Pic: Bloomberg Creative / Bloomberg Creative Photos via Getty Images

Battery demand projections for 2030 are getting bolder, but what will it do for your favourite battery metals?

Mining

Pic: Bloomberg Creative / Bloomberg Creative Photos via Getty Images

Mining

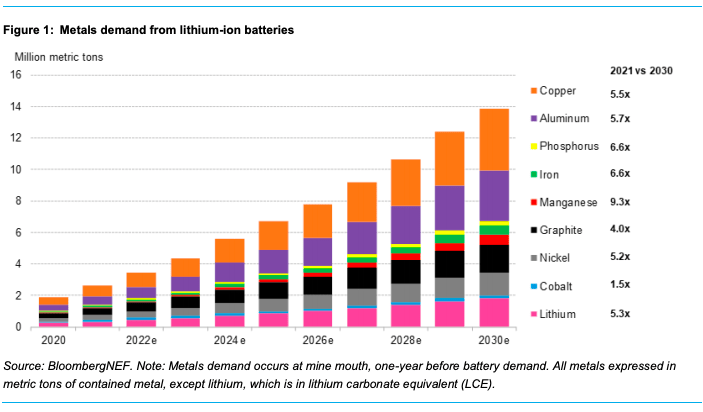

Another day, another bold prediction about the future for lithium ion batteries, this time from BloombergNEF, who say their 2030 projections have been bumped up 35% in a year.

Driven by a growing appetite for passenger electric vehicles, BloombergNEF predicts by the end of the decade demand will hit an annual level of 2.7 terrawatt hours.

Of course, these predictions are just that and have been known to morph over time, but they do give an indication that the pace of change, in particular when it comes to EVs, is expected to continue to rise.

As battery demand goes up, so does demand for the commodities needed to supply the market. Here’s where BloombergNEF’s analysts believe key battery metals are headed.

Lithium prices have stormed upwards this year, with Chinese market giant Ganfeng recently suggesting they could climb back towards record levels seen in late 2017 and early 2018.

According to BNEF carbonate prices are up around 71% this year, with hydroxide up 91% and spodumene concentrate 58% better off.

They believe lithium prices will plateau in 2022, with the hydroxide market facing a shortage sometime between 2025 and 2027 depending on how quick Australia’s conversion plants are to ramp up.

“One key risk is that some 35% of the projected supply growth from now until 2025, will come from integrated spodumene-to-hydroxide converters in Australia,” they wrote.

“These projects are expensive and have a history of delays. Should the commissioning of these Australian converters be delayed there may be a shortage of hydroxide by 2025.”

Will we see the market split in price between class I nickel for batteries and lower quality options reserved for steel refining?

BNEF thinks so, but we haven’t seen it yet. They think prices will continue to hover around US18,000/t this year.

Going forward the nickel sulphate market – that is the kind of nickel chemical prepared for lithium ion batteries – has had its shift into deficit delayed by the Chinese auto markets pivot to cheaper but less efficient lithium-iron-phosphate (LFP) battery chemistries.

In BNEF’s high LFP replacement scenario the cheaper chemistry’s share of the stationary storage market would climb from 23% to 53% by 2030.

Nickel rich battery cathodes will still be adopted at pace though, with BNEF predicting the market may slip to a 128,000t deficit around 2024.

Cobalt is going to head into a slight surplus this year if small-scale artisanal miners are able to ramp up production.

Since prices spiralled out of control in 2017, cobalt has faced the biggest challenges in terms of its long term future as a battery metal, mainly because of geopolitical concerns about its supply, which largely comes out of Africa and specifically the DRC.

Prices are up 42% since the start of the year, hitting US53,000/t in March, its strongest level in three years. BNEF expects prices to average US$45,000/t this year and hold around US$44,000/t out to 2025.

Manganese is the M in N-C-M battery chemistries. It is forecast to have the highest proportional growth in demand from the battery market of any metal, with the market in 2030 projected to be 9.3 times greater than in 2021. Sulphate prices are up 30% this year.

Demand for graphite meanwhile is projected to rise 37% in 2021 to 446,914, BNEF estimate, and 297% by the end of the decade.

Get the latest Stockhead news delivered free to your inbox.