Mining

Gold Digger: Overvalued or racing towards US$2500/oz? Will the real gold price please stand up?

Mining

Monsters of Rock: Lithium giant Pilbara Minerals says dividend unlikely, but low costs keep Pilgangoora flying high

News

Pic: Bloomberg Creative / Bloomberg Creative Photos via Getty Images

Mining

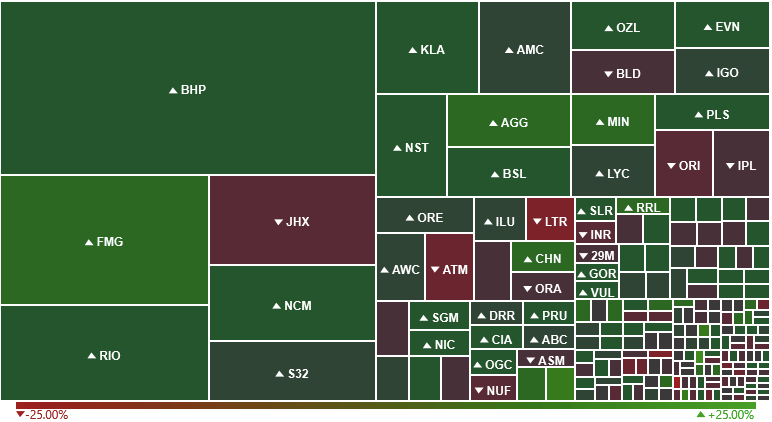

Mining stocks have defied a bearish market, seemingly riding debt-ridden Chinese property giant Evergrande’s near death experience into a sea of bright green.

The company appeared to have entered a default overnight before miraculously finding the cash to stave off collapse at the last minute, in scenes reminiscent of those Premier League transfer deals where the paperwork goes through hours after the deadline.

Dalian futures staged a major rebound after iron ore prices tumbled below US$90/t last night, while Bloomberg reported Chinese property developers posted their best two day gain in 19 months amid optimism government policy that had served to deflate the industry would ease.

In Australia cash flew through the doors of the big iron ore miners, led by Fortescue Metals Group (ASX:FMG), which posted a ~8.2% gain on no news.

BHP (ASX:BHP) and Rio Tinto (ASX:RIO) were also up, while Mineral Resources (ASX:MIN) climbed 5.78%.

Gold miners Northern Star (ASX:NST) (up 4.83%) and Evolution (ASX:EVN) (up 5.06%) were among the top performing large caps.

Among the mid-tiers Sandfire Resources (ASX:SFR), Vulcan Energy (ASX:VUL), Perseus (ASX:PRU), Ramelius Resources (ASX:RMS) and Gold Road (ASX:GOR) were all solid.

Chalice rose more than 9.5%, passing $10 a share to close at an all time high of $10.01, its third straight day of big gains after announcing Australia’s largest PGE discovery on Tuesday.

De Grey Mining (ASX:DEG) (up 7.79%), Regis Resources (ASX:RRL) (up 6.47%) and AVZ Minerals (ASX:AVZ) (up 10.1%) were also sailing high at the close.

There has been no shortage of gold miners and analysts complaining about the whack gold companies have taken in 2021.

Most have enjoyed strong margins and profits this year despite a timid gold price, and potentially a flow of capital into cryptocurrencies, weighing on their share prices.

Gold miners now seem to be hungry for growth, looking to use their growing bank balances to fund capital investments, mergers and acquisitions.

Not all analysts think this is a great thing.

Both Evolution and Newcrest (ASX:NCM) have take a hit from analysts today.

RBC today made Evolution its only “underperform” stock rating among the nine gold stocks it follows, with analyst Alexander Barkley saying downside risk on the gold price and Evolution’s plans to ramp up underperforming assets like Mungari and Red Lake in the coming years bring downside risk.

EVN is already down ~27% YTD to $4.13. Barkley thinks it could drop to $3.50.

“An update to our LOM forecasts lifts our total operating asset NPV by 18%,” he said.

“This includes substantial extensions to mine life based on new Measured and Indicated (M&I) Resource conversion assumptions.

“Further, we forecast Mungari reaching 256kozpa vs guidance of 200kozpa and Red lake at 400kozpa vs guidance 350kozpa. We expect the upper half of group gold production guidance in FY22-24 and AISC to fall over this period.

This, Barkley said, would leave execution risk.

“EVN is guiding to 27% gold growth over FY22-24 with AISC falling 7%. Further, we forecast peak production above some of EVN’s long-term mine production targets,” he said.

“This leaves little room for any ramp-up execution risks; at a time when EVN is constructing and expanding multiple new mines, expanding mill capacities and integrating newly acquired assets. Overall, we find risks to our forecasts are skewed to the downside.

“Despite our healthy LOM forecasts EVN trades at a P/NAV of 1.7x, ~54% above our gold sector average. EVN is also showing limited earnings value; trading on … 7.6x NTM EV/EBITDA. This is 44% higher than close peer NST (outperform) at 5.3x, despite NST’s larger size and greater FY21-24e growth outlook.”

Newcrest is also raising eyebrows for its growth ambitions.

It will pay US$2.8 billion (~$4 billion) in cash and shares to acquire Pretium Resources and its 345,000ozpa Brucejack mine in British Columbia, Canada.

The deal will immediately boost Newcrest’s production profile beyond 2Moz, extending its gap on Australia’s second biggest gold miner Northern Star.

But with M&A prices getting frothy there are simmering feelings that Newcrest may have overpaid.

“We lower our fair value estimate for no-moat-rated Newcrest Mining to AUD $28.50 from AUD $29.50,” Morningstar equity analyst Matthew Hodge said.

“We think the proposed acquisition of Pretium Resources brings a high-quality, relatively low-cost mine in Brucejack in British Columbia, Canada.

“However, we think Newcrest is likely overpaying, hence the slight reduction in our valuation.

“Newcrest is looking to expand production from the current base, and if cash costs can be brought down with increasing volumes and exploration proves successful, there may be upside to our estimate.

“Also, if the gold price exceeds our long-term assumption of US$1450/oz in 2025, this would be upside too. Based on our assumptions we expect the acquisition would be valuation neutral at a gold price of about US$1800/oz, close to spot.”

Mining

Mining

News

Get the latest Stockhead news delivered free to your inbox.