Price to Earnings Ratio (P/E) is a handy way for analysts and investors to understand whether markets are overvaluing or undervaluing a stock by comparing the price of a company’s stock to the earnings it generates.

2008 – the last time mining companies were this cheap — was an exceptionally volatile time for the metals and mining industry.

Aluminium and copper prices hit record levels during 2008 but by the end of the year aluminium, copper, nickel and zinc had declined 55.5%, 67.8%, 67.5% and 60.3%, respectively, from their 2008 highs. Manic.

This was driven by slowing growth in China, the collapse in liquidity and downgrades to the global economic outlook.

Sound familiar? In 2022 thus far we have seen declines of 15% for aluminium, 22% for copper, 37% for tin and 12% iron ore for many of the same reasons.

The Aussie version of same P/E chart above is a bit healthier but following a similar trend to the S&P500.

It indicates that investors are predicting greater commodity price weakness ahead, which is going to impact company earnings.

Is that too bearish an outlook, or just about right?

MineLife analyst Gavin Wendt says the downturn is understandable, but at the same time indicates that there is medium to long-term value in the sector given the commodity rush is ongoing.

“Perhaps markets are looking at the commodity cycle and saying, ‘we are selling down resources stocks because we anticipate that the existing downturn is going to be more prolonged’,” he told Stockhead.

“It could also mean investors are just taking their money out of the resources sector; in fact, many are probably taking their money out of everything right now and putting it into cash,” he says.

It could also just be a short-lived dip, Wendt says.

“Investors tend to get a little bit nervous about the resource sector when you talk about recessions, issues with China, and stagflation,” he says.

“It could turn around quite quickly over the coming months if we start to see China implement some really meaningful stimulus in order to get their construction sector, and the broader economy, going again.”

Gavin’s favourite commodities right now are …

The resources sector is a broad church; demand drivers can differ dramatically between commodities.

As such, some metals will always perform better than others. Which sectors does Wendt like best for the remainder of 2022 and beyond?

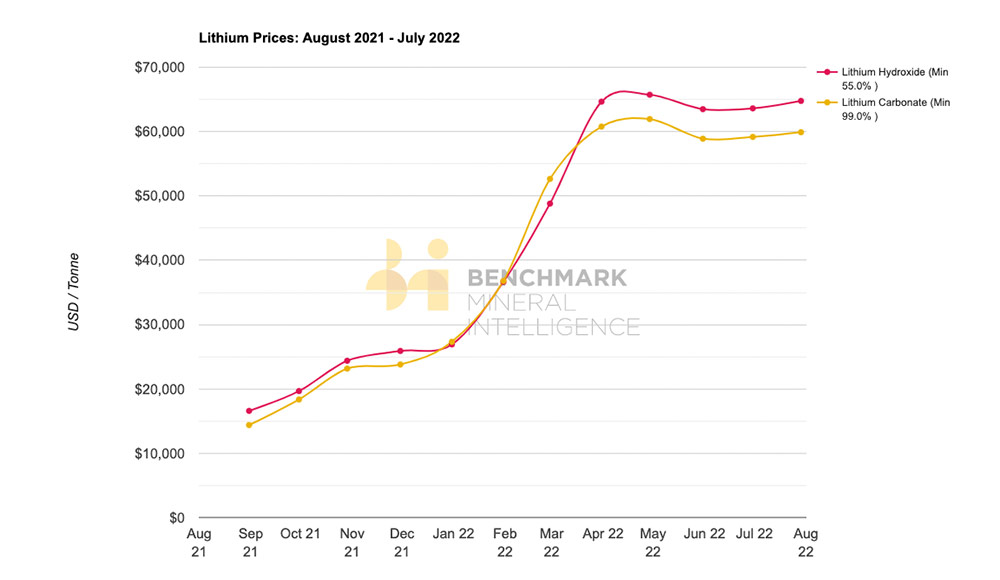

LITHIUM

Average lithium prices over the past year. Pic: Benchmark Mineral Intelligence.

“I think the lithium sector is still the standout,” he says.

“It’s been a cocktail of negative factors since the start of 2022 — with the Ukraine war, inflation, rising interest rates, question marks over China. Meanwhile, the lithium price has just held up outstandingly well.

“We also had lockdowns in China which means consumers have not been out there consuming – that would be having a big impact on EV purchasing in China.

If lithium and lithium companies can perform that solidly during a significant period of market uncertainty then there is still a lot of upside there, Wendt says.

Meanwhile, EU coal prices are more expensive than at any time in recorded history too (25y) as Europe scrambles to replace 58 million tonnes pa of thermal coal it mustn’t source from Russia while coal production came rather unfashionable for the past decade (green shift).

The other standout sector — probably just as much as lithium, Wendt says.

“You would have to think this energy shortage is not going to go away anytime soon which means thermal coal prices will stay elevated for at least the next 12 months,” he says.

“I think the coal sector should continue to do really well.

“You even have coking coal producers selling into the thermal market, because they are getting a better price for it.

“I think iron ore will depend a lot on China,” Wendt says.

“I think it’s fair to say that iron ore’s best days are behind it in terms of pricing – we probably won’t see $US250/t again — but then that doesn’t mean we are going to see prices back at $US40/t.”

The iron ore price continues to surprise, he says. There is still very strong demand out of China, and every time the price threatens to dip below $US100/t it has rallied.

“So, I am not writing off the iron ore sector and I think the forward price for iron ore will be comfortably above $US100/t,” Wendt says.

“That means your iron ore focused companies will continue to generate really strong profits.”

Get the latest Stockhead news delivered free to your inbox

For investors, getting access to the right information is critical.

Stockhead’s daily newsletters make things simple: Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.

I want the news:

Hear it first

Get the latest Stockhead news delivered free to your inbox.

Thanks! You’re subscribed, Stockhead news is coming your way soon.