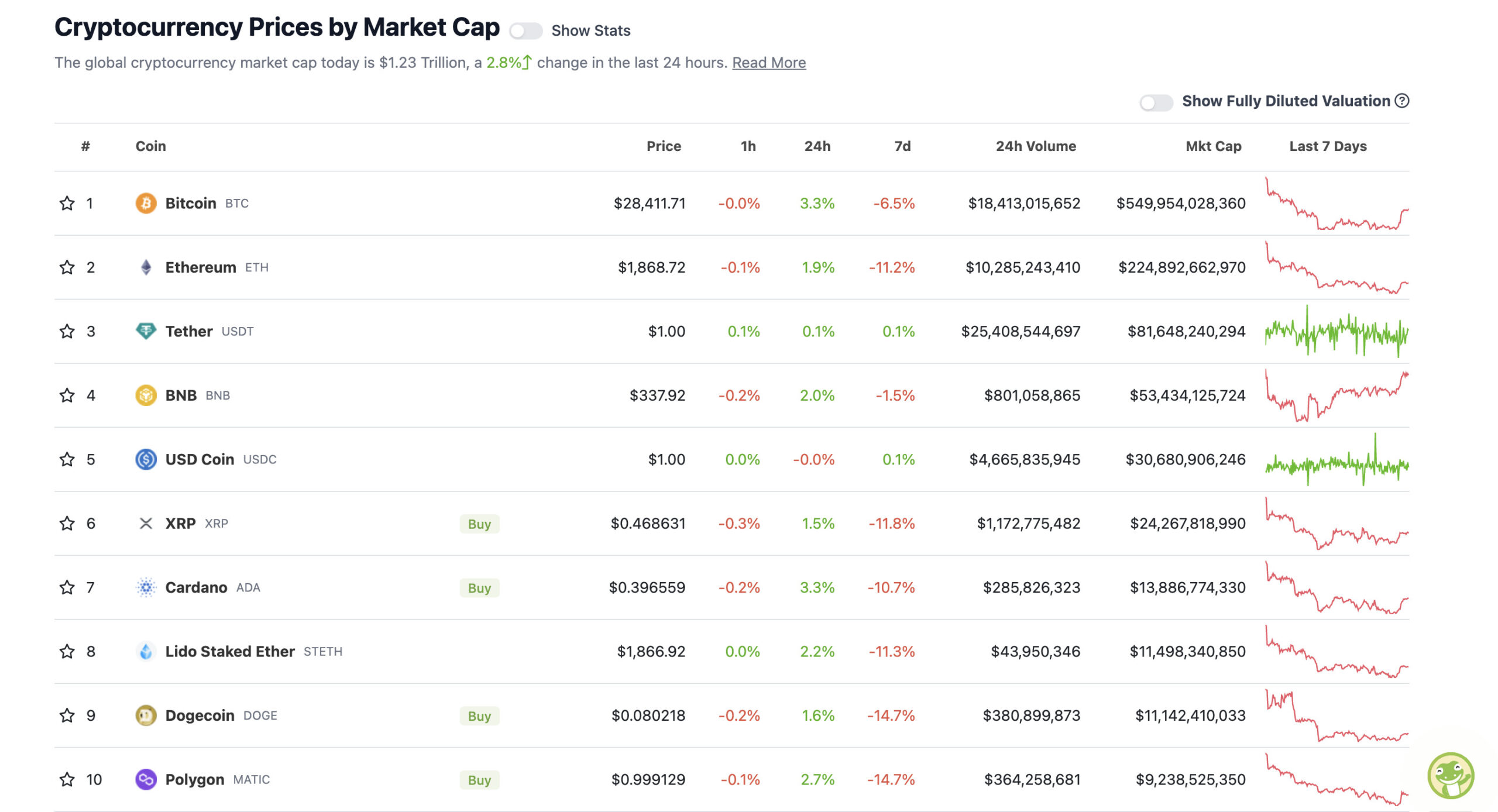

Top 10 overview

With the overall crypto market cap at US$1.23 trillion, up about 2.8% since this time yesterday, here’s the current state of play among top 10 tokens – according to CoinGecko.

Around the blocks

Some pertinence and randomness that stuck with us on our daily moves through the Crypto Twitterverse.

The probability for another 25 bps rate hike in May is just over 78.3%, down from 90.5% yesterday. pic.twitter.com/5byOHbBSLY

— Benjamin Cowen (@intocryptoverse) April 25, 2023

What's the biggest hurdle to mass adoption of crypto?

— Coin Bureau (@coinbureau) April 25, 2023

#Bitcoin did continue to hold the box at $27,000 and broke above the crucial breaker of $27,800 -> back in the range.

Next resistance is $28,800. If we'll have a slight consolidation, it seems likely that we'll continue moving upwards to $30,000. pic.twitter.com/KYRTp37K13

— Michaël van de Poppe (@CryptoMichNL) April 26, 2023

Trading rule based on S2F model. Buy BTC 6 months before halving and sell 18 month after halving. Outperforms BTC buy&hold in both return and risk. Of course not financial advice and no guarantees that it still works. Just a nice EMH test. What do you think? pic.twitter.com/nRWtlsgFE1

— PlanB (@100trillionUSD) April 25, 2023

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.