As 2020 comes to an end, so too has one of the more drawn-out company takeover sagas seen in Australia in recent times – that of Cardinal Resources.

A nine-month battle for control of the dual-listed, West African-focused gold explorer Cardinal (ASX:CDV) has finally come to a close this week, when Chinese state-owned company Shandong Gold picked up enough acceptances for an unconditional off-market takeover.

Shandong fought off a competing bid from London-based Nordgold, backed by Russian steel billionaire Alexey Mordashov, which withdrew from its planned Cardinal takeover after a lengthy pursuit which began back in March (!) of this year.

The conclusion of the bidding war must come as some comfort to Cardinal shareholders, many of whom have waited patiently as the prospective buyers duked it out with rival offers which drove the share price up from as low as 25c in March to a peak of $1.10 in October.

The ultimately successful takeover offer from Shandong came in at $1.075 per share – a 237.5% increase from the start of the year and significantly higher than its initial offer of 60c in June.

How did it get there? Here’s a rundown of events – you may need it:

On March 16, Nordgold acquires a 19.9% stake in CDV, and makes an informal offer to buy all the company’s remaining issued capital for 45.775c per share.

On June 18, Shandong Gold enters the conversation with a takeover offer worth 60c per share – a 31.1% premium to Nordgold’s offer. The board of Cardinal recommends this offer in the absence of a superior one, and a bid implementation agreement is entered.

The superior offer then comes from Nordgold on July 15 – an unsolicited on-market takeover offer worth 66c per share. Cardinal shareholders are told to take no action and notes its obligations under the agreement with Shandong.

On July 22, Shandong ups its offer for Cardinal to 70c per share. The revised offer is recommended by the CDV board ahead of the Nordgold offer.

On September 2, Nordgold increases its offer for Cardinal to 90c per share. Cardinal advises its shareholders not to take action, again referring to its bid implementation agreement with Shandong.

On September 7, Shandong ups its bid for Cardinal to $1 per share – its “best and final” offer. This is again recommended by the Cardinal board.

On September 15, the Cardinal board publicly accepts the Shandong takeover offer of $1 per share.

Both the prospective acquirers then extend their offer period repeatedly, until…

You guessed it. Nordgold matches the offer of $1 per share not already held in Cardinal on October 21. Shareholders are again advised to take no action.

On October 23, Shandong clarifies its “best and final” offer comment, stating that it would not increase its offer price unless there was a higher competing offer for Cardinal shares.

On October 26, Nordgold also says it won’t increase $1 per share offer unless there’s a higher competing offer. It then issues a statement two days later, criticising Shandong for suggesting a third bidder may emerge for Cardinal.

A third party emerges on November 18, when Ghana’s Engineers & Planners Company Ltd (E&P) offers $1.05 per share. Shareholders are told by the Cardinal board to take no action.

Nordgold issues a statement on November 24 in which it claims the E&P bid does not constitute an offer due to a lack of written terms, no means of acceptance by Cardinal shareholders, and terms inconsistent with the requirements for an off-market bid.

That same day, Shandong increases its bid for Cardinal to $1.05 per share. The board recommends shareholders accept this bid.

On December 11, Nordgold matches Shandong, and ups its bid to $1.05 per share. Shareholders are told to take no action.

On December 22, Shandong increases its offer to $1.075 per share subject to it acquiring a relevant interest in at least 30% of Cardinal shares by December 31 and Nordgold not extending its takeover offer past December 23.

On December 24, Nordgold announces it has accepted Shandong’s offer and withdraws from the race.

But wait, there’s more!

A fourth bidder emerges on Christmas eve – Dongshan Investments swoops in with an off-market offer of $1.20 per share subject to a series of conditions.

But Dongshan enters the race too late, and later that same day Shandong Gold acquires control of Cardinal by taking its shareholding above 50%.

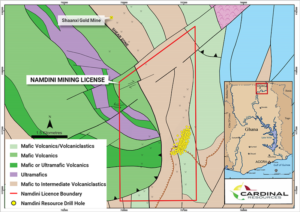

Their prize? Cardinal’s highly prospective gold assets in Ghana. The jewel in the crown is the Namdini gold project, adjacent to the Chinese-owned Shaanxi gold mine.

A feasibility study on the project outlines an ore reserve of 5.1 million ounces.

The prize: The Namdini mining lease in Ghana. Pic: Supplied

But the real winners are surely those CDV shareholders with the patience to see out almost a year of back-and-forth from companies with interests across five continents.

In exchange, they witnessed 237.5% share price appreciation over the course of 12 months. Not a bad way to end a tumultuous year.

It may seem messy, but as we head into 2021 there will be plenty of investors in search of the next Cardinal Resources.

Get the latest Stockhead news delivered free to your inbox

For investors, getting access to the right information is critical.

Stockhead’s daily newsletters make things simple: Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.

I want the news:

Hear it first

Get the latest Stockhead news delivered free to your inbox.

Thanks! You’re subscribed, Stockhead news is coming your way soon.