Mining

Monsters of Rock: EVN in a race to meet ambitious gold targets but with prices where they are does it even matter?

Mining

Pantera Minerals seizes opportunity amidst growing US lithium demand

News

Pic: Bloomberg Creative / Bloomberg Creative Photos via Getty Images

Mining

We take a look at the major commodities and what moved them, including winning and losing metals in the month of March.

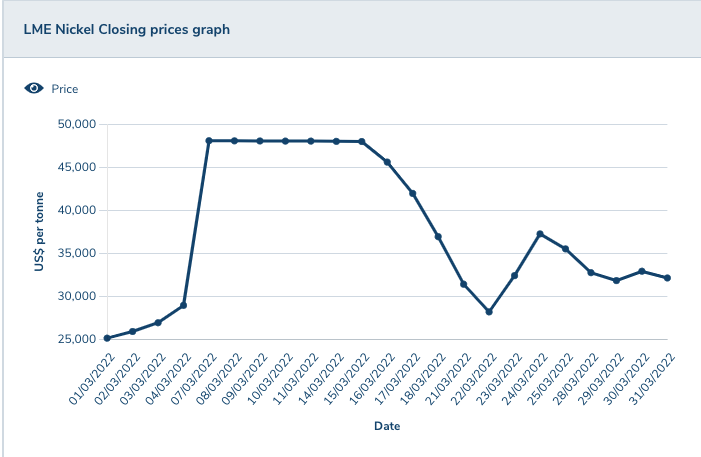

Price: US$32,107/t

%: +32.22%

This ^^^ doesn’t tell the whole story for March’s most talked about commodity.

Nor does the chart below. Officially the keeper of the keys when it comes to base metals prices, the London Metals Exchange says nickel prices peaked at US$48,063/t.

In reality they rose to more than US$100,000/t on March 8, nearly double even their historic highs of US$54,500/t that characterised the commodities strongest ever bull market before the GFC in 2007.

And they made that leap in just two hours of Asian trade, prompting the LME to close the shop, cancel all trades, take its ball and go home in a huff.

The reason was threefold. Firstly, the rise of demand for LME nickel briquettes from EV battery makers led to an historic draw on exchange stockpiles.

Second, Russia’s Norilsk Nickel is the largest producer of refined class 1 nickel in the world, the kind that makes its way into LME warehouses. With Russia’s war with Ukraine intensifying, the threat of cancelled supply from Russia loomed large.

Thirdly, and most strangely, the world’s largest stainless steel producer Tsingshan and its charismatic high rolling boss Xiang Guangda had built a short position on the LME reported at over 150,000t.

As prices rose Xiang, known colloquially in China as Big Shot for his entrepreneurial nature love of the punt, faced margin calls to cover his shorts, bets on the price of nickel going down. With little nickel on the exchange to buy, prices soared to unthinkable levels as shorters tried to cover their asses.

Facing its biggest trading crisis since the tin market went bust in the 1980s, they were eventually saved by the LME which cancelled trades and introduced strict trading limits to restrict volatility.

At current prices upwards of US$30,000/t miners will be chuffed, not withstanding the strange and unfortunate circumstances surrounding the run.

Macquarie said in research late last month that the EV/EBITDA multiples of many miners “remain attractive on our forecasts and improve in a spot price scenario.”

Panoramic Resources (ASX:PAN), which recently restarted its Savannah mine in the Kimberley, is Macquarie’s preferred development play.

Mincor Resources (ASX:MCR) has also intersected first ore at its Cassini mine near Widgiemooltha, the first greenfields mine in years in the historic Kambalda nickel district.

Its ore will be used to restart BHP’s Kambalda nickel concentrator this quarter for the first time in four years.

“The company also discovered a new mineralised zone beyond the previous extent of the resource at Long through its recent underground diamond drilling,” Macquarie said.

“We note that current prices are trading 53% above our FY22 estimate while the upside to FY23E and FY24E is 58% and 69% at spot prices.”

Meanwhile juniors Ardea Resources (ASX:ARL) and Poseidon Nickel (ASX:POS) both got Federal support for projects around Kalgoorlie.

Mark Creasy, famed for his role in the Nova nickel and Bronzewing gold discoveries, boasted another win as Azure Minerals (ASX:AZS) announced a maiden resource of some 75,000t of contained nickel and copper for the Andover deposit in the Pilbara.

Creasy Group owns 40% of the JV, which Azure announced in mid-2020.

The 4.8Mt resource grades 1.11% nickel, 0.47% copper and 0.05% cobalt, but includes a high-grade component of 2Mt at 1.41% nickel, 0.49% copper and 0.06% cobalt.

Resource certainty is also high with over 80% of the resource classified in the indicated category, which provides enough confidence for mine planning.

Less impressive was Nickel Mines (ASX:NIC). The Indonesian nickel pig iron producer has bold plans to become the Fortescue of nickel, but its close links to Tsingshan saw sentiment in the miner take a big hit despite bold expansion plans on the horizon.

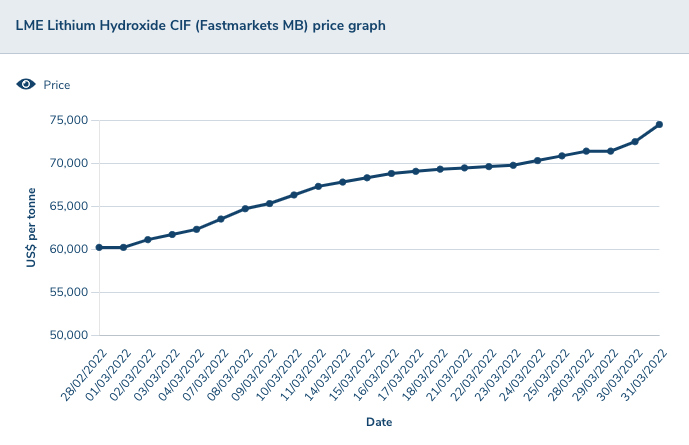

Price: US$74,200/t

%: +23.25%

Lithium, lithium, lithium.

If anyone thought the battery metal was at threat of demand destruction last month they haven’t paid attention to just how desperate electric vehicle and battery makers are to secure supplies.

Lithium carbonate prices didn’t come off slightly towards the end of last month in the order of around 1%, after outpacing lithium hydroxide prices at the start of the years.

Carbonate is more commonly used in cheaper lithium-iron-phosphate batteries that gathered market share last year in China as carmakers sacrificed range for affordability.

Hydroxide is generally the chemical of choice in traditional nickel-cobalt-manganese cathodes, which have longer range and are used in the Tesla Model 3.

Strong carbonate and hydroxide prices have spurred massive jumps in spodumene pricing, the ~6% pure concentrate produced by hard rock producers in Australia like Allkem (ASX:AKE) and Pilbara Minerals (ASX:PLS).

Spodumene prices have increased from US$400/t to US$5000/t in a little over 18 months, the equivalent according to PLS boss Ken Brinsden of a gold price at US$6000-7000/oz, three times their all time record from August 2020.

Fastmarkets MB reported a spot spodumene price even higher than that at US$5750/t on March 31. Allkem has already revealed it’s negotiating US$5000/t pricing for the June quarter.

For context, Pilbara Minerals’ unit costs for the first half of the year, when it made a maiden $114 million profit were just US$486/dmt. Its costs will rise, but nowhere near as fast as the price is.

At the start of March a host of mid-tier lithium explorers and developers moved into the ASX300 group of companies, a trigger for inclusion in index funds that can trigger heavy and high volume buying in stocks.

Then there’s just the overall exuberance in the lithium market, which has sent shares in miners AVZ Minerals (ASX:AVZ), Core Lithium (ASX:CXO), Lake Resources (ASX:LKE) and Sayona Mining (ASX:SYA) 53%, 76%, 147% and 153% respectively over the past month.

Firefinch (ASX:FFX) cleared the pathway to the development of its 50% owned Goulamina lithium mine in Mali. It banked US$170 million in funding from the deal with China’s Ganfeng which has now been completed, setting the scene for the demerger of the gold miner’s stake in Goulamina into new ASX-listed vehicle Leo Lithium.

Goulamina is expected to enter production in 2024, producing 506,000tpa in its first stage and up to 880,000tpa in its second stage expansion.

Firefinch, curiously, also became the subject of a rare LONG report from short selling research firm J Capital, which rose to prominence in the lithium research game for a controversial short report on geothermal lithium developer Vulcan Energy (ASX:VUL).

The FinTwit community was not happy with the boring outcome. It was a pleasant surprise for Firefinch holders though.

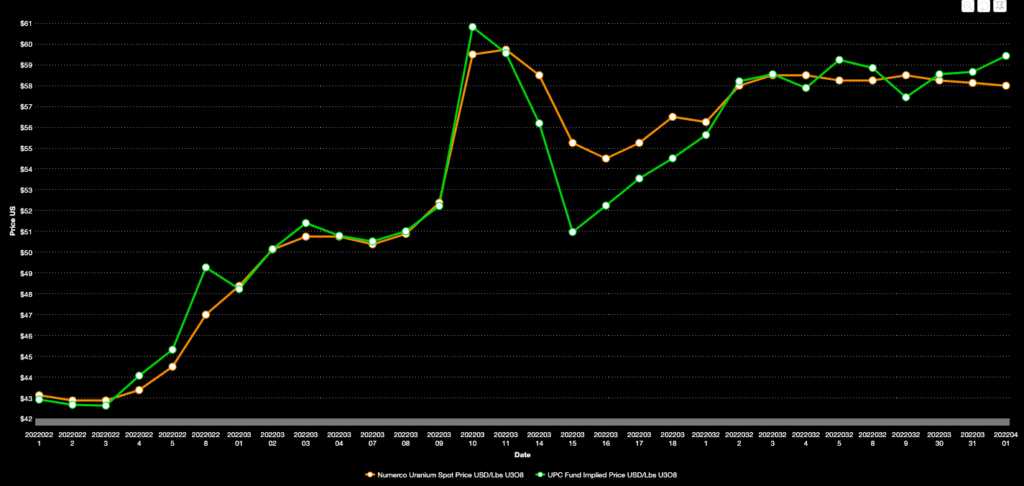

Price: US$58.13/lb

%: +23.68%

Uranium prices threatened to go south fast when Russian forces reportedly shelled Zaporizhzhia, the largest nuclear power plant in Europe and provider of 25% of Ukraine’s energy needs.

As fears of another Chernobyl emerged in the imaginations of the Twittersphere (drummed up by Ukrainian politicians hoping to twist Western arms) it turned out to be a false alarm. The fire was outside the reactors themselves.

Uranium stocks rebounded, then prices started to soar as the volume of uranium supply from Russia and friendly nations like Uzbekistan and Kazakhstan weighed on utilities in the west.

Spot prices briefly rose above US$60/lb, the level believed to incentivise new supply.

Term contract prices still need to catch up (and are less transparent than spot sales) but at US$58/lb to end the month, there is as much optimism in the yellowcake space now as there has been since the Fukushima incident in 2011.

On the last day of March an early Christmas arrived for uranium investors with not one or two but three major announcements.

Firstly Deep Yellow (ASX:DYL) announced a $658 million all scrip takeover had been endorsed by the board of Vimy Resources (ASX:VMY).

Led by former Paladin Energy (ASX:PDN) chief John Borshoff, the merged company will have $106 million in cash in the bank, with Vimy’s Mulga Rock development in WA likely to be the main focus along with Deep Yellow’s Tumas project in Namibia.

With a combined resource base of 389Mlbs, if both are developed the company – owned 53-47 by shareholders of DYL and VMY respectively – will have annual production capacity of up to 6.5Mlbs.

The same day the new Paladin announced a $215m equity raising, a new contract with a nuclear utility and concrete plans to restart the Langer Heinrich mine in Namibia by 2024, while Boss Energy (ASX:BOE) released a FEED study confirming a $113 million price tag for its Honeymoon uranium mine in South Australia.

An FID is expected soon.

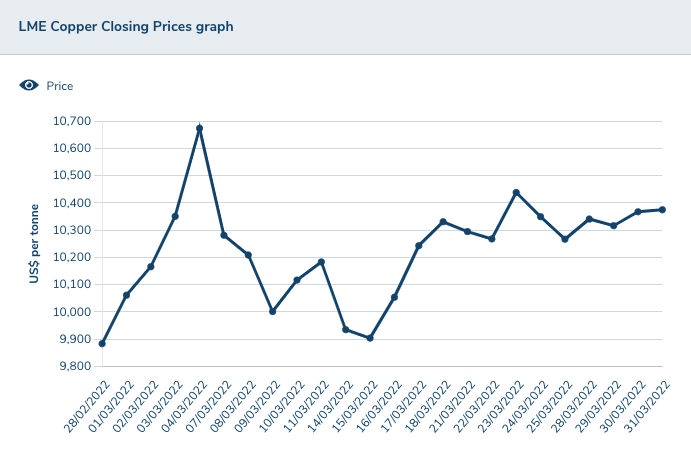

Price: US$10,375/t

%: +4.97%

A quiet month for Dr Copper, which ticked along silently while the rest of the world imploded in a molotov cocktail of volatility.

If it’s true copper can read the temperature of the global economy maybe it needs a bit of recalibration.

On the other hand, in these days and times it’s good to have some calm among the storm.

One of China’s largest producers Jiangxi Copper has warned prices could come off in the short term.

“The moderate slowdown in demand coupled with the gradual recovery of supply chain bottlenecks, the rising inflation globally is expected to gradually return to normal,” the company said after reporting a 142% increase in profits for 2021.

“At the same time, the weakening of stimulus policies, the decline of inventory cycle and high prices have suppressed demand. It is expected that commodity prices will fluctuate at a high level with a slight decline in 2022.”

But copper demand outlook is bullish due to the need for electrification infrastructure in the energy transition, a position shared by Jiangxi.

“In the long run, the supply growth is slow, and the global copper production cannot be effectively released in the next few years, and the risk of supply shortage increases,” Jiangxi said.

“While demand is likely to grow at a higher rate under the dual stimulus of economic recovery and dual carbon targets, resulting in an expansion in the lack of supply and demand, which will in turn lead to an increase in copper prices.”

US listed mining SPAC Metals Acquisition Corp has taken a major step to becoming a real boy, paying US$1.1 billion ($1.5b) to become the owner of Glencore’s CSA copper mine in New South Wales.

The Cobar operation pumps out around 50,000 tonnes a year and was put on the market last year amid heavy interest as copper prices surged beyond US$10,000/t.

Acquisitive battery metals miner IGO, which owns nickel and lithium mines in WA, had revealed itself as the preferred bidder for the mine, which has been in operation since 1967, about a month ago.

But it dumped the deal after shareholders voted with their feet, sending its shares tumbling.

Metals Acquisition Corp, which is backed by resources heavyweights in former Northern Star boss Bill Beament and ex FMG head honcho Nev Power, was always rumoured as the other major chance.

At the smaller end of the market Eagle Mountain Mining (ASX:EM2) raised an impressive $16 million to fund exploration and the recommissioning of the historic underground mine at the Oracle Ridge mine in the USA.

That deal included a $1m investment by managing director Charles Bass and came after a resource upgrade which included a 36% increase in copper metal to 17.0 Mt at 1.48% Cu, 15.09g/t Ag and 0.17g/t Au for 251,000t of contained copper, 8.2Moz of silver and 93,000oz of gold at a 1% Cu cut off.

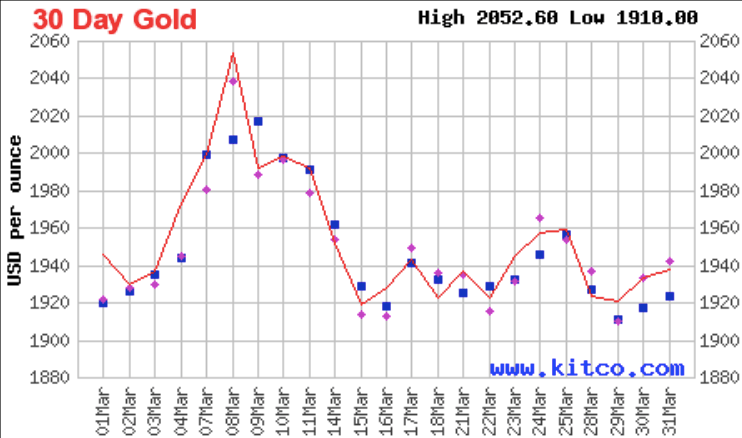

Price: US$1949.20/oz

%: +2.62%

Gold prices swung up and down throughout the month of March as global instability powered them to high levels above US$1900/oz.

In the end they remained close enough to even for the month, but the war in Russia and ongoing pandemic now has analysts and banks bullish on gold despite the first of an expected 7 rate hikes last month from the US Fed.

ANZ’s guarded gold outlook is turning positive, with the Big 4 banks now expecting prices staying above US$1900/oz in 2022.

“We have held a cautious view on gold and the precious metal sector on the premise that tighter financial conditions would see investor demand wane,” says Daniel Hynes, senior commodity strategist at ANZ.

“However, higher than expected inflation and the subsequent negative real interest rates will provide strong support to the sector.

“Much of this is based on the upheaval in the energy sector amid the Ukraine war.”

Gold’s status as a safe-haven asset has shone brightly over the past month as the war in Ukraine dominates headlines.

“Among safe-haven assets, gold has been the outperformer since beginning of this year,” Hynes says.

The broader isolation of Russia will see a structural shift in the energy sector, which will be inflationary, Hynes says.

There is also a higher risk of weaker economic growth, particularly in Europe.

“This should create a positive backdrop for investor [gold] demand,” he says.

“As such, we see the gold price staying above USD1900/oz, despite the prospects of an aggressive rate hike cycle by the Fed.”

Westgold Resources (ASX:WGX) revealed the impact of WA’s belated affair with Covid-19 absenteeism.

It lost 3860 hours or 320 shifts among its workforce onsite at its 250,000ozpa Mid West mines in just 30 days.

Westgold expects to lose 3-4% of production for the quarter, with over 5000 hours of work lost when offsite cases and close contacts are included.

Meanwhile, former mid-tier gold boss Raleigh Finlayson has set his sights on doing it all again at Genesis Minerals (ASX:GMD) after settling into his new role as MD of the junior gold explorer.

Genesis announced a 25% increase in JORC 2012 compliant resources to 2Moz last week before Finlayson launched a rebrand and strategy update he has branded Genesis 2.0.

In fact, it looks, smells and walks a lot like Saracen 2.0, with many of the same personnel and targets.

Finalyson’s aspiration to fill the $5 billion value gap to the three ASX100 listed gold miners with 300,000ozpa, two mines and a seven-year mine life would pretty much put him where he was with his former company Saracen back in 2017.

There is the promise of some tasty opportunistic M & A, so watch this space.

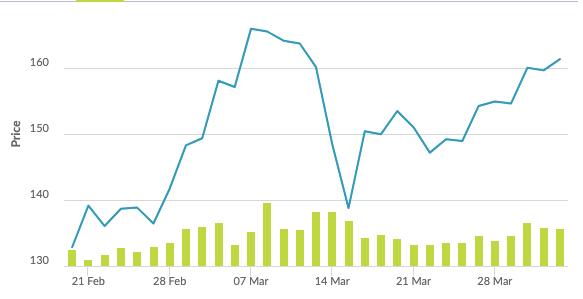

Price: US$159.80/oz

%: +15.72%

Iron ore prices continue to defy weak Chinese economic data on the expectation Chinese stimulus measures will support the world’s largest steel industry through the second half of the year.

Prices were knocked down by Communist Party intervention in February but roared back after the end of the Winter Olympics and Paralympics, a key milestone for the easing of environmental controls.

Mill capacity utilisation rose through the end of March, but a new threat to iron ore and steel demand emerged, Covid lockdowns across China including in the steel hub of Tangshan and financial centre of Shanghai.

Despite those ructions, traders in futures markets have been bullish, helping stir iron ore prices to a tick under US$160/t by the end of March.

China set official growth targets of 5.5% for its economy this year. Iron ore traders are betting that after a slow start to 2022 and amid weakness in its property sector, China plans to ramp up the activity in the months to come.

Indeed, iron ore prices and sentiment in futures (Singapore hit US$163/t yesterday) continue to climb despite weak manufacturing index data from both the People’s Bank of China and the independent Caixin index in the past week.

Steel prices have been driven higher, especially in Europe and the USA, due to the impact of the conflict on supplies out of Ukraine and Russia. But expectations around China are driving the price right now.

Is there downside here? RBC’s Tyler Broda thinks so.

“Iron ore has been stronger than expected in Q1 with prices averaging $141/t vs. our $130/t forecast, but with prices now at ~$160/t and successful stimulus needed to support prices, we are seeing increasing risk around a rollover in Q2 (RBCe $115/t),” he said.

“Longer-term we continue to expect that iron ore is moving into a structural surplus, and depending on the availability of Ukrainian production (which continues to ship) the crossover could come as early as the end of Q2.”

Year average iron ore prices are now 28% higher than the US$110/t average in the December quarter and well above analysts’ previous estimates.

Macquarie remains bullish on prices and the iron ore sector, with all of its picks bar Fortescue Metals Group (ASX:FMG) in outperform territory.

That’s a list that includes BHP (ASX:BHP), Rio Tinto (ASX:RIO), Champion Iron (ASX:CIA), MinRes (ASX:MIN) and Mount Gibson Iron (ASX:MGX).

With prices already in line with Macquarie forecasts the bank thinks there is limited upside over the next six months, but BHP’s earnings potential in FY24 and FY25 contains 147 and 158% upside respectively while Macquarie thinks Rio has upside to improve to 99% and 107% in the same years.

Rio Tinto dominated the iron ore news cycle in recent weeks with its off-again, on-again dance with the Guinean Government over the development of its portion of the Simandou iron ore mine in the West African nation.

Rio, its partner Chinalco and the operator of the other blocks at the high grade iron ore deposit, SMB Winning Consortium, worked quickly to get a deal in place with Guinea’s military junta after it suddenly halted work.

Unsurprisingly, the post Coup government wound up with more after the negotiations were complete.

Speaking of high grade a trio of juniors, including the operating Grange Resources (ASX:GRR) put some numbers around magnetite operations in WA and South Australia last month.

Macarthur Minerals (ASX:MIO) released a feasibility study on its proposed Lake Giles magnetite mine in WA’s Yilgarn iron ore province.

Meanwhile Magnetite Mines (ASX:MGT) released an expansion study on the potential future extension of its 3Mtpa Razorback mine into a 7Mtpa exporter of ultra high grade magnetite concentrate.

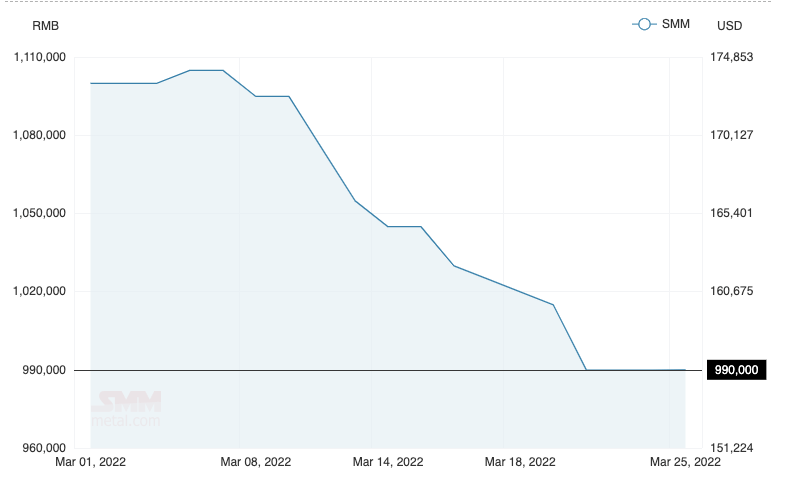

Price: US$150.63/kg

%: -13.92%

NdPr prices fell for the first time this year late in the March quarter, after Chinese authorities told the three largest players in its domestic market China Rare Earth Group, China Northern Rare Earth Group and Shenghe Resources to regulate their operations to prevent hoarding and market speculation.

It’s a common tactic China has wheeled out to try dull prices in everything from iron ore to lithium and now rare earths.

Despite its claims market fundamentals and do not match up, there’s plenty of evidence to suggest downstream demand for rare earths remains strong.

“Downstream sectors like new energy vehicles, wind turbines demonstrate strong demand, and large-scale magnetic material enterprises have been flooded with long-term orders,” Shanghai Metals Market analysts said.

“The four major magnetic material companies are expected to expand their production capacity by 29,000 mt (metric tonnes) in 2022, generating demand for at least 7,800 mt of praseodymium and neodymium (PrNd) alloy.”

Prices of neodymium-praseodymium oxide quoted by the SMM fell from US$175/kg to a tick over US$150/kg over the month, still driving massive profits for sellers.

Despite the dip in prices, the SMM say rare earths producers in China, home to more than 80% of the global supply chain remain bullish about the state of the market.

Canberra is going big on so called “critical minerals” including $2 billion in its 2022-23 budget to support the delivery of new energy metals supply chains in Australia.

Arafura Resources (ASX:ARU) was one of the beneficiaries, locking up a $30m modern manufacturing initiative grant from the Feds for its $90.8m Nolans rare earths separation plant.

Sector leader Lynas (ASX:LYC) which last month received final approvals for its Kalgoorlie cracking and leaching plant and revealed the results of a 1km long diamond drill hole at its world class Mt Weld mine near Laverton.

That revealed a 1020m long intersection at an average 2.22% rare earth oxide, suggesting a large addition to the mine life at Mt Weld could be on the cards to support its expansion plans.

At the junior end of the market RareX (ASX:REE) locked up $10 million in funding via an institutional placement to support drilling at its Cummins Range rare earths project, later announcing a host of results showing evidence of primary mineralisation from drilling last year at the project, including 21.9m at 1.7% TREO with an interval of 6.4m at 3.5% TREO.

A new resource expansion drilling program is due to start this month. Projects like RareX’s could have a smoother development path as well after Iluka Resources (ASX:ILU) announced it had made a final investment decision to develop its Eneabba rare earths refinery 300km north of Perth after the end of the month.

The Federal Government will provide a $1.05 billion loan to support the development, where Iluka will firstly process high grade monazite stockpiles from Eneabba before developing its Wimmera mine in Victoria’s Murray Basin and taking third party concentrate from other Aussie miners.

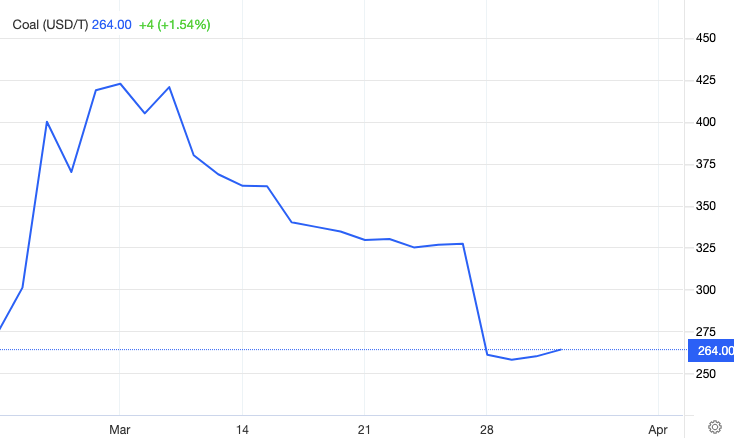

Price: US$264.00/t

%: -3.83%

Coal prices fell month on month but that hardly tells the full story.

Thermal coal from Australia charged to the US$450/t territory as buyers turned their back on Russian coal, sending prices to their highest level in real terms in 200 years according to Rystad Energy.

That left a big void in the market, particularly Europe which is heavily reliant on Putin for its energy resources.

The issue is supply is so tight in Asia, the main seaborne market for thermal coal it is virtually impossible to replace Russian tonnes.

By the middle of March coal prices tracking for a gain of 65% for the month.

But prices subsided as energy sanctions did not come as hard as the market was expecting and China dramatically ramped up production of domestic coal, with figures showing it is tracking to produce as much as 500Mt more in 2022 than it did in 2021.

Some classes of metallurgical coal surged to as high as US$670/t during the month as supplies of the steelmaking material remained barren and finished March at around the US$520/t mark, forcing forecasters to lift their end of year predictions.

Even PCI coal, traditionally a discount product, were in line with prices for premium hard coking coal, fetching as much as US$645/t.

PCI coal is one of the products heavily supplied to the European market by Russia.

Indonesian backed minnow Stanmore Coal (ASX:SMR) has virtually wrapped up the ambitious purchase of its remarkably well timed purchase of BHP’s BMC coal mines.

Majority owned by the Widjaja family dynasty, Stanmore offered 5.6 times its market cap to ink the US$1.2 billion ($1.6b) deal with BHP last year.

In March Stanmore locked up $694m in funding in a retail entitlement offer and institutional placement which, backed by debt, should be enough to secure the transaction which will deliver Stanmore an 80% operating stake in Queensland’s Poitrel and South Walker Creek mines.

The operations produce semi-soft and PCI coking coal for steelmaking, two products considered “lower quality” by BHP but which are now fetching big bucks thanks to the exodus of Russian tonnes from the market.

Over in America coal miners are also enjoying strong pricing.

Allegiance Coal (ASX:AHQ) released its half-year results in March, saying it plans to hit a 1Mt sales run rate by June 30.

The ASX-listed US focused coal miner has been working on the ramp up of its New Elk and Black Warrior mines over the past year, making $13m in revenue on 91,000t of coal sales with a loss of $27m before interest and depreciation in the six months to December 31.

But it is the next year ahead which will be more telling for Allegiance, with 415,000t of sales and US$90 million in revenue expected across the second half of the financial year after meeting quality requirements to upgrade its sales to the premium High Vol A index.

The latest example of profitability of coal miners came from $2.65 billion capped New Hope Corp (ASX:NHC), which swung from a $55.4m loss in the first of 2020-21 to a $330.4m profit through the first half of 2021-22.

The profit will power ~$250 million of payouts to shareholders, 17c through New Hope’s interim dividend and 13c in the form of a special dividend.

The company has built an enviable cash pile of $513m and undrawn debt of $420m after paying off the $310m debt it held at the end of July last year, as realised prices soared from an average $77.98/t last year to $192.38/t in the six months to January 31.

It followed a number of its peers in returning to profit and dividend payments, including Coronado (ASX:CRN), Yancoal (ASX:YAL) and Whitehaven Coal (ASX:WHC), the latter of which will bank at least some of its revenue from the taxpayer in the March quarter after selling an emergency 70,000t cargo of energy coal to Ukraine (valued at $31.7m at market prices at the time) via the Commonwealth Government.

Silver

Price: US$24.88/oz

%: +1.34%

Tin

Price: US$42,910/t

%: -5.12%

Zinc

Price: US$4173.50/t

%: +12.16%

Cobalt

Price: $US82,000/t

%: +9.25%

Aluminium

Price: $3491/t

%:+3.63%

Lead

Price: $2416/t

%: +1.21%

Mining

Mining

News

Get the latest Stockhead news delivered free to your inbox.