Markets across the region and in New York are prepping for the likely conclusion to the awful public spectacle of a once incredible tech-giant’s two-year orchiectomy, as Alibaba reports its Q2 earnings Thursday night Sydney time, ahead of the opening bell on Wall Street.

Wall Street analysts are saying that after a decade of effortless fiscal rigidity, Jack Ma’s Alibaba (NYSE: BABA) is about to report its first ever slump in quarterly revenue.

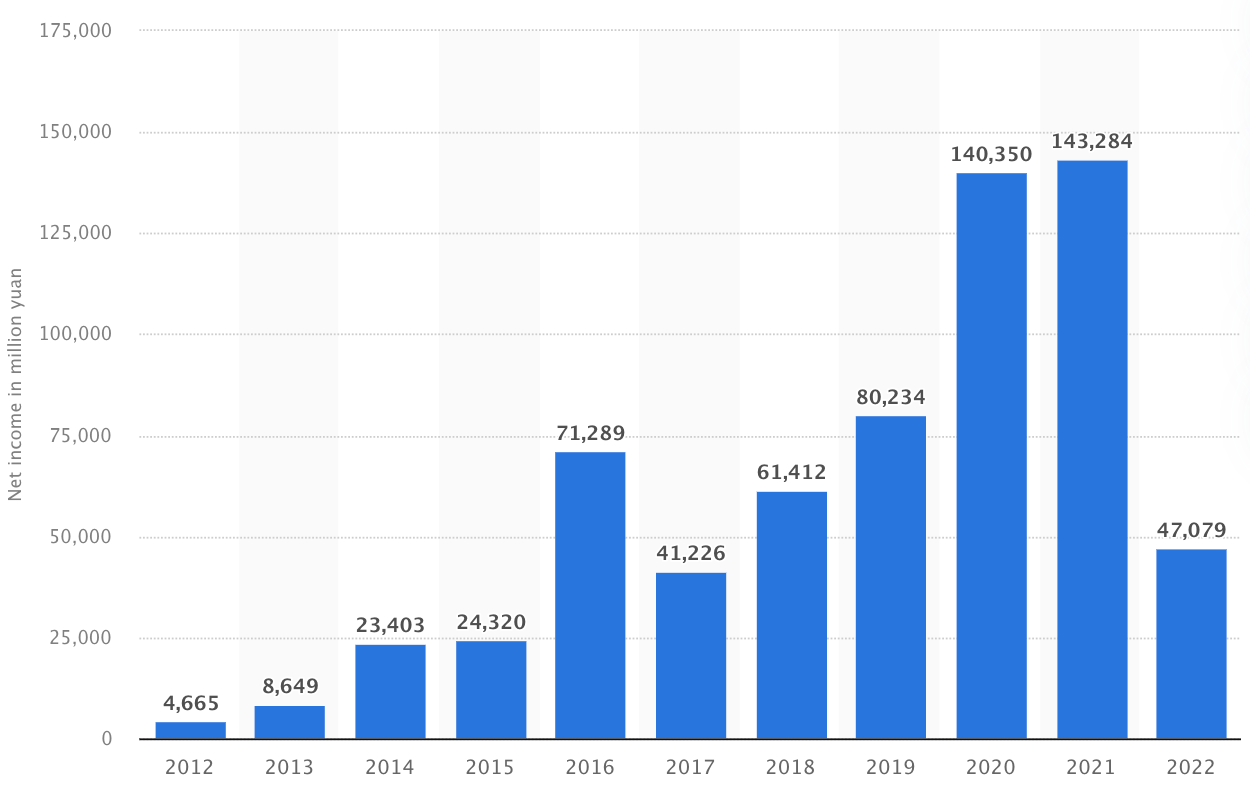

Alibaba: annual net income FY12 – FY22 (in million yuan)

Via Alibaba

The other Chinese tech and business magnate, investor and philanthropist-billionaire who comes to mind is Jack Ma’s bestest frenemy, Pony Ma. His social media mega-company Tencent will report Friday night. It’ll be touch and go for an equally gelded Pony as well.

It’s almost hard to remember now that before the invisible hand of the Chinese Communist Party wiped away some US$1 trillion off the Tencent and Alibaba market caps, these were the internet-tech plays with the most potential, the broadest growth and the most blue sky prospects that the world had seen since the rise of Apple and Microsoft during the initial internet boom.

Alibaba HQ, Hangzhou China. Via Alibaba

Analysts point to China’s zero-COVID policy, global economic uncertainty and a domestic consumption slump as a few of the headwinds behind BABA’s flaccid results.

But the problem is much simpler and lots more violent.

Jack Ma’s Alibaba Group was already a household name and an integral part of the nascent Chinese e-commerce netscape when the ambitious Hangzhou Teachers School dropout began to expand Alibaba from an e-commerce facilitator into a multinational technology conglomerate.

Ma and Alibaba became the stuff of instant legend. The epitome of the Chinese Dream, writ large.

Pic: Jack Ma, via Alibaba

Unassuming and incredible, Ma and his plaything (now the plaything of everyone in China) became the name and address of the Chinese economic miracle.

I was in Beijing during the years of almost instantaneous user take-up. Amid China’s madhouse sprint to modernisation, the takeovers, the monetisations, the public offers and the multi-trillion Yuan valuations.

Then on November 1st, 2020 Chinese President Xi Jinping via China’s Financial Stability and development Committee headed by his right-hand boy and economic tsar, Liu He, scrapped the looming public listing of Alibaba’s affiliate Ant Financial.

Investors had pre-ordered – check it out – $3 trillion of stock. The IPO put Ant around $315 billion – four times the value of Goldman Sachs.

Alas, a week earlier Ma had indirectly criticised the Chinese government for “stifling innovation”.

The IPO was on pace to shatter records. The excitement was palpable and investors lined up for Ant’s dual listing in Hong Kong and Shanghai, where in Shangers alone institutional investors subscribed for over 76 billion shares, more than 280 times the initial offering tranche.

Pulling the ANT IPO was the first cut in Xi and He’s root-and-stem neutering of Chinese tech. This was, at the time, easily the world’s largest fintech. Its audacious integration into the everyday lives of Chinese everywhere was – and still is – hard to wrap your head around.

Which is why Ma, Ant and Alibaba et al so clearly came to be viewed as an existential threat to the upper echelon of the Communist Party.

Since then Ma’s business and the man’s own vitality has been ripped to absolute shreds.

Happier times – ASEAN Leaders gathering BALI – Oct 12, 2018: International Monetary Fund MD Christine Lagarde (L) meets with Jack Ma during the IMF/World Bank Annual Meetings, 2018 in Bali, Indonesia. (Stephen Jaffe Getty Images)

Alibaba and its various affiliates – most particularly Ant Group – are at their core so startlingly good, that it’s taken this long for the bleeding to show.

And forget the wider geopolitical tension, the economic uncertainty, the regulatory confusion, the State-sponsored bullying or just the absurdly unpredictable deformities these are producing across the Chinese Internet and the formerly dominant e-commerce giant. Because in just the last fortnight BABA has been slapped onto the US Securities and Exchange Commission’s (largely Chinese tech-companies) blacklist which now face a delisting of their shares from Wall Street indices unless they allow American regulators to audit company records.

Since then Ma has popped up saying he’s divesting all his holdings in, and control of Alibaba, Ant Group and all the many many bits and pieces they picked up along the way.

For now, Wall Street’s put its clammy grip around an Alibaba second-quarter profit estimate of US$1.56 a share, on US$30.17B in revenue, possibly tip-toeing into a historic maiden year-on-year revenue slip since it went public.

Even despite this, highly-paid Wall Street analysts suggest there are signs that the Chinese Internet market is stabilising, and that BABA is in a position to lift growth during the rest of this year.

This is both true and messed up.

Following the US$1.15 trillion blood loss across Chinese tech after Xi and He whipped out the knives in late 2020, early 2021, it’s true, there is definitely money to make in Chinese tech.

But no matter what Alibaba’s next move is, the grim medical truth for the once trailblazing giant is clear: Castration is most definitely permanent.

Get the latest Stockhead news delivered free to your inbox

For investors, getting access to the right information is critical.

Stockhead’s daily newsletters make things simple: Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.

I want the news:

Hear it first

Get the latest Stockhead news delivered free to your inbox.

Thanks! You’re subscribed, Stockhead news is coming your way soon.