Happy days for CML Group shareholders ... not so much for Scottish Pacific. Picture: Getty

CML Group shows Scottish Pacific how it’s done

Tech

Happy days for CML Group shareholders ... not so much for Scottish Pacific. Picture: Getty

Tech

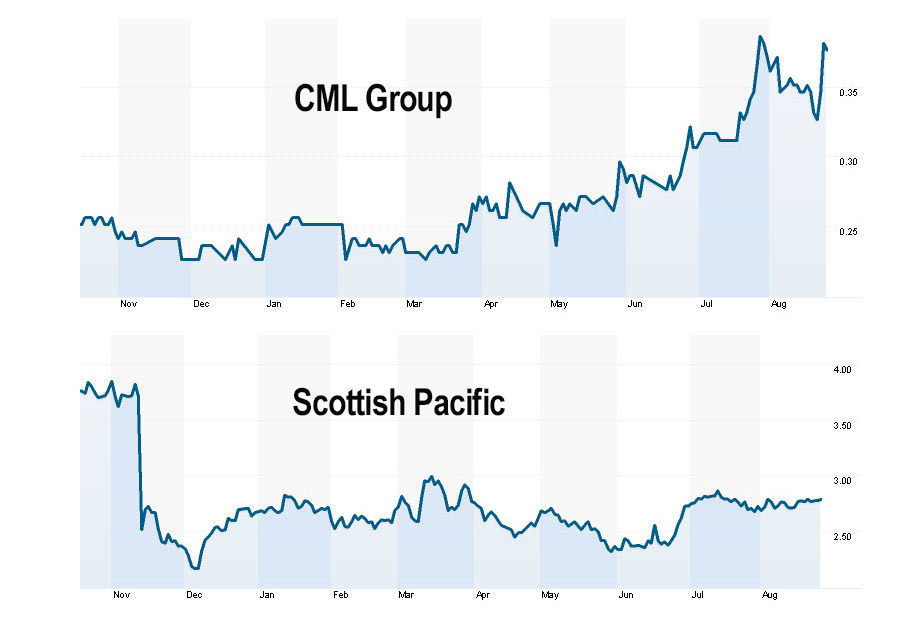

While the big end of town did its dough in last year’s float of specialty trade financer Scottish Pacific, payroll minnow CML was reaping the rewards of bedding down acquisitions that helped lift its shares to all-time highs.

From an initial public offering priced at $3.20, an unexpected profit warning late last year saw Scottish Pacific (ASX:SCO) shares dumped into the sin bin. They are still trading well under $3.

Yet shares in CML (ASX:CGR) last week hit new highs close to 40c as earnings hit a new peak. Its shares have doubled in price over the past year.

Both companies operate in the same industry but Scottish Pacific boasts a market cap of just over $300 million, compared with only around $45 million for CML.

After starting out in the recruitment sector, CML morphed into salary funding and payment services and now into invoice financing.

CML took time finding its feet and has only recently managed to build scale with key acquisitions over the past few years. The lift to scale has helped lift margins.

But its small size has hampered growth. A constrained balance sheet left CML with little alternative but to borrow expensive money, mostly via bonds costing around 8 per cent.

There was also an issue of convertible notes carrying a coupon of 9 per cent a year.

The sustained uplift in the CML share price, to recent highs at 38c, has given the company the right to convert the notes, which will lift shares on issue by close to a third.

But the real kicker will be a steep cut to its cost of funds, since conversion will axe the cost of the 9 per cent interest payment, and add close to $1 million to the bottom line – a quick 40 per cent profit uplift, albeit with dilution to earnings a share, and a higher dividend bill.

This cut to funding costs won’t be a one off.

CML has raised $65 million via three bond issues which mature in 2020 and 2021.

The first bond issue was for $25 million, with the second the same size plus a $15 million extension.

CML reckons that over the next two years it will shift to majority bank-funding, which will lower the cost of funds to 3 to 4 per cent from the 8 to 9 per cent it is paying at present — a lower cost of funding that should flow through to higher profits.

A funding line with the ANZ Bank, for example, costs around 4 per cent, which is a clear pointer to the potential margin uplift.

Typically, CML targets a margin of more than 2.8 per cent on its invoice funding, which will rise significantly as it restructures the balance sheet.

And with the financier already purchasing around $1 billion of invoices annually, any improvement in funding terms will earnings a lift.

As the scale of CML’s financing activities has expanded, this has reduced operating costs, which has also flowed through to the bottom line – an improving cycle which CML reckons will continue.

Or as the company’s managing director, Daniel Riley puts it: CML has simplified and improved its business over the past two years and is confident of its growth prospects.

CML has emerged as the second largest ASX-listed non-bank invoice financier in Australia, with the largest operator in the sector believed to be Scottish Pacific.

Along with refining existing operations, CML is planning to launch new products, such as equipment financing which, while it is unlikely to have much of an impact on the bottom line anytime soon, does give its sales team something extra to talk to clients about while also adding another leg to earnings down the track.

Get the latest Stockhead news delivered free to your inbox.