That story, penned in conjunction with Arafura Resources (ASX:ARU), highlighted 30% price growth in NdPr prices between late October 2020 and the price on the date of publication – around $US65.30/kg.

It was impressive growth, but with the benefit of hindsight it really does look as though that was just the beginning. Today, the price of NdPr on the same index makes for some serious reading – crossing the $US100/kg mark in October, it currently sits above $US120/kg.

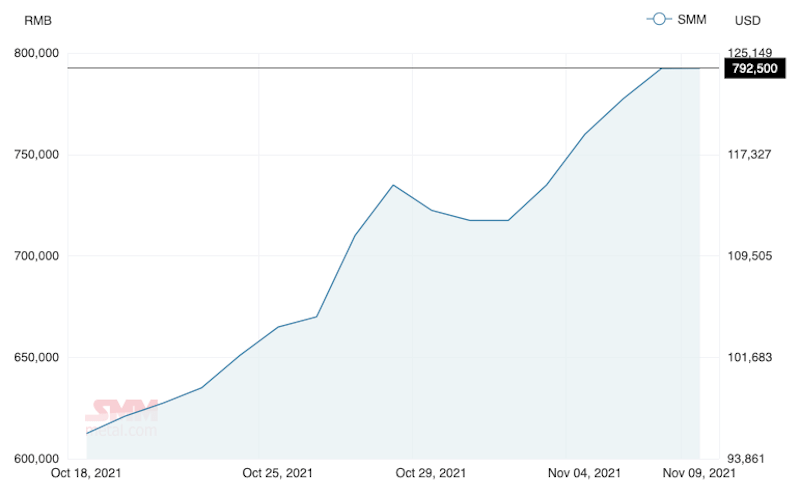

You can keep track of it for yourself on the Shanghai Metals Market website or app, or check the monthly growth chart below.

NdPr price movement over the month to November 9, as measured by Shanghai Metals Market. USD/t listed on the righthand side. Pro tip: there’s 1000kg in a tonne, in case you failed year 10 mathematics like your writer did. Picture: Shanghai Metals Market.

Remarkable.

Rare earths price movement is no secret to those in the know, but mainstream coverage tends to pay more attention to the price movement of certain commodities. We’re all aware of big movements in iron ore and gold. Nickel triggers headlines when highs are hit, so too copper. NdPr and its rare earth relatives generally don’t crack as much of a mention.

High prices are obviously a good thing for project developers like Arafura, which holds the shovel-ready, NdPr-rich Nolans project in the Northern Territory.

That company is progressing discussions with several potential offtake partners with a view to securing 85% of its project output as binding offtake, as it works towards funding and a final investment decision in the second half of next year.

Speaking to Stockhead, Arafura general manager sales & marketing Lloyd Kaiser said it had been more than a decade since a locally listed rare earths project achieved significant funding – one of many reasons the industry was watching NdPr prices increase.

“There hasn’t really been any real investment in plants or projects for such a long time,” he said.

“The last time we saw it really was in 2009, which was Lynas Corporation (ASX:LYC), and that is a long time ago.

“With current high prices and continued price growth, the prospect of good projects getting up into production via funding and offtake is becoming much more real.”

What’s driving prices?

The demand equation is simple. The tech of tomorrow relies on the magnets produced by the rare earths – particularly NdPr – output of today and the years to come.

“Chinese magnet output in 2021 is approximately 228,000 tonnes, and outputs have grown since March 2020. Overall demand has lifted from 160,000t in China,” Kaiser said.

That supply is being soaked up by the world’s growth industries.

“EVs are going really well. You’ve got the electronics market, robotics, e-bikes, wind energy and renewables – over the next five years and beyond we expect to see even more growth in that renewables space,” Kaiser said.

Geopolitical tensions have led the US, Europe, Korea, Japan, India, Australia – the list goes on – to reconsider the global supply chain and prioritise local or allied access to the raw commodities and magnets powering the world of the future.

That’s massive for the demand equation in the future, but it doesn’t really explain the price performance right now.

“Over the last year we’ve seen the Chinese government pushing environmental law within the supply chain, particularly within rare earth processes, and that’s restricted some output,” Kaiser said.

“If there’s any issues with processes or mining operations they have to be rectified, which can take a long time and raise the costs of production. Some of the projects shuttered in the southern rare earths region of China have been closed for years and may never reopen.”

When push comes to shove, the world needs more rare earths for magnets to produce technologies for which appetites are growing. Demand growth, supply constraints. A lack of project investment over the last decade, in an industry where development takes time, with a sprinkling of geopolitics to boot.

Where’s the new supply? It’s a question the whole world should be asking.

At Stockhead, we tell it like it is. While Ionic Rare Earths, PVW Resources, RareX, American Rare Earths and Arafura are Stockhead advertisers, they did not sponsor this article.

Get the latest Stockhead news delivered free to your inbox

For investors, getting access to the right information is critical.

Stockhead’s daily newsletters make things simple: Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.

I want the news:

Hear it first

Get the latest Stockhead news delivered free to your inbox.

Thanks! You’re subscribed, Stockhead news is coming your way soon.