Guy on Rocks is a Stockhead series looking at the significant happenings of the resources market each week. Former geologist and experienced stockbroker Guy Le Page, director, and responsible executive at Perth-based financial services provider RM Corporate Finance, shares his high conviction views on the market and his “hot stocks to watch”.

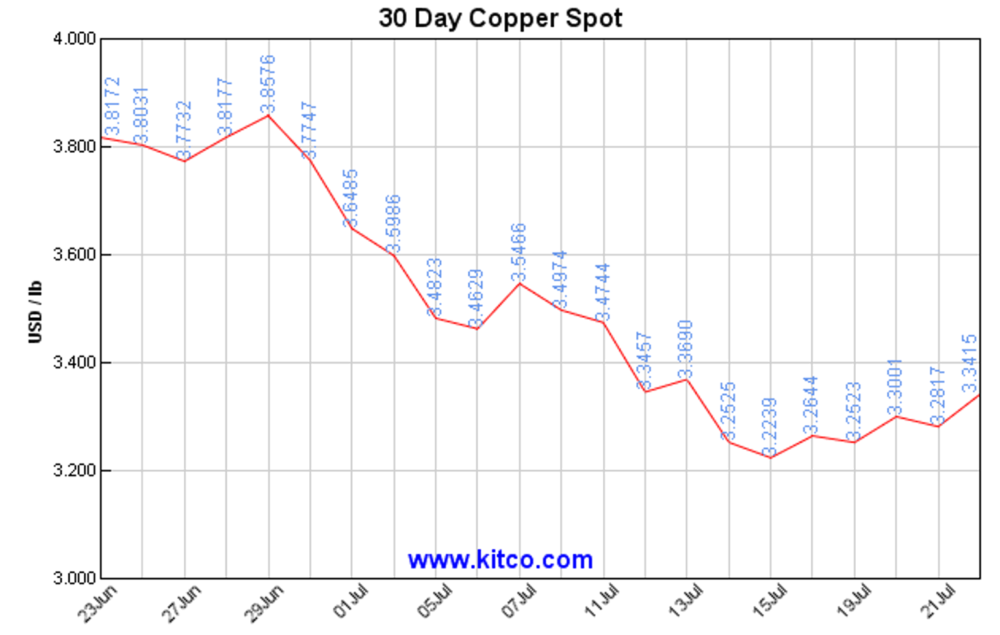

Market Ructions: Copper price nears cost of production

The volatility across all metals has continued with palladium up over 9% last week to close at US$1,924/ounce. Copper staged a big rally late last week closing at US$3.32/lb with three month-futures contracts now modestly in contango.

Not surprising, given copper prices are approaching costs of production for the average copper producer.

With gas supplies running low in Europe, Germany’s economy ministry has decided to reinvigorate its coal industry and also delay the planned closure of its remaining three nuclear power stations making up 6% of the country’s energy requirements.

According to the 2011 directive, they were supposed to be shut down by the end of 2022. Public support appears to be shifting as they face the possible reduction or cut-off of Russian gas.

A new assessment will be due out in a matter of weeks and will also take into consideration the impact of higher gas prices on electricity prices, gas supply outages and a cessation in French nuclear power.

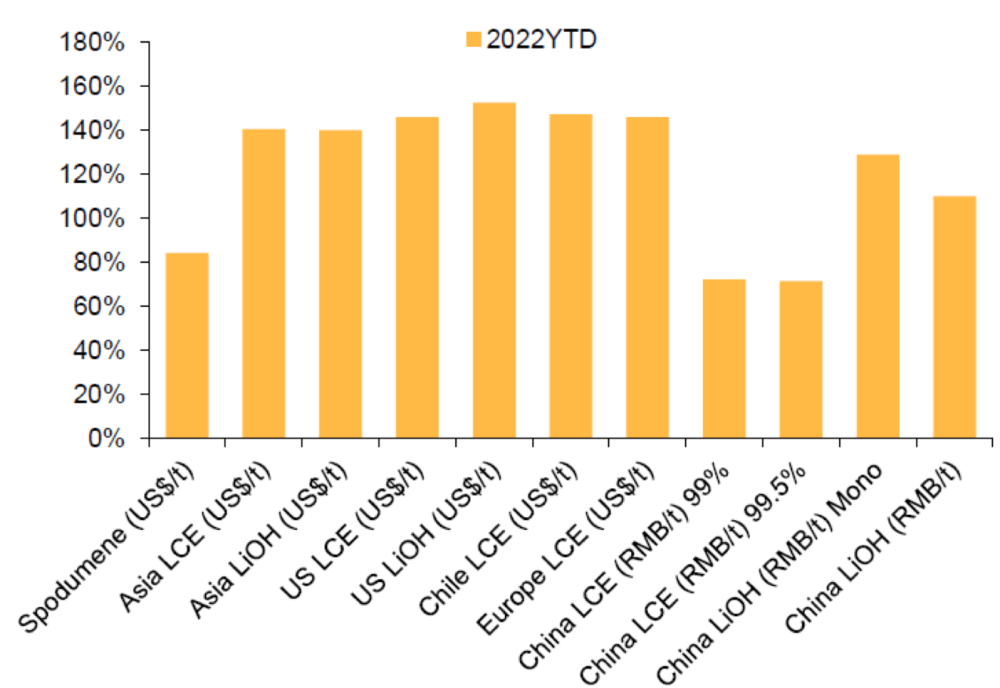

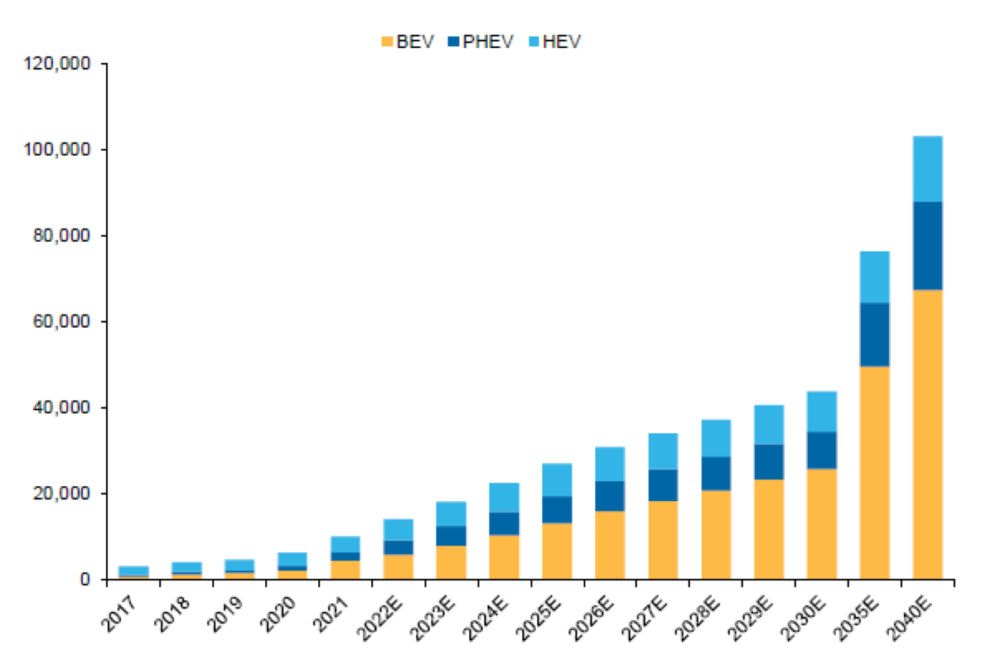

Lithium prices (figure 2) have been the strongest performer in the metals space this year and have been supported by strong EV demand (figure 3) in China up 40% month-on-month to 596,000 units in June according to Macquarie Research (July 2022).

In addition, the penetration rate increased by 0.5% to 26.8%, reflecting continued customer adoption growth. In the US BEV/PHEV sales have also continued to accelerate, up 5% MoM and 71% YoY to 83,000 units, with an increasing penetration rate.

A similar story in Europe with EV sales reaching 165k units in June 22 representing a 20.2% MoM increase.

Figure 2: Lithium price changes over CY 2022 (Source: Macquarie Research, July 2022).Figure 3: World EV sales projections (Source: Macquarie Research, July 2022).

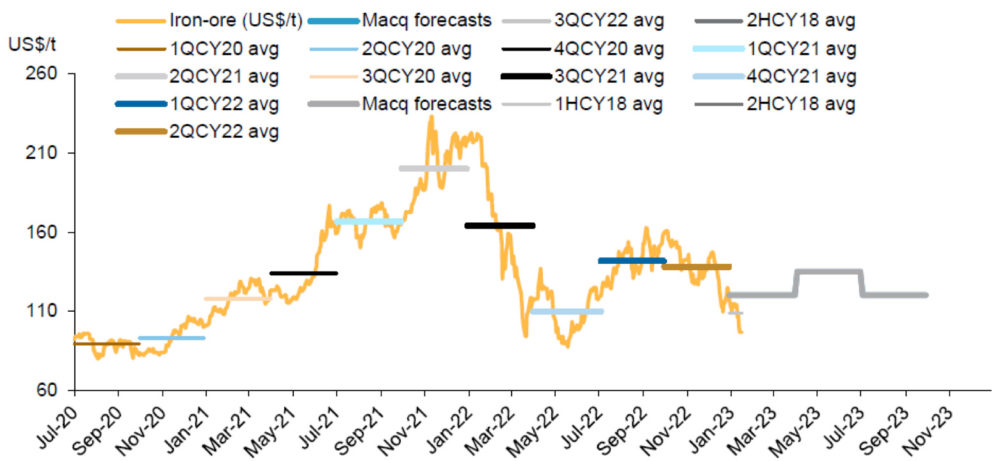

July has seen relatively soft property sales coming out of China which saw iron ore prices dip below US$100/t in mid-July (figure 4).

Mind you, the softer Australian dollar has cushioned the USD fall in prices.

Figure 4: Iron ore price projections (Source: Macquarie Research, 20 July 2022).

China appears to be moving forward with its plan to form a state-owned enterprise to manage both global supply and the giant Simandou deposit in Guinea.

The objective is to form an entity that has responsibility for raw materials supplies to the steel industry.

I am not sure how this is all going to pan out given the Chinese-led Winning Consortium Simandou (WCS) has put workers on leave with the possibility of layoffs as the dispute with Guinea’s government over infrastructure rolls on.

The Guinean government is demanding a 15% free carried undilutable interest in the railway and port JV.

Adavale Resources Corporation (ASX:ADD) is a Tanzanian nickel explorer led by executive director David Rieke which is currently bedding down a $3 million share placement at 2 cents per share.

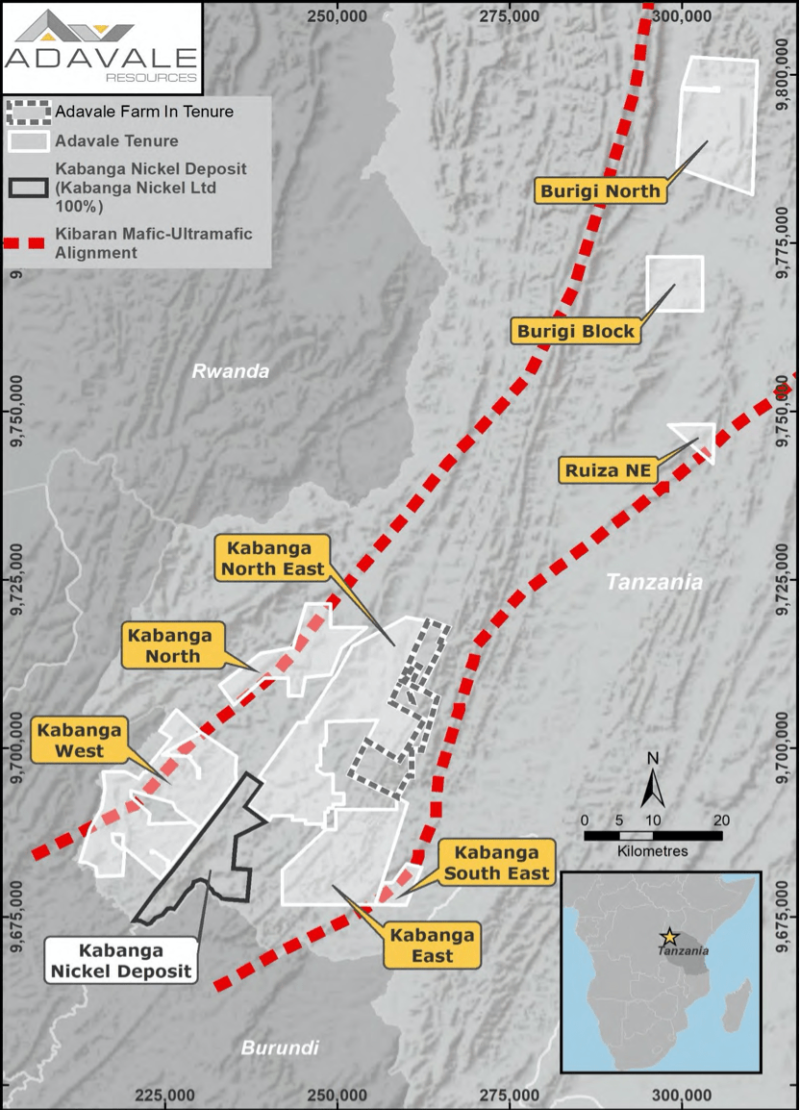

Proceeds will be applied towards their high priority nickel targets, including Kabanga Jirani and Luhuma. (figure 6).

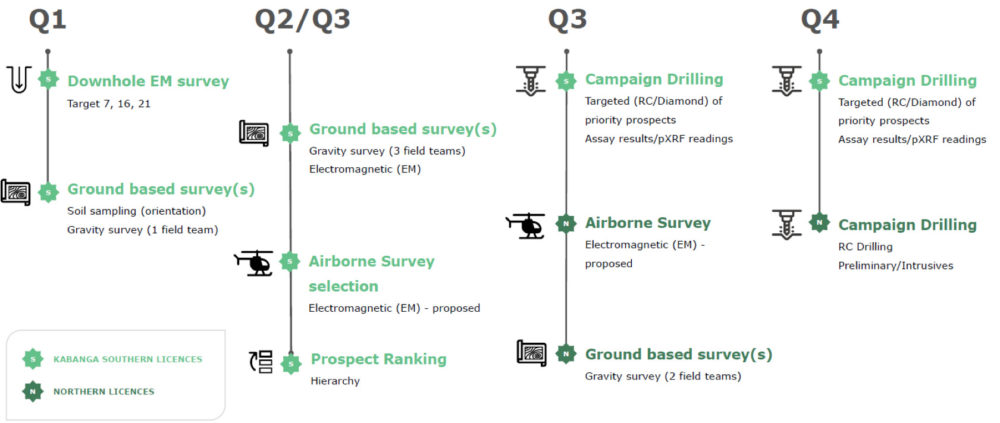

Exploration will include heliborne electromagnetic surveys with diamond and RC drilling to follow up any targets of interest from the geophysical survey.

The licences are 100% owned (with the exception of the Luhuma farm-in) and covers approximately 1,200km2 in the Kabanga-Musongati mafic-ultramafic belt which is prospective for Ni, Cu, Co, Cr and PGEs hosted in layered intrusions.

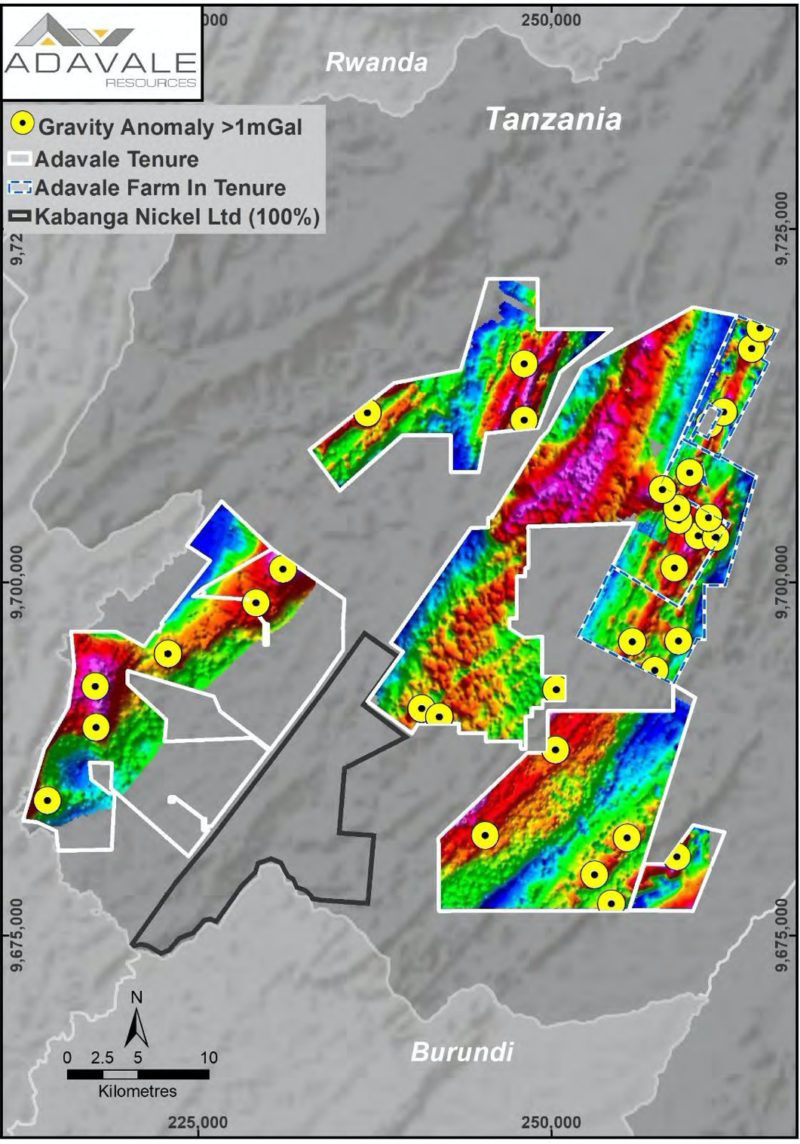

The 2021 exploration program included a prospect scale gravity survey (including 24,000 gravity stations) which has identified more than 32 new targets over a 55km strike length (figure 7).

At an enterprise value around $7 million, $4 million in cash (post placement) and with an active 2022/23 program (figure 8) I think ADD provides good leverage to any exploration success in a sector where there are few genuine junior nickel explorers.

It’s also refreshing to write up a Tanzanian explorer after the country was on the nose from 2017 till earlier this year when it tried to obtain a stake of 16% in miners and increase royalties by 50%.

Australian explorers and developers had a great run in the 1990s and the karma feels good here (which means I previously made good money).

Figure 6: Adavale’s Tanzanian exploration portfolio (Source: Company Presentation, July 2022).Figure 7: Priority targets from the 2021 gravity program (Source: Company Presentation, July 2022).Figure 8: Adavale’s 2022/23 exploration program (Source: Company Presentation, July 2022).

At RM Corporate Finance, Guy Le Page is involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting, and corporate advisory roles.

He was head of research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July 1998. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada, and the United States. The views, information, or opinions expressed in the interview in this article are solely those of the interviewee and do not represent the views of Stockhead.

Stockhead has not provided, endorsed, or otherwise assumed responsibility for any financial product advice contained in this article.

Get the latest Stockhead news delivered free to your inbox

For investors, getting access to the right information is critical.

Stockhead’s daily newsletters make things simple: Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.

I want the news:

Hear it first

Get the latest Stockhead news delivered free to your inbox.

Thanks! You’re subscribed, Stockhead news is coming your way soon.