Pic: Bloomberg Creative / Bloomberg Creative Photos via Getty Images

Nickel volatility is still very much a thing, here’s how to make the right pick

Mining

Pic: Bloomberg Creative / Bloomberg Creative Photos via Getty Images

Mining

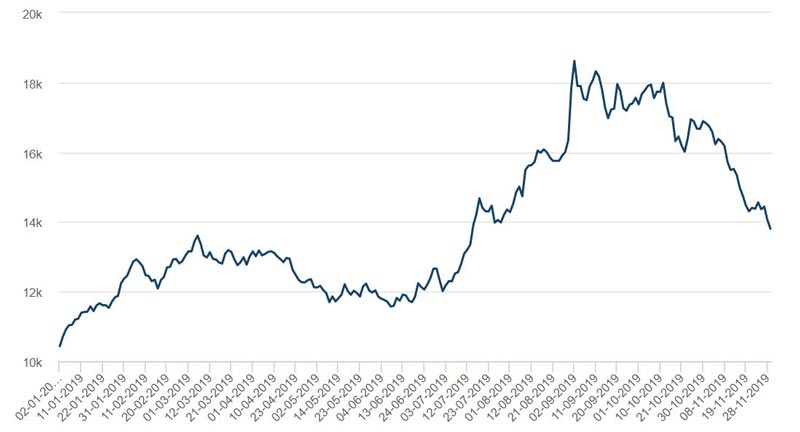

Nickel has the reputation of being one of more volatile commodities to trade in and ample evidence can be seen in how quickly prices fell from the highs of over $US18,000 per tonne in early September to below $US14,000.

The nickel price had initially risen on speculation, which morphed into fact, that Indonesia would ban ore exports in 2020 rather than in 2022.

This changed abruptly on the realisation that the rally lacked support and that there was no shortage of the metal in the market.

Despite this some remain bullish about nickel’s prospects, with S&P Global saying this month that nickel will be one of the best performing commodities going forward.

So is there any further support for this view?

Lion Selection Group fund manager Hedley Widdup told Stockhead that while it was hard to say if the next 12 months would be good for the nickel market, its long-term fundamentals were pretty good.

He added that new demand for nickel from the battery sector was probably a positive thing, but it could be anything from 2020 to 2030 before demand really came through.

“If you’re an investor on a five to 10-year timeframe, you probably have got a little bit more confidence that can play out,” Widdup said.

Concerns have also been raised that while there is sufficient nickel to meet demand from Chinese stainless steel producers, the same may not be true for high-quality nickel for use in batteries.

Market intelligence provider Fastmarkets forecast that while more than 500,000 tonnes of nickel could be used in lithium-ion batteries for electric vehicles by 2025, production of nickel sulphate to meet this demand appeared to have been overlooked.

Widdup also noted that while one of the recent standout plays in mergers and acquisitions (M&A) was Independence Group’s (ASX:IGO) $312m bid for Panoramic Resources (ASX:PAN), it was probably for strategic reasons rather than a trend for nickel players.

Read: Independence makes a move on Panoramic with $312m takeover bid

“I do look at that as an example of merger and acquisition appetite across the mining space, this is a mid-tier company trying to buy a junior,” he said.

“Is it a tick up in nickel M&A? I’m not so sure. Is it a tick-up in M&A by mid-tiers generally? Yes, I think you can probably credit it to that more so than anything else.”

Hedley does have some advice for how to pick the right nickel stocks for our readers.

“I think a good nickel play is something which has reasonable grades because nickel is a very volatile commodity,” he said.

“You want something that is high grade that can carry you through the cycle and there are not many of these around.”

Read: Here’s a plain language guide on how miners ‘grade’ mineral discoveries

The good news for investors interested in Australian nickel players is that the quirks of Australian geology means that our projects tend to have reasonably high grades or reasonably sizeable concentration of nickel along with other base metals

“We are very fortunate to have that. There aren’t too many other continents that have geological endowment as a starter,” Widdup noted.

He said nickel offtakers could drive a hard bargain for nickel concentrate as typically the high-grade deposits were not that large.

“Which means that they are small fish in a reasonably larger ocean of buyers of the concentrate,” Widdup said. “That is something that sort of complicates the picture of what makes a good nickel pick at the end of the day.”

He also took a cautious approach to nickel companies looking at producing higher value products such as nickel that is suitable for use in batteries.

“I suspect that is a slightly new business for miners in comparison to smelting and refining,” Widdup said.

“So while it might be an attractive case, they are probably still coming to terms with actual risks and difficulties of putting that kind of business together.

“And also understanding which concentrates are actually suitable for it. Some concentrates will be more suitable than others based on the percentage of nickel, the percentage of everything else.”

Get the latest Stockhead news delivered free to your inbox.