Pic: Bloomberg Creative / Bloomberg Creative Photos via Getty Images

Why junior miners are lagging their larger counterparts (and is it time to buy?)

Mining

Pic: Bloomberg Creative / Bloomberg Creative Photos via Getty Images

Mining

For Australia’s mining industry, the macro conditions have been pretty strong in the first half of the year.

Iron ore prices have pushed to new record highs, while gold cleared $2,000 an ounce for the first time ever.

For the listed junior explorers and mining companies that make up the small cap resources index, it makes for an interesting operating environment.

There’s been some unsolicited bids and joint-venture overtures, as markets speculate who’s next in line as a potential takeover target.

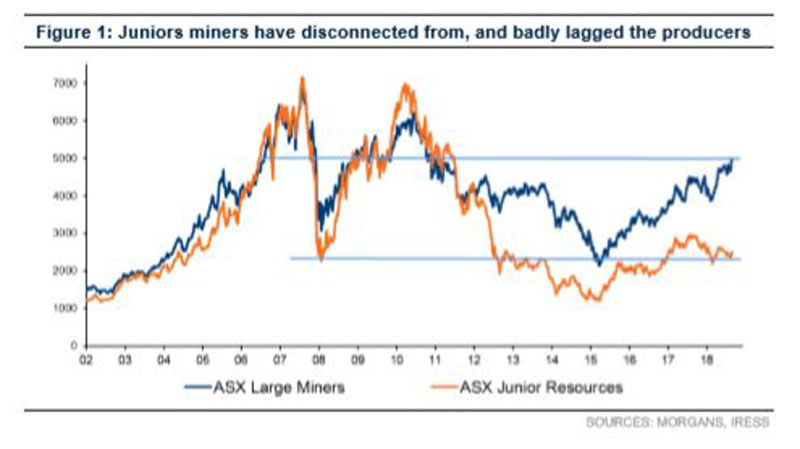

But within that backdrop, Tom Sartor and the research team and Morgans highlighted an interesting trend; smaller miners have noticeably underperformed their larger counterparts.

This chart from Morgans tells the story:

The analysts cited a number of reasons for the split, but also said the current state of play provides an opportunity for investors to “buy when no one’s shopping”.

Sure, it won’t be a return to the speculative days of the mining boom, but Morgans said the disconnect in valuations is “likely concealing several opportunities”.

Looking at the industry more broadly, Morgans said it was seeing the benefits from a combination of strong prices, the “robust focus” on costs and a lower Aussie dollar.

As a result, the value of Australia’s mineral exports is now around “six times higher than pre-boom levels”.

So why the lag in the junior’s share prices? The team at Morgans cited “competition for risk capital” posed by the tech sector, and the inability of the sector to articulately communicate its value proposition amid some complex headwinds for the global economy.

Those sentiments were echoed in part by Hedley Widdup, fund manager at listed investment company Lion Selection Group.

Speaking with Stockhead, Widdup began by highlighting the risk-averse nature of what he called “big money”.

“The majors have everything that risk averse institutional money is after, the juniors don’t,” he said. Namely, things like “funding, permitting, development and commissioning”.

And rather than allocate portfolio funds to riskier small-caps, big investors are more or less just avoiding the sector right now. He also cited the influence of global capital flows into the huge exchange traded funds (ETFs), which implement rules around minimum investment size.

Moving from big money to “risk money”, he also cited the allure of tech investments pointed out by the Morgans team.

“Typically, risk money moves sectors because the music stops in one place, not because it has started elsewhere,” he said. And right now, the music is on in tech.

Although, the competition isn’t so much from local tech stocks, but “unlisted start-ups overseas”. Widdup said a large pool of private equity capital had “found its way into unlisted start ups, and in those companies there is no market to price funding rounds – it’s in everyone’s interest for each round to be higher priced”.

Lastly, he cited a string of recent collapses in Australian gold mining projects which have left investors once bitten, twice shy (in this case, “bitten very hard”).

For example, “one raised money shortly before entering administration. These leave shareholder’s heads spinning, and instead of feeling wary they are all out in avoidance after that”.

But despite the various stumbles and pitfalls, both Widdup and the Morgans team said the potential of Australia’s small-cap mining sector isn’t lost on investors.

“The mining industry is well aware of the value on offer in the junior space,” Widdup said.

He added that in the current environment, smaller companies had also been rewarded for executing tie-ups that created scale — pointing to the recent merger between Silver Lake Resources (ASX:SLR) and Doray Minerals (ASX:DRM).

Creating size through mergers brings companies into the scope of the big investors and ETF flows, and therefore “need to be owned”.

Morgans recommended a portfolio approach, where investors aim for “super returns” from around 20 per cent of the companies they invest in.

The team suggested exposure to commodities where prices are still depressed, such as uranium and oil & gas. Morgans also highlighted juniors with high exploration upside, or legitimate pathways to production.

“Greed is creeping back into the market, and if juniors become a target, sooner or later the market will become watchful for this and start to speculate on who is next,” Widdup concluded.

The following companies were highlighted by Morgans as part of their tactical investment recommendations:

Low valuation and high exploration upside:

Sunstone metals (ASX:STM)

Stavely Minerals (ASX:SVY)

PolarX (ASX:PXX)

Plausible pathway to production and cashflow:

Panoramic Resources (ASX:PAN)

Cassini Resources (ASX:CZI)

Cooper Energy (ASX:COE)

Get the latest Stockhead news delivered free to your inbox.