Via Getty

Faceboo… I mean Meta is having a very serious and very public identity crisis

Tech

Via Getty

Tech

There is blood is in the metaverse water this morning, if the metaverse does indeed have water.

The bleeding, if Meta Platforms does indeed have any blood, is leaking from the hot tech-mess that was once Facebook.

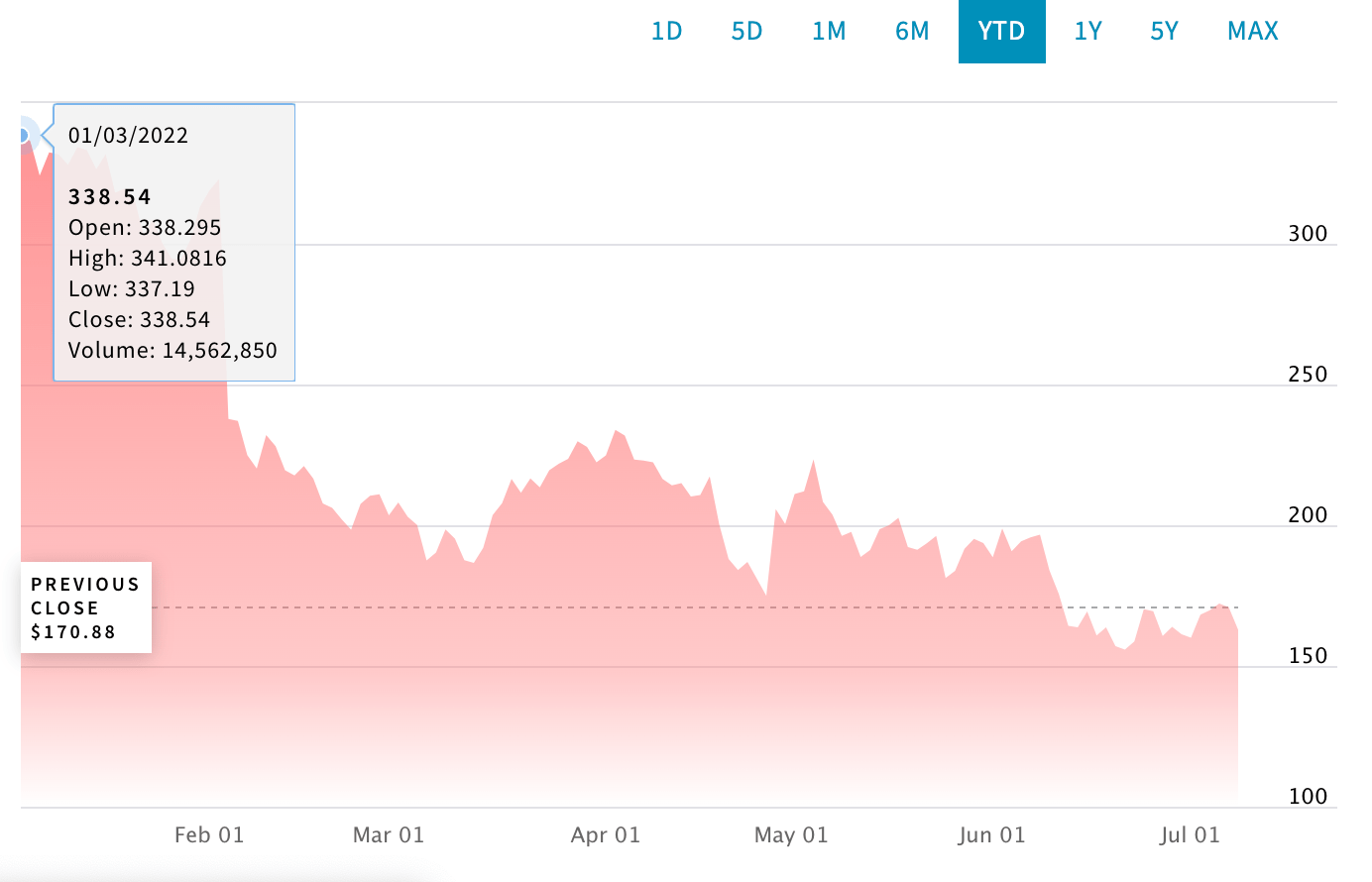

The immediate cause appears to be an overnight stock downgrade to Underperform from Hold by popular Needham & company MD, senior internet & media analyst Laura Martin. Shedding almost 5%, Meta is now barely treading meta-water at US$162.88. It began the year above $US330.

But a collapsing stock is just another symptom of a bigger, huger META-sized problem… no-one, Meta included, knows what Meta is.

Now, I stopped using Facebook years ago. Probably around the same time youngsters realised they should never start.

Facebook knows they shouldn’t either. Its purpose has been reduced to the ridiculous, the inane and the poisonous.

The smartest commercial exercise it could muster – remember this is still home to some 2.91 billion monthly active users (as of April) – is still just advertising.

That’s nothing short of a failure of imagination.

Which is why it doesn’t want to to be that anymore. It now wants to be this company:

When virtual and physical worlds collide, anything can happen. Digital creators unlock the possibilities of our tech and end up in all kinds of things virtual and augmented environments. Check it out: https://t.co/t0h9kYwHCt pic.twitter.com/7MKEEFDVwe

— Meta (@Meta) July 5, 2022

And what this company actually does, remains one of the more open, yet unspoken mysteries in tech today.

It’s been a gruelling year for Meta.

Philosophically, I am absolutely behind the collision of the virtual with the physical in the search for augmented environments. But I think of companies like Althea Group (ASX:AGH) or my local pub for that, long before I think of Meta.

So far 2022 has been one long existential crisis for a company which is still somehow home to the third most visited website in the Berners-Leeverse. Suddenly the user base appears porous. Investor and user sentiment alike has soured.

In February, Meta Platforms recorded its first-ever quarterly decline in the critical FB metric of daily active users.

In the March quarter its monthly active users came in well under analyst expectations for the first time.

The pandemic should’ve been an engine of creative and commercial industry. An engine of change and ecploration.

Not just somewhere for everyone to park their money as the record high share price began to take on a bloated and slightly breathless weight.

As the Nasdaq began reversing its cyclical gains, Meta just looked like it was having a stroke.

Undoubtedly chastened by a collapsing share price, the best idea the remaining Mark Zuckerbergians have had is to stop hiring talent and root out the non-believers.

In a recent theatrical ’round table’ with employees, the CEO strode the digital stage talking up the reboot. The executive has a new focus a new management and a new raisaon d’etre.

According to the New York Times last week, Zuckerberg warned his team Meta was in one of the “worst downturns that we’ve seen in recent history.”

Unfortunately for Meta Platform workers in hard times, apparently lots of them are no longer wanted or welcome and should you choose to stay, it’s going to be pretty shite.

The CEO told his near 78K Meta workforce they should brace for more work, less resources and a tougher performance process.

“I think some of you might decide that this place isn’t for you, and that self-selection is OK with me,” Zuckerberg reportedly said “Realistically, there are probably a bunch of people at the company who shouldn’t be here.”

The fact is The Zuck’s idea of a Meta Platform escape simply can’t escape the dire economic world the rest of us live in.

Shares of Meta Platforms Inc (NASDAQ:META) have slumped well over 50% since January and last night Needham & Co threw the first punch in anger, and it’s likely the kicks will follow.

“Meta has stated that it is investing in the Metaverse at the same time it is guiding to slower revenue growth. We lower our estimates because we believe cost growth will far exceed revenue growth for the next 2 years,” Martin said in a note to clients.

Then there’s the heaps of worries investors have about Meta people figuring out what consumers actually want from them.

Then there’s the surging quality and volume of competition.

Needham and Co reckon Meta’s company moat, its strategic uniqueness, is deteriorating.

Then there’s the world of fabulous new and decidedly anti-dominance regulatory obstacles.

And Metaverse comes with a whole wall of investment risks, Martin says before suggesting shareholders could “use Meta as a source of funds” and investors should stand by – as worsening short-term fundamentals and risks around structural valuation intensify in the current economic environment.

“We recommend investors remain on the sidelines while they assess several structural valuation risks including consumer behaviour shifts, competition, moat degradation, regulatory risks and Metaverse investment risks.”

Martin says the company’s uncertain but mighty pivot into the metaverse has been ill-timed and the pay-off arc could be like finding a pot of gold at the end of a rainbow.

“Near-term, we worry that consensus estimates are too high, based on Meta’s promises of higher investments in the Metaverse at the same time it is purposely slowing its revenue growth to better compete with TikTok,” Martin said.

Basically she reckons the gamble could take too long to pay off.

“We worry that Meta’s enormous spending to create a new world called the Metaverse suggests it fears existential risks to its historical collection of businesses,” Martin added.

Get the latest Stockhead news delivered free to your inbox.