Mining

Reporting Rodeo: Here's how analysts think the ASX's big miners will shape up in March quarter reporting season

Mining

Resources Top 4: Gold stocks gain again, while Piedmont's US lithium ops get a boost

Mining

Pic: Schroptschop / E+ via Getty Images

Mining

Demand for battery metals to power the green transition is on the up, with Wood Mackenzie projecting global demand for energy storage will rise to 1TWh by 2030.

Energy storage deployments around the world are going to triple in 2021 alone, analysts from the consultancy said in their Global Energy Storage Outlook report this week, to 12GW/28GWh.

Global lithium-ion battery capacity is also forecast to double over the next two years with storage and EV application to drive demand for the dominant nickel-cobalt-manganese and lithium-ion-phosphate chemistries – 89% of the LiB market – to 2.3TWh by the end of the decade.

In the energy storage sphere the Asia-Pacific market, dominated by China, will total 400GWh by 2030, while tax credits will drive US demand up 4.5x this year, with the US and China expected to account for 70% of demand in 2030.

Europe will also see unprecedented demand growth for energy storage over the next nine years, with the world’s leading EV market accounting for 100GWh of demand.

Lithium prices have already hit record levels on the back of supply shortages, with battery makers struggling to get their hands on enough raw materials to fill their production lines.

The dramatic uptick in energy storage application begs a bigger question – just how will we mine and produce the commodities essential to fulfilling this demand?

It is projected demand for metals from the energy transition is going to spike significantly. WoodMac sees the market for nickel, for instance, doubling from 2.4Mt today to 4.9Mt in 2040.

Only 800,000t of that demand will come from nickel’s traditional stainless steel demand sector, with as much as 30% of that demand coming from battery precursor producers, up from 7% in 2020.

That is all before COP26, the highly anticipated global climate dialogue taking place in Glasgow next month.

That event is all but certain to result in countries and the conglomerates that operate in them adopting more ambitious targets to decarbonise energy and electrify power.

WoodMac metals and mining vice chair Julian Kettle says demand is not the question, it’s about supply, a point echoed by nickel, copper and lithium miner IGO’s boss Peter Bradford, who told the Australian Nickel Conference in Perth last week the minerals sector risks slowing the pace of change if it does not build new mines fast enough.

Kettle says the industry is way behind on the capital spend needed to meet the ambitions of world leaders.

“Politicians, NGOs and consumers are set on stimulating demand for energy transition commodities through ambitious target setting,” he said.

“That we are way behind on the necessary capex spend is unquestionable; yet it seems investors and policy makers are either not listening or are unwilling to play their part in ensuring the significant increase in supply which is so desperately needed.”

Aided by supply chain issues wrought by Covid-19, supply crunches are already being felt in some metals essential to the energy transition.

Tin, a material used as solder in electronic circuit boards, is a case in point, with the world’s major commodity exchanges seeing their stocks reduced to 2.5 days of global consumption earlier this year as prices spiked towards record levels.

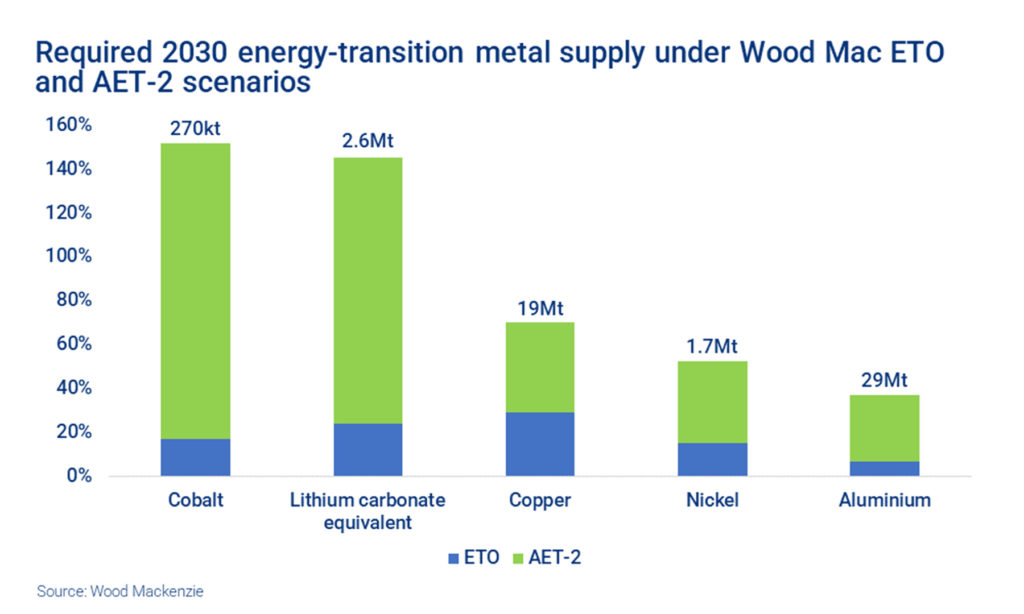

Research from WoodMac shows the gulf between a base case energy transition, limiting global warming to 2.5C on pre-industrial levels, and a 2C scenario aligned to Paris targets is staggering.

“The supply gap represented by the uncommitted proportion of the potential 2030 market represents a major opportunity for investment, with the associated tonnages being truly transformational when set in the context of current market size,” Kettle said.

Kettle says without a “sea change in policy” delivering the metal by just 2030 required to meet net zero by 2050 targets would be “truly incredible”.

“As demand continues to grow, we believe the attention of the analyst community will start to focus on miners tilting the dividend distribution vs capex balance more towards growth,” he said.

“The precursor to this is a debate on whether the mining industry (or rather its investors) has the appetite to fund the significant investment necessary to achieve an AET-2 pathway.

“Of course, this debate presupposes that it remains possible to physically develop the required mining and processing capacity in time, which is by no means a given.”

The other factor impacting investment for critical metals is not just global demand as a whole, but the desire to diversify supply chains away from China.

According to BloombergNEF in a report released last week, China will remain the dominant player in the lithium ion battery market over the next five years.

It presently hosts 80% of the production capacity for LiBs, and is expected to lift output by 100% by 2026 to two TWh, equivalent to 20 million EVs.

But the USA has moved up its rankings to second in both the 2021 and 2026 projections, based on battery demand, improved manufacturing and broader regulatory support in the early days of the Biden Administration.

“The US has many of the ingredients needed to foster a domestic lithium-ion battery value chain, but in the past, individual companies like Tesla have had to forge a path by themselves. Now that there is policy support in place, we are seeing a coordinated effort from companies across the supply chain to anchor more value within the country,” BNEF head of energy storage James Frith said.

Europe has also shown its determination to invest in a domestic battery supply chain, with the first locally-owned GW scale factory to be opened by Northvolt in Sweden in late 2021.

If Europe were ranked as a whole, the volume of demand for batteries across the EU would make it a bigger market than China, BNEF said.

“Europe has set the ambitious goal of supplying all of its own battery demand for the region by 2025, and has committed billions of euros in state aid to attract investments in the battery supply chain. We are now starting to see the results of this effort,” BNEF energy storage analyst Cecilia l’Ecluse said.

Lithium and other battery metal miners who are able to operate in and sell to these jurisdictions are set to benefit not just from what could be a major shortage of supply for their product in general, but also the desire of European and American customers to exit the Chinese supply chain.

In Europe, Rio Tinto (ASX:RIO) is leading the charge at the top end of town with its US$2.3 billion Jadar lithium-boron mine, which from 2026 promises to be Europe’s largest lithium producer.

However, it is facing opposition however from local communities in and around the giant Serbian lithium deposit, where it plans to mine a rock called jadarite famous for having a similar chemical composition to the fictional kryptonite from Superman.

European Lithium (ASX:EUR) is advanced with its smaller scale Wolfsberg lithium project in Austria, where a definitive feasibility study is due in the first quarter of next year following a major drilling program.

A PFS in 2018 showed the mine would produce 10.129tpa of lithium hydroxide over a 10-year-plus mine life, generating an NPV at the time of US$339.4m.

Lithium markets are arguably better placed than they were when European Lithium released that study, which came shortly before a crash in lithium prices, which are now well and truly back on the up.

Vulcan Energy (ASX:VUL), has excited the market with its novel geothermal Zero Carbon lithium project in Germany, raising upwards of $300 million from investors this year alone.

It recently produced its first battery quality lithium hydroxide from a pilot operation, and signed its first offtake deal with LG in July.

In the non-lithium space local copper miner Sandfire Resources (ASX:SFR) recently announced a US$1.865 billion deal to purchase the 100,000tpa MATSA copper complex in Spain from Trafigura and Abu Dhabi’s Mubadala Investment Company.

Over in the States there are a host of ASX-listed companies trying to open that country’s vast stores of lithium resources.

Ioneer (ASX:INR) is the most advanced, securing a US$490m investment from global major Sibanye-Stillwater to help develop its Rhyolite Ridge project in Nevada. A key risk there could be the proposed listing of the native plant the Tiehm’s buckwheat as an endangered species, which Ioneer says it supports and will work to coexist with at Rhyolite Ridge.

Other North American focused lithium miners include Piedmont Lithium (ASX:PLL) and Sayona Mining (ASX:SYA).

At Stockhead, we tell it like it is. While European Lithium is a Stockhead advertiser, it did not sponsor this article.

Mining

Mining

Mining

Get the latest Stockhead news delivered free to your inbox.