Guy on Rocks’ is a Stockhead series looking at the significant happenings of the resources market each week. Former geologist and experienced stockbroker Guy Le Page, director, and responsible executive at Perth-based financial services provider RM Corporate Finance, shares his high conviction views on the market and his “hot stocks to watch”.

Market Ructions: Dark Clouds

As the Ukraine invasion rolls on, it is timely to look at potential disruptions to commodity markets with table 1 setting out Russia’s share of global supply.

Table 1: Russian production and exports of industrial commodities (Source: Macquarie, Sales Desk Strategy, 24 February 2022).

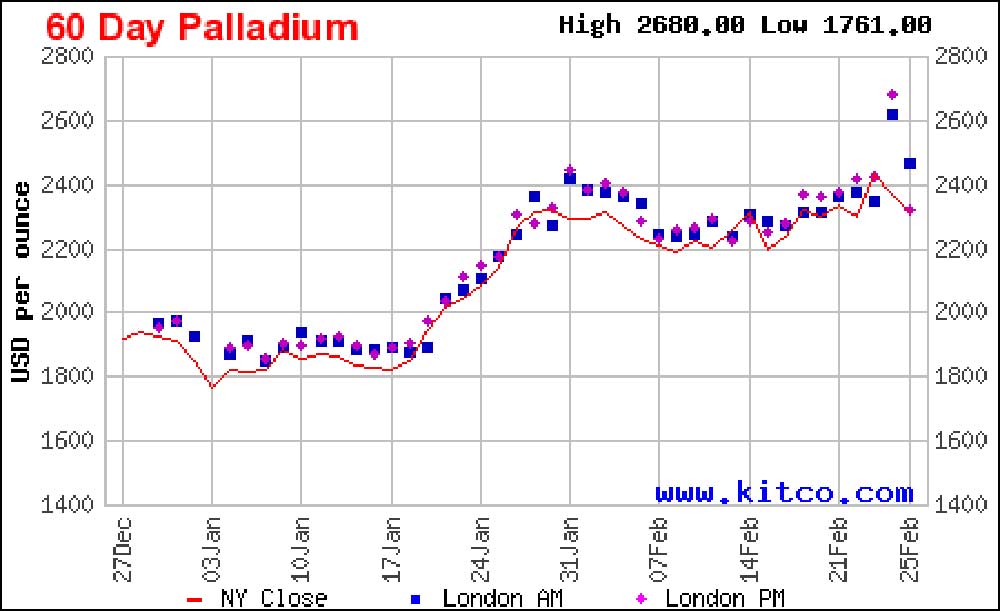

Of the precious metals, palladium looks the most exposed however it has barely responded, trading at around US$2,300/ounce (figure 1).

As we know however, metal demand/supply metrics and price volatility are not a linear equation and the Ukraine invasion has some way to go. We will see.

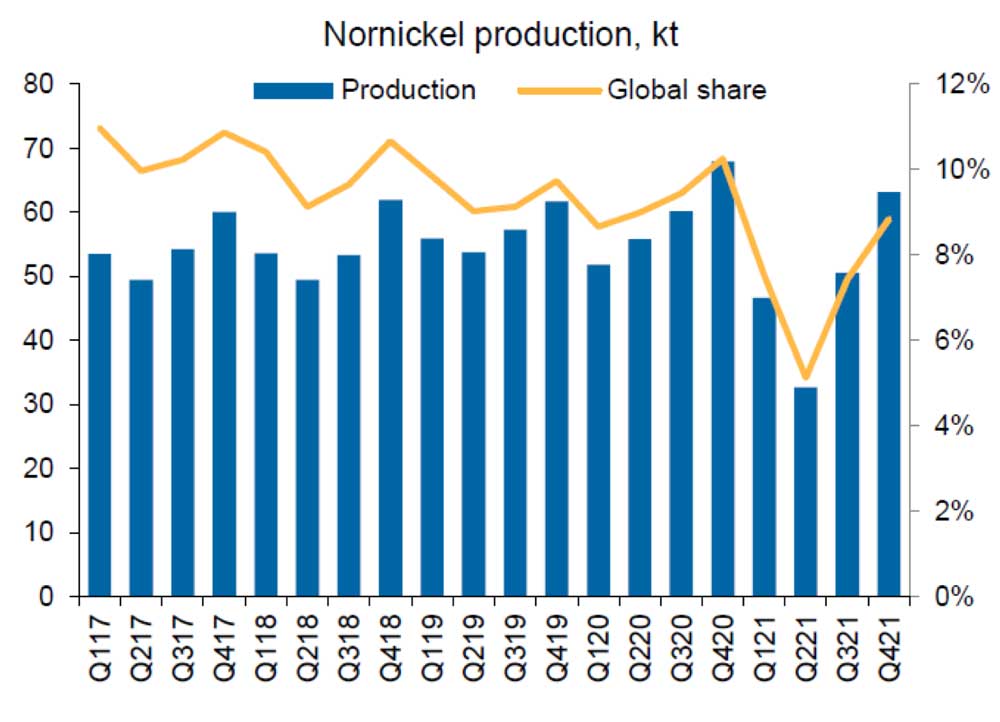

Notably copper, nickel and thermal coal represent 4%, 8% and 17% of Russian share of global supply respectively.

The copper and nickel markets as the Stockhead faithful know are “tight” and while these percentages seem low, their impact could be very significant in the near term.

Figure 1: 60-day Palladium spot price (Source: www.kitcometals.com).Figure 2: Nornickel production (Source: Macquarie, Sales Desk Strategy, 24 February 2022).

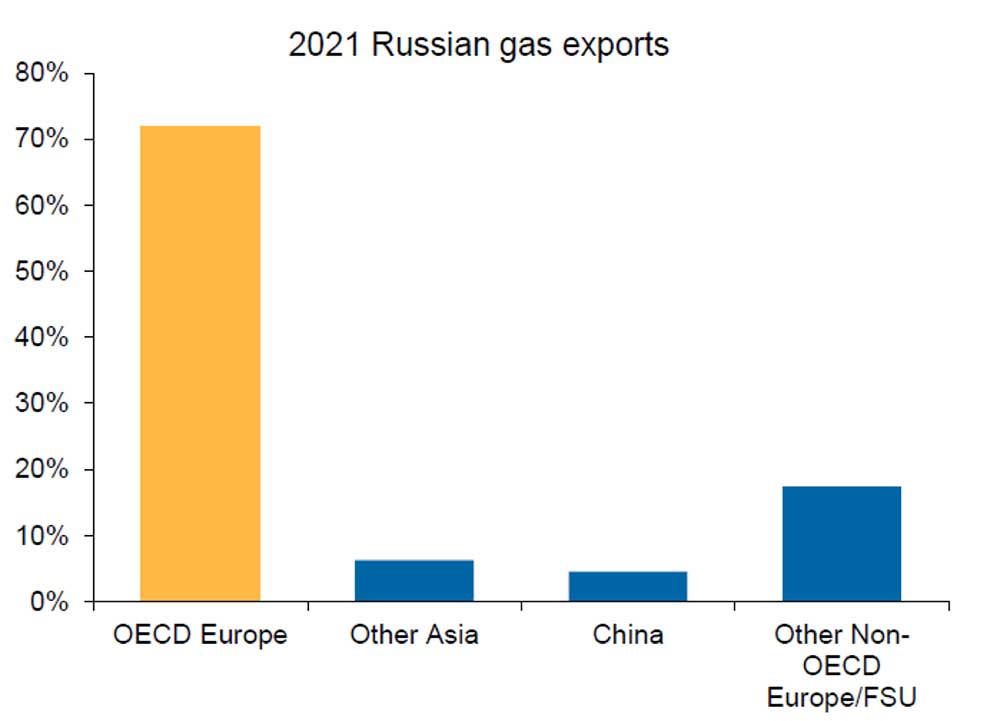

The elephant in the room is of course natural gas (figure 3) which supplies around 30% of Europe’s, and around 32% of Germany’s requirements.

In total, over 70% of domestic Russian gas production is exported to Europe; hence the initial reluctance by the West to do away with the SWIFT payments system as part of the proposed sanctions against Russia.

Ironically if Germany had not decided to move away from nuclear power the conversations regarding sanctions the West is having with Russia at the moment could be very different.

Figure 3: Russian gas exports (Source: Macquarie, Sales Desk Strategy, 24 February 2022).

Nuclear power accounted for approximately 13.3% of Germany’s electricity supply in 2021 (6 power plants) of which three were decommissioned late last year. The balance are due to close at the end of CY 2022 in accordance with the 2011 phase out plan.

A disastrous poorly thought-out plan for which the Germany economy will suffer as a result.

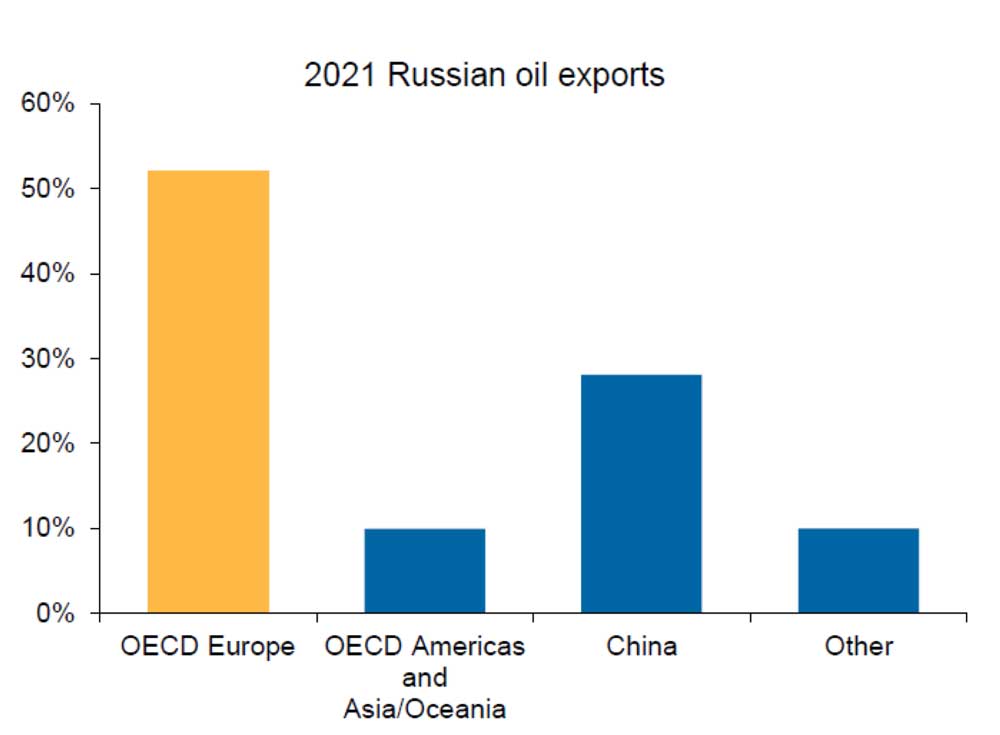

Russia also produces (figure 4) approximately 10 million barrels of oil (10% of world supply) of which 50% is exported to Europe of crude oil, accounting for 10% of global supply. The USA buys just under 18 million barrels from Russia, or 7% of its annual requirements.

Countries have permanent interests not permanent allies so keeping the lights on in Europe is always going to take precedence over military intervention on the fringes of Russia.

It appears that Putin so far has played all the right cards; accumulate a US$600 billion war chest, hold the gas switch in one hand and a big stick in the other and see who blinks first.

The SWIFT exclusion on selective banks (probably those not involved in trading fossil fuels?) will certainly make life very difficult for many Russian businesspeople.

Wars don’t always go according to Hoyle however and the prospect of a protracted guerrilla war in a vast country with a large number of weapons in the community will prove to be a difficult beast to tame and an even more dangerous place for any remaining Russian soldiers.

The pursuit of disastrous energy policies founded on flawed climate change debates and delusional renewable energy targets could plunge many parts of the West into an energy crisis (particularly in Europe) of its own making.

Germany’s disastrous move to phase out nuclear power (now purchasing nuclear power from France) means Russia remains an important business partner.

In the short-term Russia has neutralised any possibility of military intervention by the West in the process weakening the bargaining position of both the USA and Europe.

So where to from here?

Continued tightness in supply, upward pressure on base and precious metals and rising energy prices fuelling runaway inflation which is already off the leash.

While not a military strategist, the prospect of a large heavily armed Ukrainian population (including soldiers who will likely melt back into civilian life) taking on a protracted military insurgency could prove a longer-term challenge for Russia.

The second Chechen war is still fresh in the mind of many Russians and saw a brief 9-month war (August 1999-May 2000) followed by an insurgency phase from 2000 to 2009.

“Chechen Syndrome” was the name given to traumatised returning soldiers from Russia. “Ukrainian Syndrome” could well follow.

You have to like Volodymyr Zelensky showing himself on a video message near the centre of Kiev. Not dissimilar to William the Conqueror who quashed rumours of his death at the battle of Hastings in 1066 by lifting the visor of his helmet while galloping along the Norman lines.

As is often the case, the real danger for Putin may come from his inner circle or even the Russian people if he can’t deliver on his promises and it turns into another Afghanistan.

The recent press conference demonstrated there are also a few cracks appearing at the Kremlin with the head spook appearing to forget his lines.

Russia’s economy is projected to be around US$1,700B this year (Australia is just under US$1,500B) and with a population of almost 6 times that of Australia and with no middle class, who knows what could happen if the economy takes a nosedive and the Russian people become unhinged.

I mentionedPeel Mining (ASX:PEX) last year and while the share price performance has been a little disappointing, investor interest has certainly returned with the company raising $21 million at 18 cents.

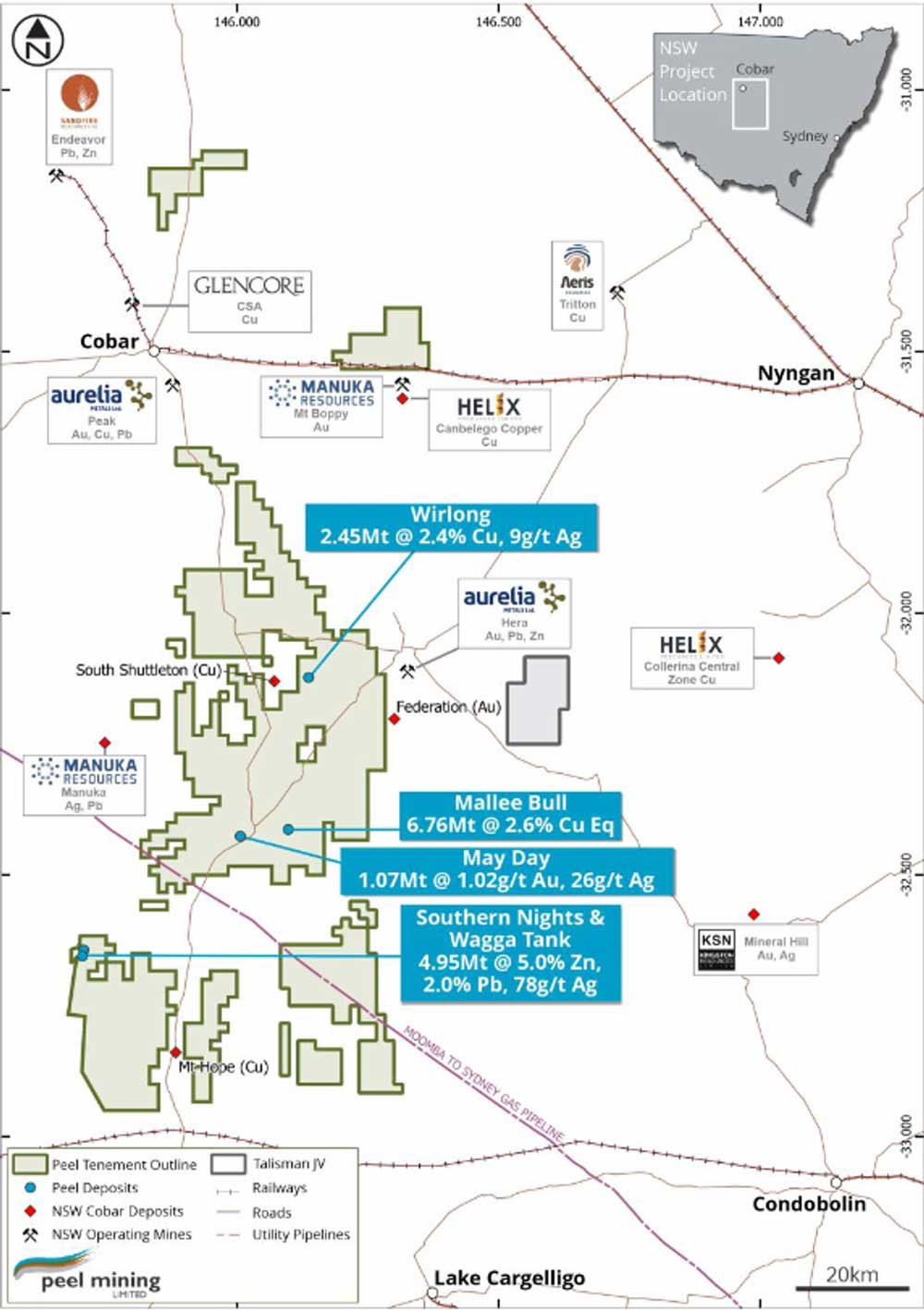

This will be applied to their South Cobar Copper project (figure 6), namely Mallee Bull (JORC Resource of 6.8Mt @ 1.8% Cu, 31 g/t Ag) and Wirlong (JORC Resources 2.45Mt @ 2.4% Cu, 9 g/t Ag) ~100km south of Cobar (NSW).

So far mineralisation has been outlined from around 60 metres vertical depth and is open along strike and at depth.

The company is targeting a 10 year, 20Ktpa operation and metallurgical testwork has been promising with Wirlong returning 95% Cu recoveries reporting to a 32% concentrate and Mallee bull 90% and 30% respectively.

Figure 6: PEX south Cobar Copper project (Source: PEX RIU Presentation, 15 February 2022).

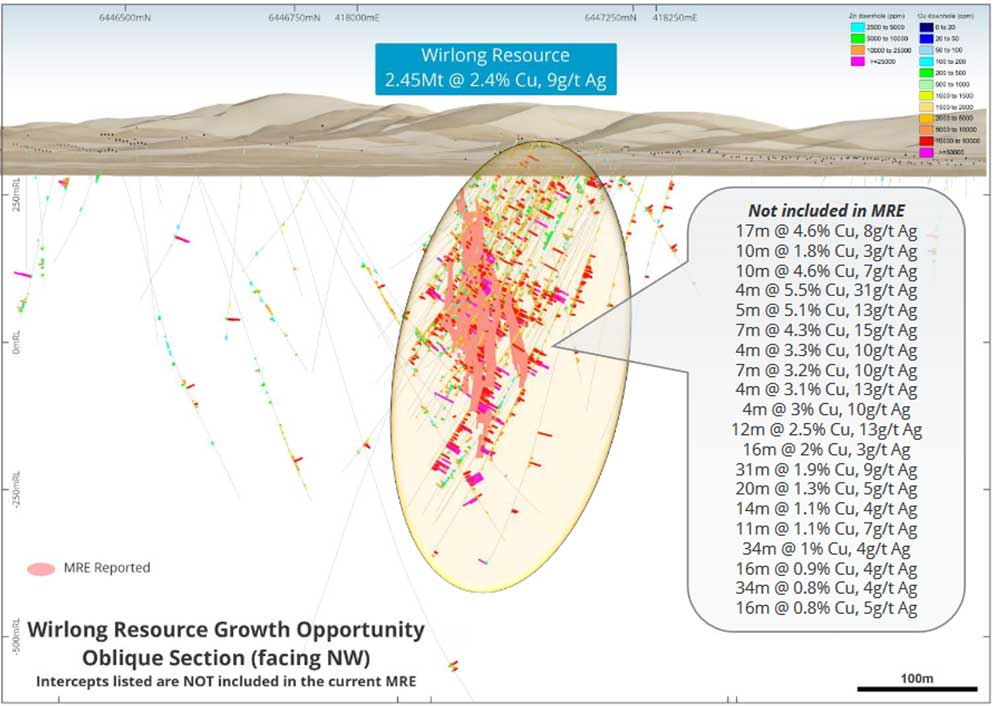

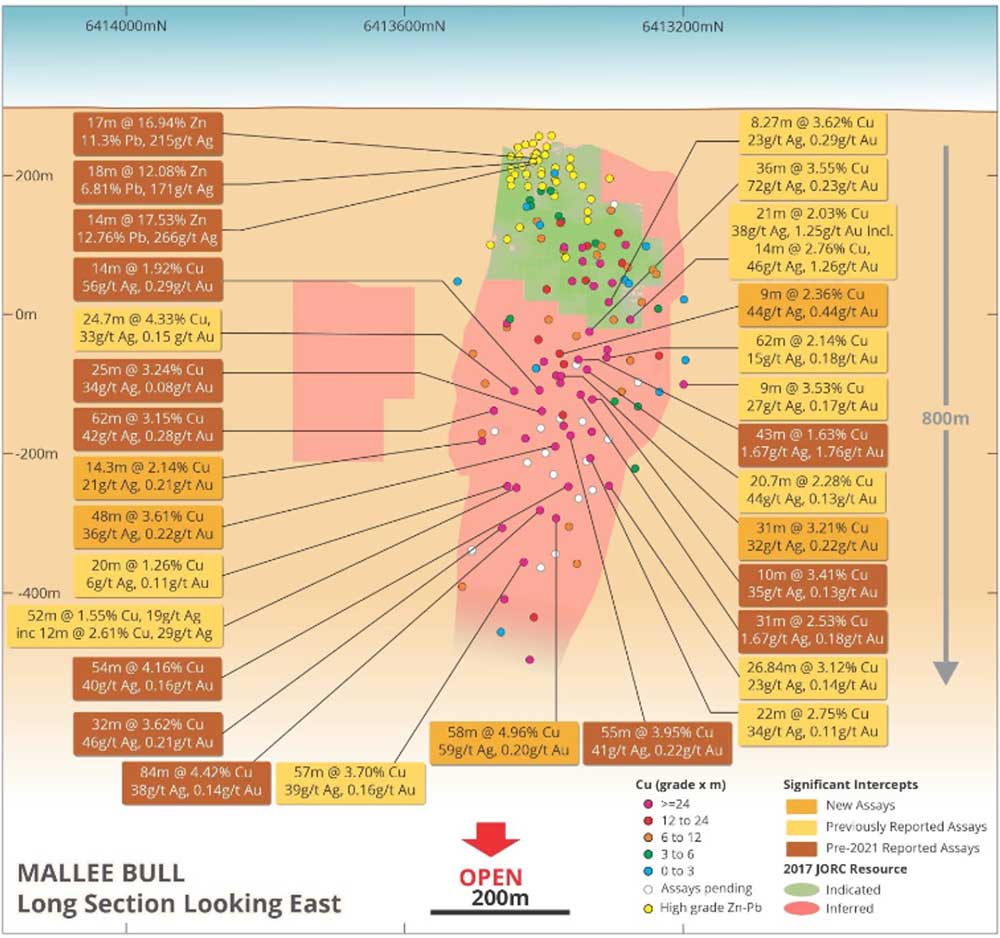

The last 10 years or so of exploration at Cobar have been highly successful and there appears to be significant resource upside at both Wirlong (figure 7) and Mallee Bull (figure 8).

Figure 7: PEX’s Wirlong Resource – oblique section (Source: PEX RIU Presentation, 15 February 2022).Figure 8: PEX’s Mallee Bull- long section looking east (Source: PEX RIU Presentation, 15 February 2022).

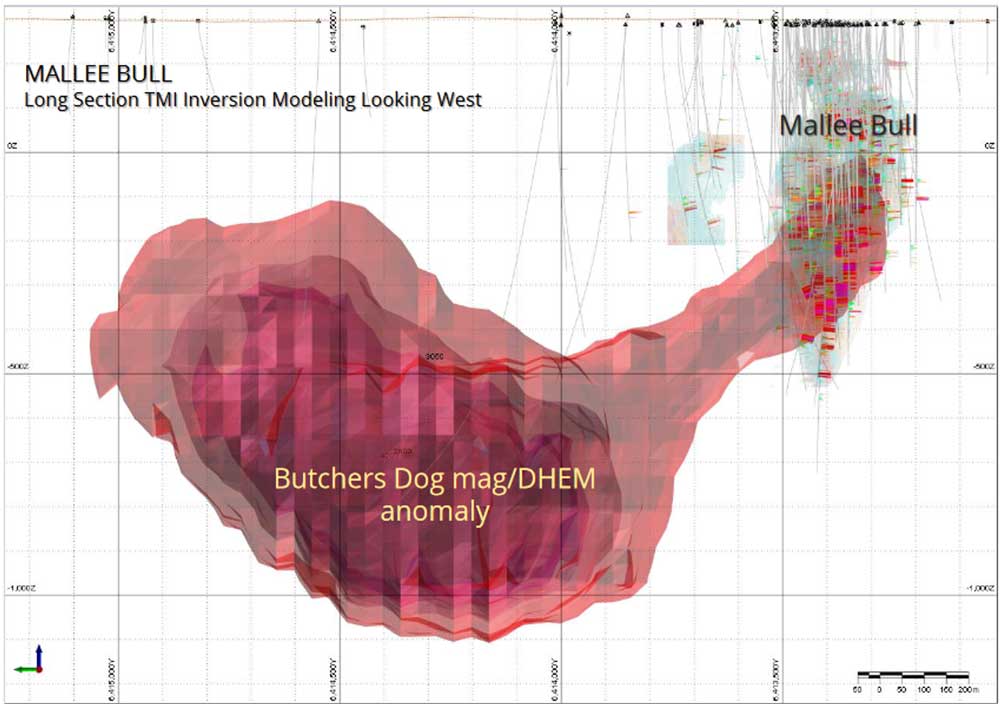

Mallee Bull north is also a large untested mag/DHEM anomaly that remains untested (figure 9) and its location just north of Mallee Bull should have any serious explorationist excited.

Figure 9: Butchers Dog mag/DHEM anomaly in long section looking west (Source: PEX RIU Presentation, 15 February 2022).

I believe the company would be looking to delineate +10Mt of JORC Resources into the Indicated category across the various deposits to achieve their objective of a 10yr mine life producing 20Ktpa of copper (equivalent).

Based on the provenance of the Cobar district (including the CSA Mine operated by Glencore at 50Ktpa of Cu) PEX is a good chance of delivering on its aspirational statements and at an EV of around $80 million, represents good value in a tight market for base metals.

At RM Corporate Finance, Guy Le Page is involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting, and corporate advisory roles.

He was head of research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July 1998. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada, and the United States. The views, information, or opinions expressed in the interview in this article are solely those of the interviewee and do not represent the views of Stockhead.

Stockhead has not provided, endorsed, or otherwise assumed responsibility for any financial product advice contained in this article.

Get the latest Stockhead news delivered free to your inbox

For investors, getting access to the right information is critical.

Stockhead’s daily newsletters make things simple: Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.

I want the news:

Hear it first

Get the latest Stockhead news delivered free to your inbox.

Thanks! You’re subscribed, Stockhead news is coming your way soon.