Investors in the insanity of the post-Covid market have become accustomed to the idea that stocks only ever go up, but after a nearly unparalleled rise in commodity prices across virtually every metal over the past six months, something had to give.

It came in the form of China’s slowing economy as Covid lockdowns poured cold water on its lower than usual but still ambitious 5.5% 2022 economic growth target.

Sprinkle in a bit of jawboning (the Community Party doing their version of the Jimmy McMillan bit, yelling THE PRICE IS TOO DAMN HIGH) and the clear-out across a wave of commodities can be partially explained.

The good news for investors is it could just be a breather, especially after the uber-inflation we saw in February and March as major energy and metals exporter Russia first stationed troops along the Ukrainian border then sent them in to wage war on its neighbour.

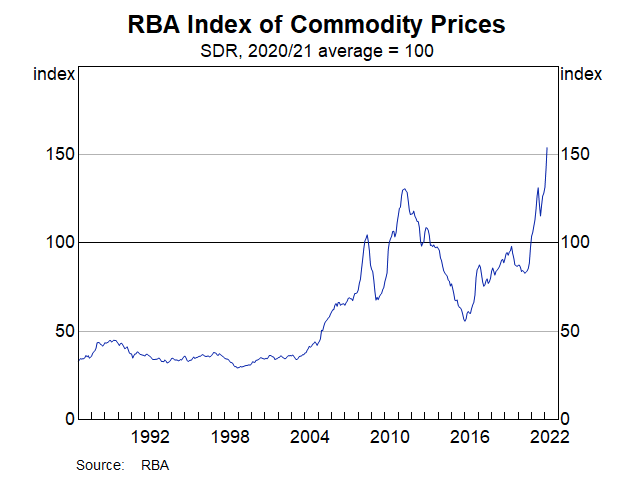

On the other hand, commodities have long been frothy. The Reserve Bank’s Commodity Price Index is as high as it’s ever been, up 1.7% in April after a mad 7.2% run in March.

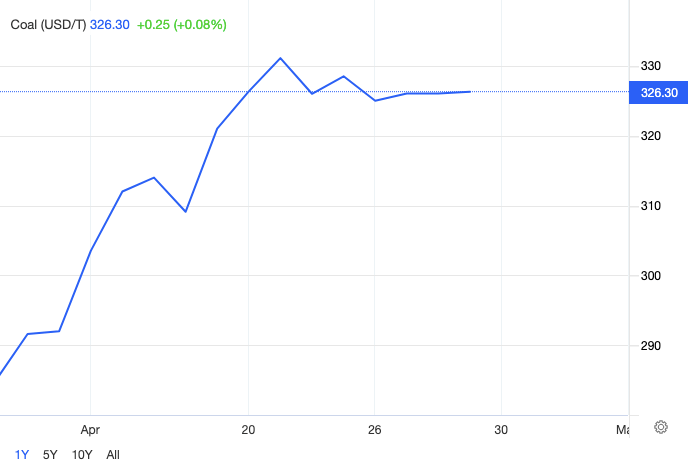

That is despite it sending premium hard coking coal prices briefly to US$670/t in March and inflating the normally discounted PCI coal price due to Russia’s outsized role in Europe’s supply of that product.

Prices nosedived back to still historically healthy levels of US$264/t for thermal coal and around US$380/t for met coal by the end of March but have caught a second wind. Thermal coal prices climbed almost 25% in April, while PHCC FOB Dalrymple Bay was fetching almost US$520/t on Friday according to price reporters Fastmarkets MB.

Ludicrous stuff. Expect the big earnings to come from the Aussie coal crew.

Commbank mining analyst Vivek Dhar said replacing Russian coal will be hard for Europe, Japan and South Korea, which collectively import around 90Mt of thermal coal and 25Mt of met coal annually from Putin’s Russia.

“Even taking into account some additional purchases of Russian coal by India and China, the rise in coal prices indicate market concerns that it will be very challenging for OECD nations to replace their coal imports from Russia,” he said in a note.

“There is simply very limited spare capacity in thermal and coking coal markets.”

Pic: Trading Economics

LOSERS

Lithium (sorta)

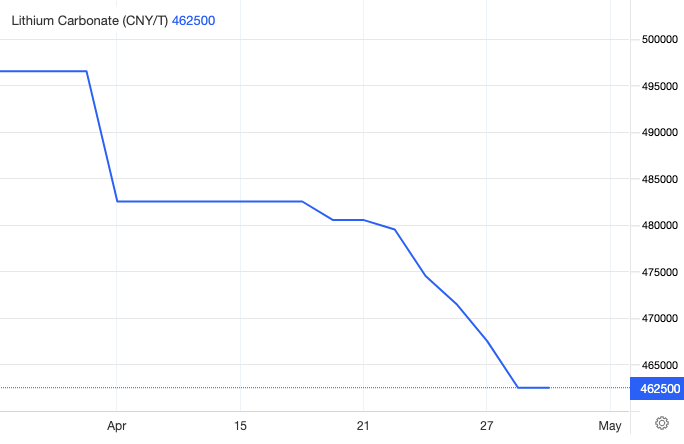

Price (Lithium Carbonate): US$69,988/t %: -5.67%

Supercharged lithium prices, the source of one of the most remarkable investment bull markets in recent years, have taken what’s been referred to by those in the industry as a “breather”.

Or have they? While prices have been sliding from record levels in China for lithium carbonate, one of the two main lithium chemicals used in electric vehicle batteries, lithium hydroxide chemical prices and spodumene prices have held firm.

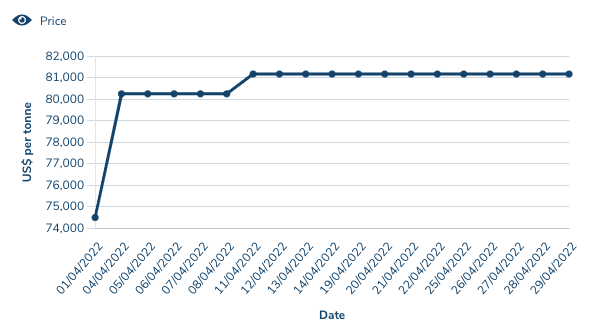

Spodumene, the ~6% rich lithia concentrate produced by hard rock miners in Australia, is fetching record prices of US$5750-6300/t, while Pilbara Minerals (ASX:PLS) last week sold a shipment at auction for US$5650/dmt.

Its retiring boss Ken Brinsden reckons margin will sit with the miner for years to come, saying that raw materials and the underinvestment in new lithium mines are the biggest bottleneck in the electric vehicle supply chain.

Lithium carbonate prices have eased in China. Pic: Trading EconomicsBut Hydroxide has picked up the pace. Pic: LME/Fastmarkets

Uranium

Price: US$53/lb %: -8.82%

Uranium prices briefly touched multi-year highs after the March quarter ended on one of the most jubilant days in Australia’s yellowcake sector in years.

Spot prices, probably inflated by Sprott’s activity in the small uncontracted market and Russia’s war in Ukraine, have since cooled.

But major banks are starting to up their long-term price forecasts as supply shortages emerge and governments thaw their frosty attitude to nuclear power amid surging fossil fuel prices.

Bank of America Merrill Lynch upped its price estimates for 2022-2027 by 20% last month.

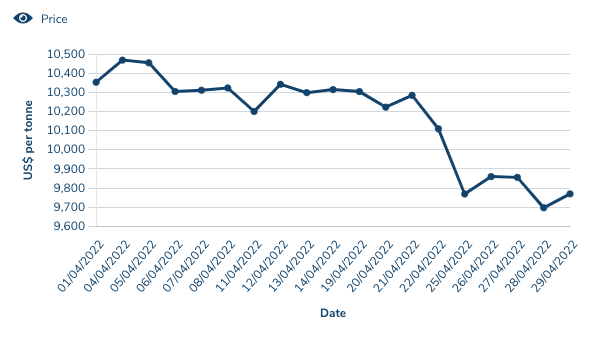

Nickel was the most talked about metal of March, surging to US$100,000/t briefly in two hours of trade that broke the LME nickel market and shone an unwanted spotlight on high-rolling Chinese nickel executive and stainless steel entrepreneur Xiang Guangda.

Xiang, known colloquially as “Big Shot” was believed to be the short seller whose bet with steel giant Tsingshan on a 150,000t short position spectacularly backfired when the threat of sanctions against Russia sent prices out of control.

Nickel is back in more comfortable territory, trading roughly sideways at very high levels of over US$30,000/t across the month.

That will provide some confidence to miners its run higher has more fundamental support behind it in the form of low warehouse supplies and skyrocketing demand from EV and battery makers.

Longtime industry participants say prices of US$15/lb, around double those factored into most economic models, could support new nickel sulphide producers. New sources of nickel are sorely needed to fill the supply gap emerging in battery grade product as the energy transition picks up.

“There’s definitely a shortage of class one, high-quality sulphide nickel, that’s for sure. So users will need to source high-quality nickel from elsewhere, because existing mines just can’t supply enough.”

Nickel prices have been stable after a crazy March. Pic: LME

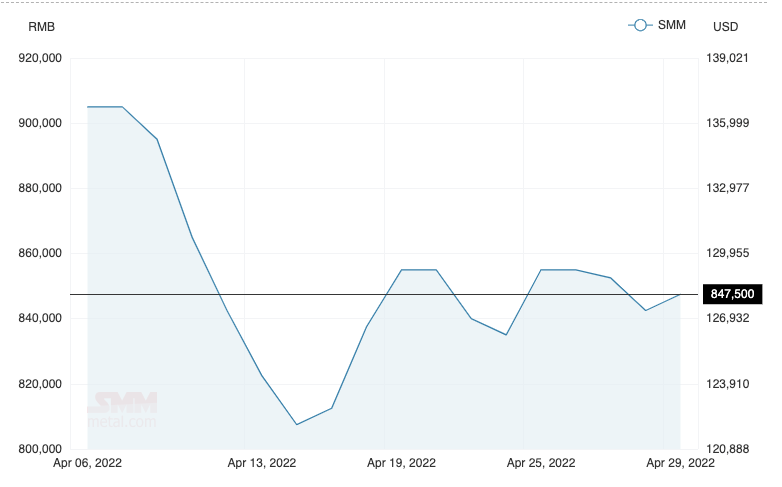

Rare Earths (NdPr Oxide)

Price: US$128.24/kg %: -14.86%

Like lithium, rare earths were another commodity market that seemed like it could run forever until China intervened.

Both calls for price moderation from the Chinese Government and Covid have kept a lid on prices, with prices quoted on the Shanghai Metals Market of neodymium-praseodymium oxide and other rare earths posting major falls for the second straight.

Rare earths are a collection of 17 uncommon elements used in a range of applications, with massive demand growth from their use in the permanent magnets essential to EVs and wind turbines.

More than 85% of the supply chain is based in China, which has seen massive government support for new downstream processing projects in Australia.

While NdPr prices have cooled down somewhat after hitting highs of US$175 per keg in February, the market leader outside China, ASX-listed Lynas Rare Earths(ASX:LYC), reckons the market is as undersupplied as ever.

“The fundamentals will remain strong. And who would have thought that we’d be looking at US$130/kg and saying ‘oh gosh, isn’t the price a bit soft?'” Lynas managing director Amanda Lacaze said on a quarterly call.

NdPr prices have fallen for the second month straight. Pic: Shanghai Metals Market

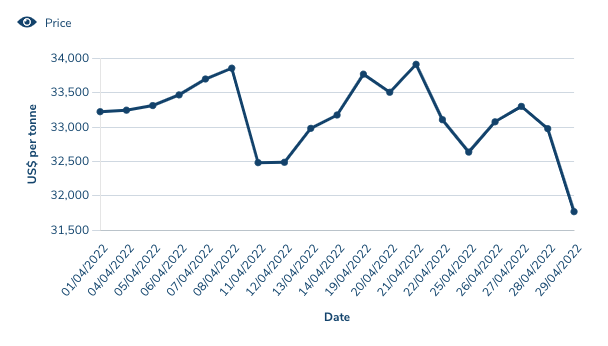

Copper

Price: US$9770/t %: -5.83%

MMG’s Las Bambas mine in Peru, one of the world’s largest copper producers with a capacity of over 400,000tpa, has been halted for over a week after Indigenous communities around the mine began camping at the site in protest.

That should provide support for copper on the supply side, especially with BHP lowering guidance from it and Rio Tinto’s giant Escondida mine in Chile in its recent quarterly review.

Alas, copper is one of the commodities most driven by Chinese industrial growth, and sentiment in the red metal has been knocked by the slowdown in economic activity from China’s wave of Covid lockdowns.

With prices still in touching distance of US$10,000/t they remain very healthy for producers. Sandfire Resources (ASX:SFR) enjoyed those fruits with a strong shareholder reaction to its latest quarterly results.

Those prices have also made assets in the copper space hot property. Bill Beament and Nev Power’s Metals Acquisition Corp SPAC paid over US$1 billion for Glencore’s 50,000tpa Cobar copper mine recently.

That was followed last week by Aeris Resources (ASX:AIS), which announced a $234 million cash and share deal with Washington H. Soul Pattinson to secure its Round Oak Minerals business, owner of the Jaguar mine in WA and Barbara mine near Cloncurry in Queensland.

Sandfire boss Karl Simich says copper will remain in high demand going forward.

“CRU estimates that an investment of over US$100 billion will be needed if the world is going to meet soaring global demand for copper,” he said.

“The outlook for many other metals is similar, with zinc (which accounts for around 26 per cent of our revenues from MATSA) rising to the highest level since 2006 and inventories falling to historically low levels.

“All of these macro developments provide a very powerful backdrop to Sandfire’s growth strategy, with a rising production profile being delivered into historically strong metal markets.”

Copper prices have drifted down despite tight supplies. Pic: LME

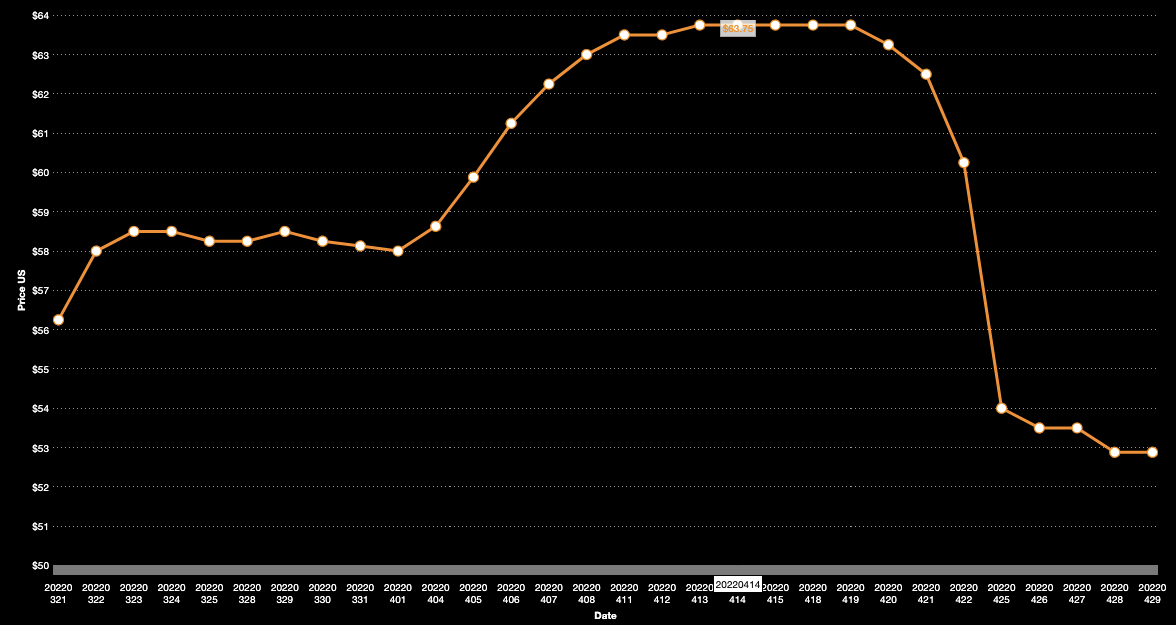

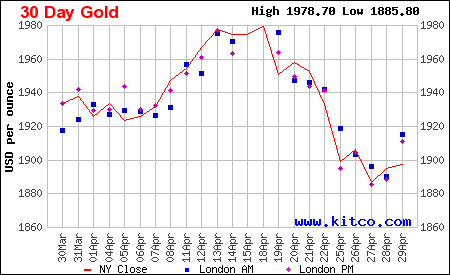

Gold

Price: US$1897.28/oz %: -2.66%

Gold buying is on the rise, with investors flocking to the safe haven asset amid geopolitical uncertainties and decades high inflation.

Net buying by central banks more than doubled from the previous quarter, adding over 84t to official gold reserves during Q1 2022, dominated by countries such as Egypt and Turkey.

While 29% lower than Q1 2021, central banks continue to value gold’s performance during times of uncertainty, WGC senior analyst Louise Street says.

“The first quarter of 2022 has been a turbulent one, marked by geopolitical crises, supply chain difficulties and surging inflation,” she said.

Still gold prices struggled to break resistance in the US$1900/oz range in April. Sentiment for gold miners was not helped in a March reporting best described as a series of unfortunate events.

Many hit by Covid and labour shortages struggled with costs and guidance, with Silver Lake Resources (ASX:SLR) spectacularly pulling its production targets just one quarter from the end of the financial year.

The threat of interest rate rises is also coming, both from major banks like the US Fed and our own Reserve Bank.

Rate rises are typically bad news for gold miners, though wild inflation figures could yet keep real rates negative.

“The market is expecting the Fed will hint at two or more 50bps hikes to tame inflation,” ANZ’s David Plank said.

“This comes as the personal consumption expenditure index advanced 0.9% from a month earlier and 6.6% from March 2021.

“A respite in the rally in the USD saw gold recover some of those losses later in the week. Nevertheless, the prospect of strong safe-haven demand remains high.

“According to World Gold Council report, gold ETF flows of 269t were strongest since Q3 2020 and total demand rose by 34% y/y to 1234t.”

Gold has swung high and low over the last month. Pic: Kitco

Iron Ore (62% Fe)

Price: US$144.95/t %: -8.93%

Iron ore prices have been kept in balance by two equally strong forces in 2022 so far, after sentiment around China’s economic growth plans drove prices way above consensus around US$158/t by the end of the March quarter.

On one hand, China’s lockdown and talk of reducing steel output in 2022 have prevented prices from heading towards the crazy records of more than US$230/t we saw in May last year.

But very weak export performances from the majors are keeping them from dropping back down to the lows of under US$90/t we saw late last year.

BHP, Rio Tinto and Vale all disappointed with their production numbers in the March quarter.

Fortescue Metals Group (ASX:FMG) on the other hand upgraded guidance. But its main growth project, the 22Mtpa Iron Bridge magnetite mine in the Pilbara, has been delayed to March next year.

While iron ore bosses are often hesitant to make predictions on iron ore prices, outgoing FMG boss Elizabeth Gaines is confident China’s economic growth target will support steel and iron ore demand.

“We’re focused on the GDP growth target of five and a half per cent for this calendar year,” she told media on a conference call last week.

“We think that that is supportive of steel demand more broadly and I think encouragingly in March, as I mentioned earlier, we saw crude steel production reach that annualised rate of over a billion tonnes.

“There’ll be further investment in property and infrastructure, all of which is supportive of steel demand and therefore demand for iron ore.”

One interesting trend has been the relatively recent contraction of the spread between prices for benchmark 62% iron ore fines and low grade 58% fines.

Low grade iron ores have risen in value relative to the benchmark. Pic: Fastmarkets MB

Get the latest Stockhead news delivered free to your inbox

For investors, getting access to the right information is critical.

Stockhead’s daily newsletters make things simple: Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.

I want the news:

Hear it first

Get the latest Stockhead news delivered free to your inbox.

Thanks! You’re subscribed, Stockhead news is coming your way soon.