Pic: claffra/iStock via Getty Images

Russia’s invasion of Ukraine has shone a spotlight on palladium and platinum supplies. What does the future hold?

Mining

Pic: claffra/iStock via Getty Images

Mining

Platinum group elements or PGMs are essential metals in the modern world, but until recently they’ve been an obscure investment in the Australian market.

The group of six metals, especially the major three in platinum, palladium and rhodium, are prized for their catalytic qualities.

They are key components in the fuel efficiency converters that help auto vehicles with internal combustion engines follow modern emissions standards.

Their anonymity has faded for a few reasons. One, Chalice Mining (ASX:CHN) shot to fame by making the first major PGE discovery, the palladium rich Julimar project 70km north of Perth in 2020, inspiring a rush of explorers into the district and commodity class.

Secondly, new applications linked to the green energy transition have emerged, including the role of PGEs in fuel cells and electrolysers that use renewable energy to convert water into so-called “green hydrogen”.

Then there is Russia’s dominance in the world palladium market. It produces about 40% of the world’s mined palladium, with South Africa close behind and a big gap to third place.

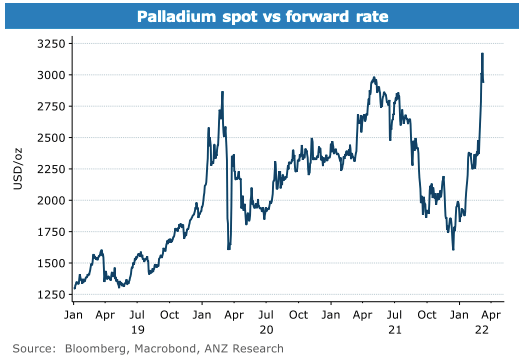

As sanctions and boycotts against Russia have expanded since its invasion of Ukraine on February 24, palladium prices have risen to all time highs of a touch under US$3500/oz on supply fears.

Back under US$3000/oz after the London Platinum and Palladium Association said it would keep Russian refiners off its no-go list, prices remain close to the previous ATH set last year in anticipation of a post-pandemic recovery in auto demand.

Palladium and its sister metal rhodium are largely used in standard gasoline cars, with the bulk of the metal being sold to makers of catalytic converters.

Platinum is typically the metal of choice in diesel cars, and has large side markets as an investment asset and in jewellery.

All up annual global demand for palladium is around 10.5Moz, platinum 7.5Moz and rhodium, which is currently trading in excess of US$20,000/oz, 1.2Moz.

According to Johannesburg based PGE mining expert Johan Odendaal, around 7Moz of palladium, 6Moz of platinum and 700,000oz-800,000Moz rhodium is mined annually with catalyst recycling making up a large part of the shortfall.

Even before the Russian invasion of Ukraine, he said the market was looking at supply shortages from 2023 onwards.

“That outlook in terms of supply and demand was before the situation that developed now in Ukraine and sanctions being applied to Russia,” he said.

“So certainly I think going forward, depending on what’s going to happen with sanctions, there could be a significant short supply of palladium in the market.

“If we look at at Russian supply of palladium, in particular, a large percentage of that goes to China. So at least some of that material will find its way into normal demand. But still, if you look at the remaining remaining 50% I’m not sure how that is going to be handled.

“It’s a large chunk of metal that you’ll have to find other alternative supplies somewhere, I don’t think there’s enough in stockpiles.”

Platinum remains oversupplied, according to the World Platinum Investment Council. While palladium is paying US$2829/oz yesterday, platinum was fetching US$1098/oz.

But Odendaal says that could that gap could close.

“I believe it will lead to an increase in thrifting away from palladium into platinum. And I think what we’re going to see is certainly the platinum price picking up in the next year.”

Odendaal is the managing director designate of unlisted Southern Palladium, which is looking to capture these tailwinds by revisiting a forgotten but substantial PGE deposit in South Africa’s Bushveld Igneous Complex, the Bengwenyama project.

The Bushveld Complex is the largest source of magmatic ores in the entire world with an areal extent of 66,000km2 of igneous rocks formed 2.1 billion years ago.

It is the largest source of platinum and palladium ore in the world, at one stage containing a respective 75% and 50% of the world’s known resources.

South Africa is the only country that challenges Russia in its palladium output, a virtual supply duopoly that sees the countries combined produce around 80% of the world’s mined ounces.

In platinum it is the outright leader, accounting for around 70% of global production.

But low prices for the latter have stalled investments in new production in recent years, something Southern Palladium CEO Johan Odendaal sees reversing in the years to come.

“I think what we are going to see panning out here and if we go back into looking at also the history of PGM prices in particular, we had quite a long period of a very low PGM price environment,” he told Stockhead.

“And what it resulted in is almost a stalling in expansion of existing projects and also a stalling of exploration into new projects.

“So what I believe is certainly going to happen is is certainly a renewed focus in expanding existing operations, and also a new interest in exploration and particularly in South Africa where there are still projects available.

“Definitely we’re going to see a focus back into South Africa and into the other areas as well.”

Previously reported resources for the Bengwenyama project, held by a local South African company called Miracle Upon Miracle Investments, have come in at a little under 19Moz.

Located on the Nooitverwacht and Eerstegeluk farms where local community partner Miracle Upon Miracle Investments won the prospecting rights in 2015, the deposit is nestled among some of the world’s top PGM deposits close to smelters owned by the industry’s two majors Impala Platinum or Implats and Anglo American Platinum.

Common for deposits in its area of the Bushveld complex, where Southern Palladium has both the major UG2 and Merensky Reefs running through its ground, the proportions of palladium and platinum are relatively even at ~44% each.

That gives the company optionality as conditions for palladium and platinum shift.

With palladium prices at all time highs on the back of the Russian invasion of Ukraine, he says it could have longer term implications.

Historically palladium was a lower value metal – when platinum hit all time highs above US$2000/oz in 2008 palladium was fetching less than US$500/oz – but became more economic to mine as emissions standards became stricter and carmakers substituted it for the more expensive platinum in catalytic converters.

That situation has been flipped on its head. But Odendaal is bullish about platinum for the same reason. He thinks the push to diversify away from Russia will draw buyers back to platinum.

“If we look at the current situation, of course, it absolutely favours us with the high palladium and rhodium prices,” he said.

“But of course if we start to see platinum prices increase that will also be very favourable for this project.

“And I think in some cases where you find a high palladium ratio to platinum for instance, when we see palladium prices decline could see it having quite a negative impact on your revenue stream.

“So I believe no matter what happens in Ukraine, and what happens with Russia, I think what we’re going to see in the PGM industry in particular is that consumers are going to focus on new suppliers and also on thrifting.”

Odendaal said substitution is already starting to occur due to super high palladium prices.

“I think we’re going to see certainly the move away from palladium use, (carmakers are) going to try reduce demand for palladium to make themselves less dependent on Russia,” he said.

“And that means that there is certainly going to be increased demand in platinum.

“Because of the palladium price, which is so high, we are starting to see a lot of what we call thrifting. So we see palladium being replaced again by platinum in the internal combustion engine, and particularly petrol engines.

“So, the overall perception is that eventually we will see both platinum and palladium trading on par because both will be applied in the internal combustion engine.”

While palladium prices have touched record highs due to the war in Ukraine, Metals Focus says there is a risk the dispute could impact demand downstream from ICE vehicles.

Previously it had been assumed demand for palladium would rise 700,000oz, and a 12% increase in rhodium, due to a rebound in auto production after semiconductor shortages curbed the industry’s productivity in 2021.

“Compared with pre-pandemic norms, we had expected palladium automotive demand to be just 2% short of the 2019 total and rhodium actually exceeding that year’s demand by 2%, despite a forecast of 8M fewer ICE cars being produced,” Metals Focus said in a note last week.

“Since 24th February, the slump in geopolitical stability and the rise in sanctions have cast mounting uncertainty on the automotive recovery.

“Setting aside the ongoing challenges caused by the pandemic, there

is a perpetuation of existing, as well as new, global supply chain

challenges caused by the invasion that could weigh on demand.”

Metals Focus says even before the Ukraine crisis a slower than expected recovery in chip demand could reduce motor vehicle production by 3.8 million units.

Ukraine was a key supplier of the neon gases used in laser engraving as well, part of the chipmaking process.

“Globally, supply of older technology chips used by the automotive sector could still see intermittent bottlenecks and

disruptions, placing as much as 5M cars and some 550koz palladium

and rhodium demand at risk,” Metals Focus said.

On top of that, vehicle production estimates in Russia, while a small market, have been revised down by 500,000 units, and BMW, Audi and Mercedes Benz have warned of short term production issues. VW expedited a shut down of its factory in Wolfsburg due to its inability to replace wire harnesses imported from Ukraine.

“Finally, even leaving aside these demand-side production issues, a

key ingredient to the recovery in the automotive sector is pent up

consumer demand,” Metals Focus said.

“The consequence of war and sanctions could see consumers rethink large new purchases, adding further uncertainty to what should have been a year when both automotive production and palladium and rhodium demand enjoy strong recoveries.”

Longer term though, Southern Palladium’s Odendaal says despite the momentum behind emissions reductions and the shift to battery electric vehicles by carmakers, ICE vehicles will remain a big part of the new car market for years to come.

That will maintain demand for new sources of platinum, palladium and rhodium as production at older operations winds down.

“There is certainly if you look at from now until 2030, still a very good demand in the application of PGM in autocatalysts, but from 2030 onwards, what we start to see is a stronger demand for electric vehicles in particular, and then, of course, fuel cells will slowly start to to come in as well,” he said.

“But I think the internal combustion engine is still going to be with us for many, many years albeit that you’ll start to see slower demand from 2030 onwards, but some of the analysts look at out up to 2040, that we will still see the internal combustion engine being used in vehicles.”

Tightening emissions standards will also mean increased amounts of the material will be needed for catalytic converters, the main segment of demand for PGMs.

“There’s continuing strengthening of these emission standards. And hence, it will require higher loadings. Despite the fact that we will start to see that decline (of ICE production), there will still be increased loadings of PGMS in the auto catalyst industry,” Odendaal said.

Platinum group elements are also used in fuel cells, where cumulative demand will increase significantly in the coming years.

Just north of Southern Palladium’s Bengwenyama project is Nkwe Platinum, a longtime ASX-listed company whose black empowerment partner Genorah Resources unsuccessfully contested MUM in a dispute over the rights to the Nooitverwacht and Eerstegeluk farms.

They were taken out by major shareholder, Chinese gold giant Zijin, in recent years and removed from the bourse.

The largest PGM producer on the ASX, Implats backed Zimplats (ASX:ZIM) has proven a good investment in recent years, up almost 400% over the last five years.

The company produced around 543,000oz of 6E metals including platinum, palladium, rhodium, gold, ruthenium and iridium in 2020-21 from a network of mines and smelters in Zimbabwe.

Chalice’s aforementioned Julimar discovery, a mix of platinum, gold, palladium, nickel, copper and cobalt containing 17moz of palladium equivalent, has inspired a revival of interest in PGM exploration in Australia over the past couple years, but only a handful of companies have substantial resources.

Trading at 40c and 185% up over the past 12 months, Podium Minerals (ASX:POD) is aiming to become Australia’s first PGM producer from its Parks Reef project in WA.

It this month released a stock exchange compliant exploration target for Parks Reef for between 2.7-3.8Moz of combined platinum, palladium and gold on top of the 2.8Moz inferred mineral resource it announced last month.

Impact Minerals (ASX:IPT) meanwhile is another company with projects on the western margin of the Yilgarn Craton.

On Friday, Impact raised $2m to fund exploration including at its Arkun and Jumbo nickel-copper-PGM projects in WA. It counts Anglo American as one its neighbours after the platinum behemoth followed Impact into tenements near Arkun.

Impact also has mining giant IGO (ASX:IGO) on board, looking to earn a 75% interest over 8 years by spending $18m on exploration at its Platinum Springs nickel-copper-PGE project near Broken Hill in New South Wales.

Located about 20km from the famous Broken Hill silver-lead-zinc mine, IGO has identified a large 420m by 85m EM conductor around 350m below surface around 1000m along trend from a previous hole that struck high grade PGM mineralisation including 0.6 metres at 11.5 g/t platinum, 25.6 g/t palladium, 1.4 g/t gold, 7.6% copper, 7.4% nickel and 44.3 g/t silver from 57.1 metres downhole.

At Stockhead, we tell it like it is. While Impact Minerals and Podium Minerals are Stockhead advertisers, they did not sponsor this article.

Get the latest Stockhead news delivered free to your inbox.